Universal XBody Strategy on DAX(1Day)

June 12, 2024, 9:23 AM

Strategies

1 Comment

{kind=link}

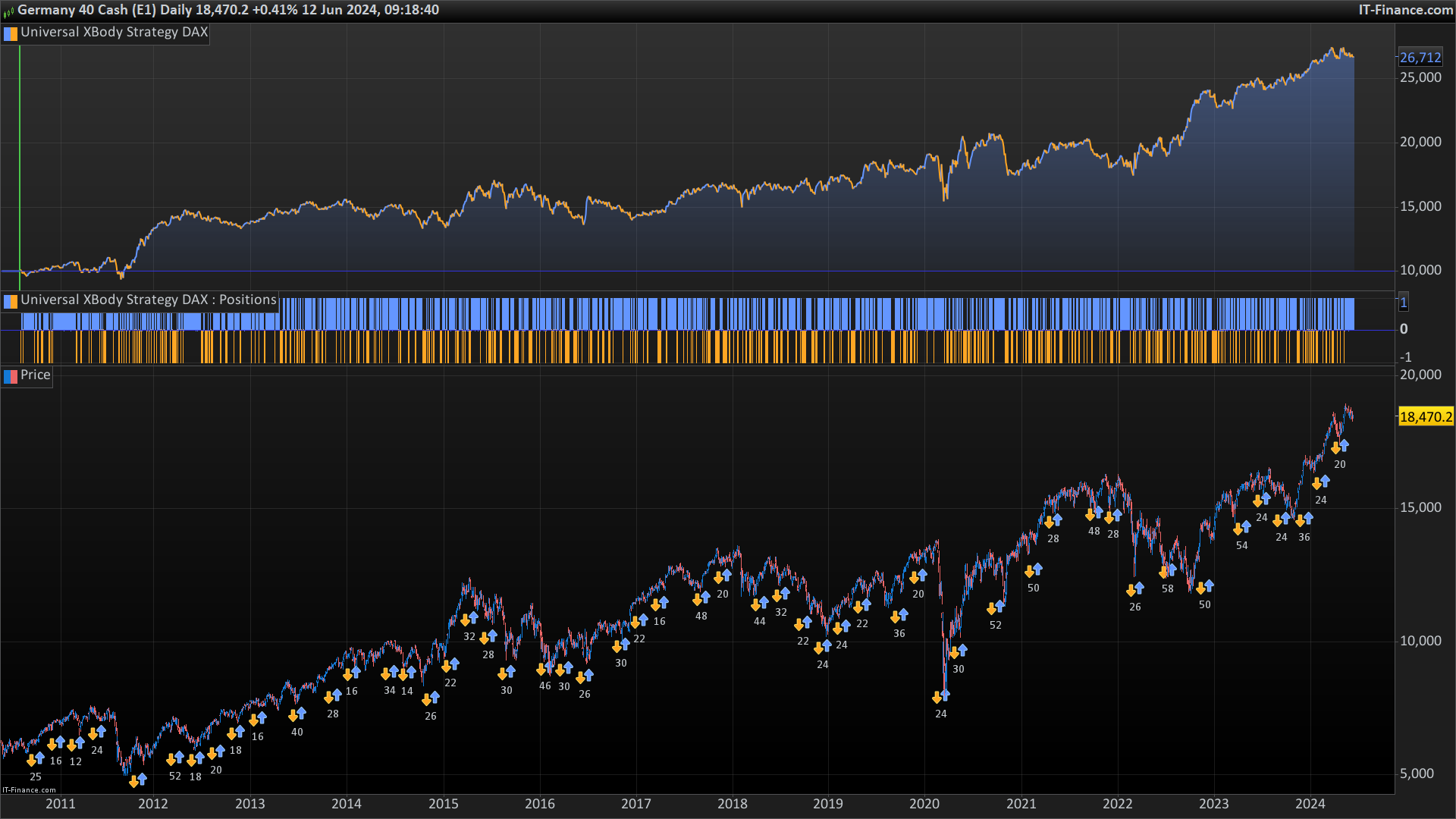

I have the pleasure of sharing with you the Dax version of the Universal XBody Strategy (which you can find here), with the parameters optimized for this market.

Happy Trading!

//-------------------------------------------------------------------------

defparam cumulateorders=false

//------------------ SYSTEM VARIABLES---------------------------------------

//DAX40 Values: -------------------------------------------- Ottimization info

period=84// Optimize best value for each Symbol, range=1-1000, with step=1

mode=1// Optimize the best trading mode , range=1-4, with step=1

invertsignal=1// 1=positive signal, -1=negative signal, range=-1/1, with step=2

//***********************************************************************************************

//------------------ SYSTEM FILTER---------------------------------------

filter1=81// to set after the variable optimization, range=1-100, with step=1

filter2=6// to set after the variable optimization, range=1-100, with step=1

//------------------ INDICATOR ---------------------------------------

n = 1 //contracts quantity

body=close-open

var=(body-body[1])

sumvar=summation[period](var)

if sumvar>filter1*pipsize then

green=(sumvar)

endif

if sumvar<-filter2*pipsize then

red=(sumvar)

endif

if mode=1 then

c1=red<red[1]

c2=green>green[1]

endif

if mode=2 then

c1=red>red[1]

c2=green<green[1]

endif

if mode=3 then

c1=red<red[1]

c2=green<green[1]

endif

if mode=4 then

c1=red>red[1]

c2=green>green[1]

endif

if c1 then

signal=1*invertsignal

elsif c2 then

signal=-1*invertsignal

endif

// Conditions for entering long positions and exit short positions

IF signal>0 then

BUY n contract AT market

ENDIF

// Conditions for entering short positions and exit long positions

IF signal<0 THEN

SELLSHORT n CONTRACTs AT market

ENDIF

Download

Filename:

Universal-XBody-Strategy-DAX.itf

Downloads:

121

Average

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...