VECTORIAL DAX (M5)

{kind=link}

Hello. I share with the community an automatic strategy that works on the DAX for M5 timeframe.

I wanted to test a strategy that involves observing the angular orientation of a moving average. The higher the angle and slope of the moving average, the stronger and more directional the movement. It then took me back into my distant memories of mathematics courses, trigonometry and vector calculus to try to develop this code.

The strategy consists first of all in calculating the angular orientation of a 10-period moving average (PeriodA) over a period of 15 bars (nbChandelierA). Then I calculate the slope of this moving average. This amounts to calculating a “vector” hence the name of the algorithm.

I then added a trailing stop and optimized the entry points with particular playing on the variable “lag”.

I launched the code in real mode and in demo mode. There are some differences in the positions, but overall it works pretty well.

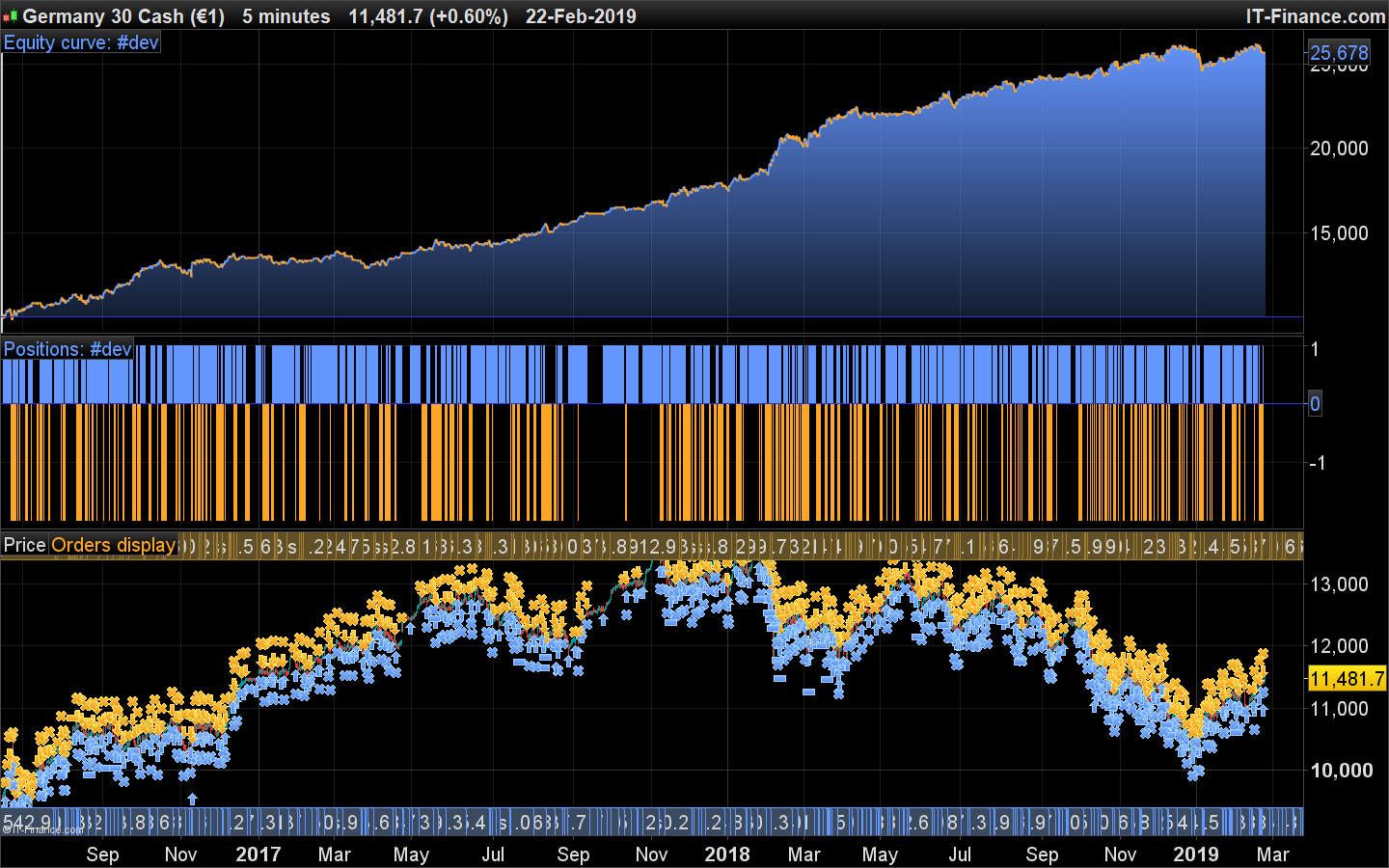

Note that the attached backtest images correspond to a backtest on 200,000 bars (Premium version of PRT) with a spread of 1.5 points.

The code looks good on other timeframes (including H4) by changing the variables.

Looking forward to having your feedback, feedback and suggestions for improvements.

// ROBOT VECTORIAL DAX

// M5

// SPREAD 1.5

// by BALMORA 74 - FEBRUARY 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//VARIABLES

CtimeA = time >= 080000 and time <= 220000

CtimeB = time >= 080000 and time <= 220000

ONCE BarLong = 950 //EXIT ZOMBIE TRADE LONG

ONCE BarShort = 650 //EXIT ZOMBIE TRADE SHORT

// TAILLE DES POSITIONS

ONCE PositionSizeLong = 1

ONCE PositionSizeShort = 2

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CondBuy1 = ANGLE >= 45

CondSell1 = ANGLE <= - 37

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

lag = 5

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CondBuy2 = (pente > trigger) AND (pente < 0)

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

//ENTREES EN POSITION

CONDBUY = CondBuy1 and CondBuy2 and CTimeA

CONDSELL = CondSell1 and CondSell2 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSizeLong contract at market

SET TARGET %PROFIT 4.25

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSizeShort contract at market

SET TARGET %PROFIT 1.25

ENDIF

//VARIABLES STOP SUIVEUR

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 7.5 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 25 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

//EXIT ZOMBIE TRADE

IF POSITIONPERF<0 THEN

IF shortOnMarket AND BARINDEX-TRADEINDEX(1)>= barshort THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

IF POSITIONPERF<0 THEN

IF LongOnMarket AND BARINDEX-TRADEINDEX(1)>= barlong THEN

SELL AT MARKET

ENDIF

ENDIF{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}