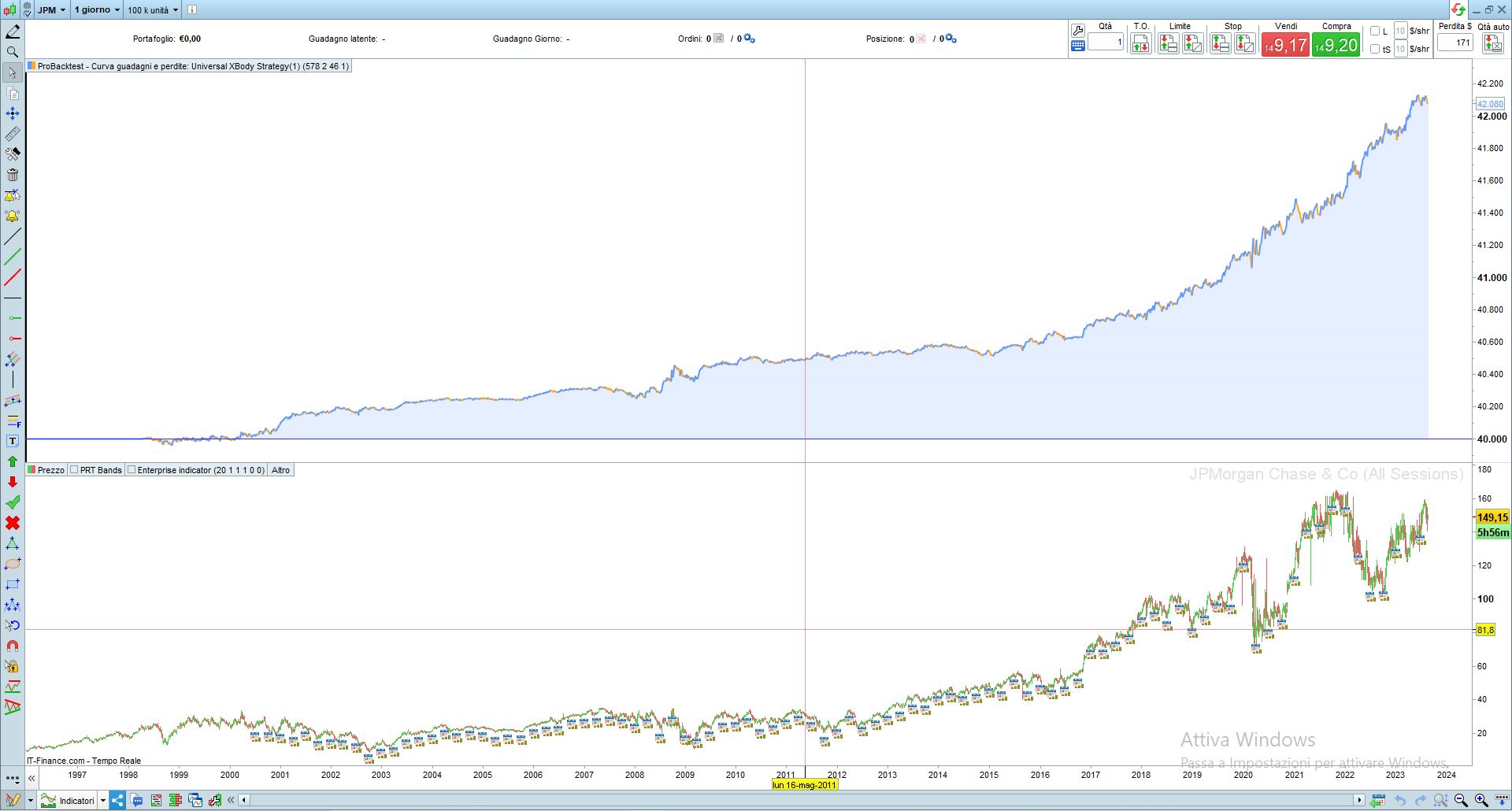

Universal XBody Strategy on Jp Morgan Chase (1Day)

August 22, 2023, 4:55 PM

Strategies

8 Comments

{kind=link}

here is the same strategy (other one can be found here) with the parameters adapted to follow the movements of the shares of the famous JP Morgan Chase bank.

//-------------------------------------------------------------------------

// Codice principale : Universal XBody Strategy

//-------------------------------------------------------------------------

//Universal XBody STrategy

// instrument: Jp Morgan Chase

// timeframe : Daily

// Spread: 0.3

// created and coded by davidelaferla

//————————————————————————-

//-------------------------------------------------------------------------

defparam cumulateorders=false

//***********************************************************************************************************

//------------------ SYSTEM VARIABLES---------------------------------------

//CAC40 Values: -------------------------------------------- Ottimization info

period=578// Optimize best value for each Symbol, range=1-1000, with step=1

mode=2// Optimize the best trading mode , range=1-4, with step=1

invertsignal=1// 1=positive signal, -1=negative signal, range=-1-1, with step=2

//***********************************************************************************************

//------------------ SYSTEM FILTER---------------------------------------

filter1=46// to set after the variable optimization, range=1-100, with step=1

filter2=1// to set after the variable optimization, range=1-100, with step=1

//------------------ INDICATOR ---------------------------------------

n=5

giorno=opendayofweek

body=close-open

var=(body-body[1])

sumvar=summation[period](var)

if sumvar>filter1*pipsize then

green=(sumvar)

endif

if sumvar<-filter2*pipsize then

red=(sumvar)

endif

if mode=1 then

c1=red<red[1]

c2=green>green[1]

endif

if mode=2 then

c1=red>red[1]

c2=green<green[1]

endif

if mode=3 then

c1=red<red[1]

c2=green<green[1]

endif

if mode=4 then

c1=red>red[1]

c2=green>green[1]

endif

if c1 then

signal=1*invertsignal

elsif c2 then

signal=-1*invertsignal

endif

// Conditions for entering long positions and exit short positions

IF signal>0 and opendayofweek<5 then

BUY n contract AT market

ENDIF

// Conditions for entering short positions and exit long positions

IF signal<0 and opendayofweek<5 THEN

SELLSHORT n CONTRACTs AT market

ENDIF

Download

Filename:

Universal-XBody-Strat-JpMorgan.itf

Downloads:

150

Average

Operating in the shadows, I hack problems one by one. My bio is currently encrypted by a complex algorithm. Decryption underway...

Author’s Profile

Loading...