The "Turtle Soup"

April 3, 2016, 4:56 PM

Strategies

6 Comments

{kind=link}

I recently discovered this strategy Linda Bradford Raschke.

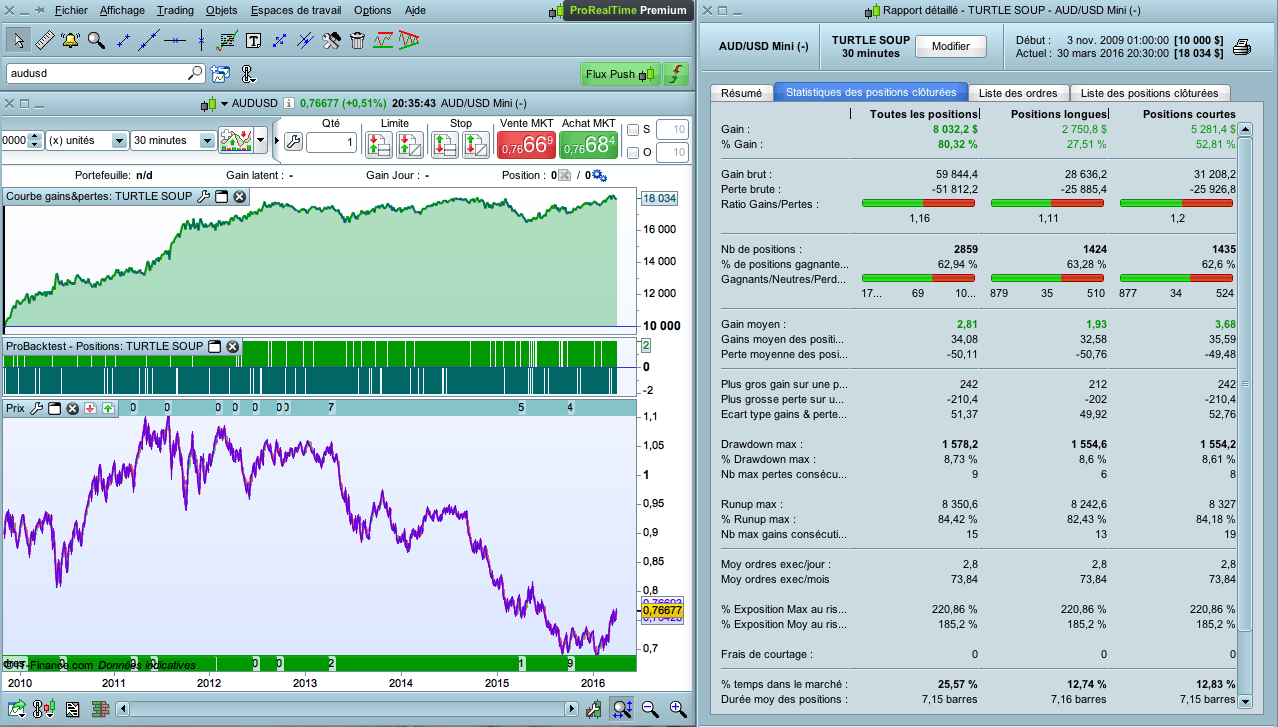

Everyone knows the mythical “Turtle strategy”. The problem is that it is not performing with forex.

This new strategy applies in forex, with modified parameters, which are a bit like the strategy of turtles.

It applies in M30 timeframe.

I’m a little disappointed with the results overall (bad profit factor), even is the strategy is profitable on the long term, with most forex pairs. I have checked my code, there is no error.

Too bad we can not go before the backtest 2010 with PRT (the website where I saw the backtest showed tests since 2006, with good growth in capital curves).

In any case it remains promising, there are probably ways to improve the code.

DEFPARAM CumulateOrders = False

n = 2

// Conditions pour ouvrir une position acheteuse

c1 = close < lowest[5](low)[1]

c2 = ExponentialAverage[21](close) > ExponentialAverage[30](close)

ctime = time > 060000 and time < 220000

IF c1 AND c2 and ctime THEN

BUY n CONTRACT AT MARKET nextbaropen

ENDIF

// Conditions pour fermer une position acheteuse

c3 = high > highest[5](high)[1]

IF c3 THEN

SELL AT MARKET

ENDIF

// Conditions pour ouvrir une position vendeuse

c1 = close > highest[5](high)[1]

c2 = ExponentialAverage[21](close) < ExponentialAverage[30](close)

ctime = time > 060000 and time < 220000

IF c1 AND c2 and ctime THEN

SELLSHORT n CONTRACT AT MARKET nextbaropen

ENDIF

// Conditions pour fermer une position vendeuse

c3 = low < lowest[5](low)[1]

IF c3 THEN

EXITSHORT AT MARKET

ENDIF

// Stops et objectifs

SET STOP LOSS 3*AverageTrueRange[20](close)

Download

Filename:

The-Turtle-Soup.itf

Downloads:

382

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...