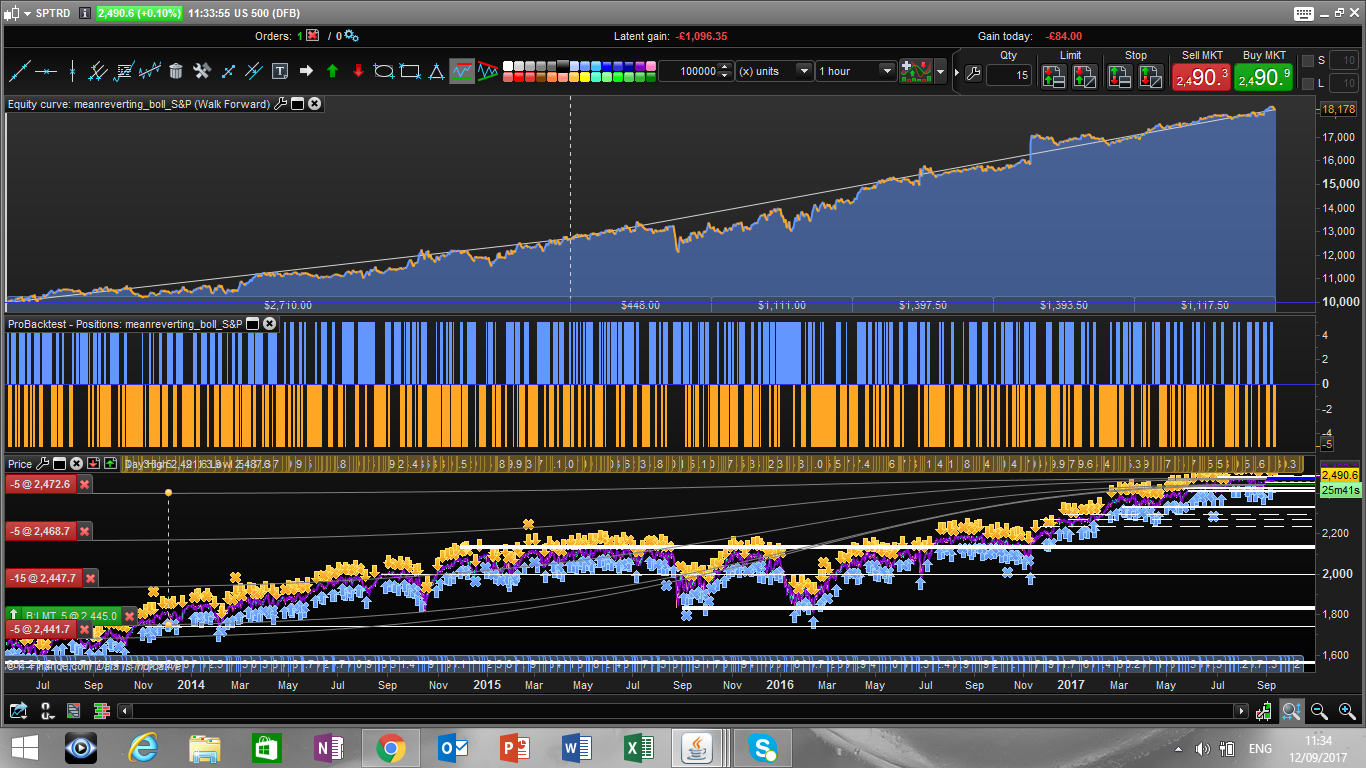

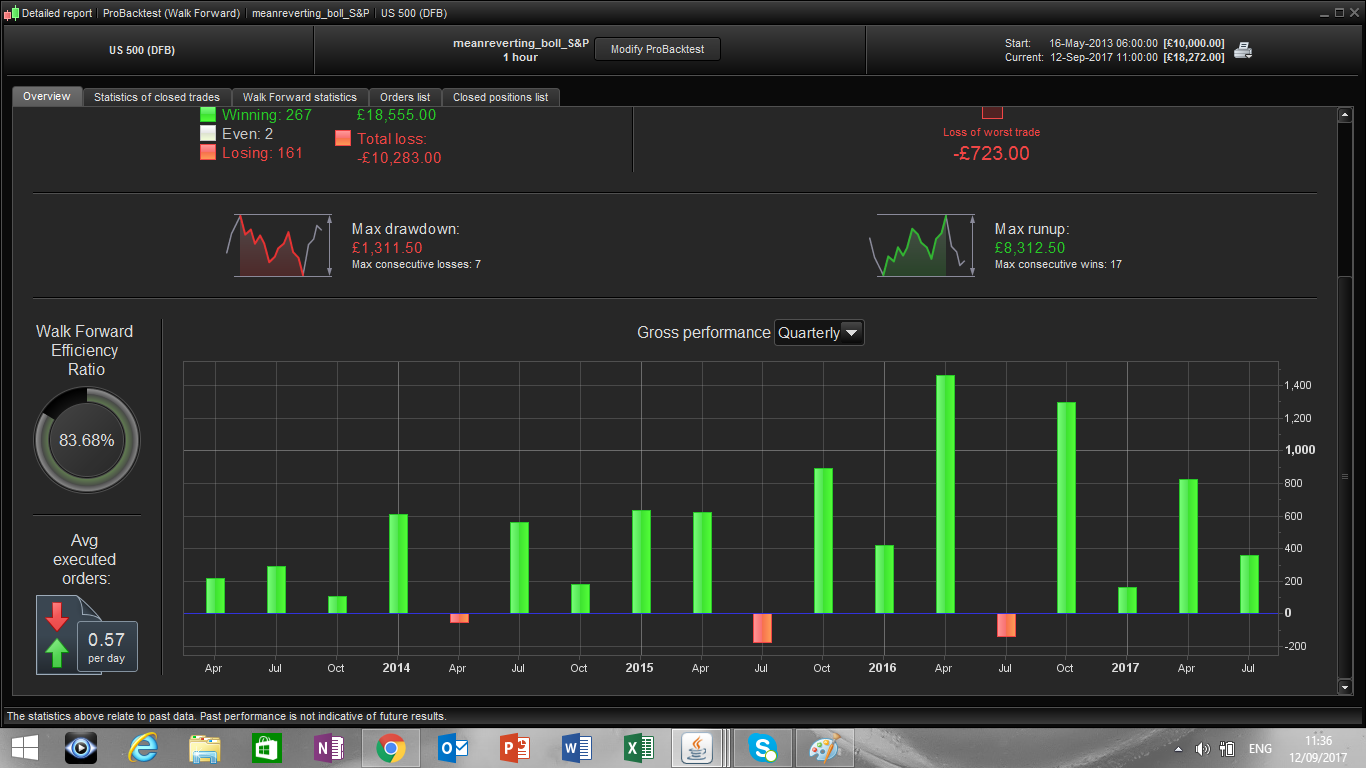

S&P 500 mean reverting strategy

September 13, 2017, 10:53 AM

Strategies

18 Comments

{kind=link}

Dear all,

pls enjoy this little code which gives very nice results on S&P 500.

There are only 2 variables optimized (the bollinger bands and the moving average periods) , can work with several underlying.

Best regards

Francesco

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//optimized parameters

bbperiod = 30

averageperiod = 180

bollup = BollingerUp[bbperiod](close)

bolldown = BollingerDown[bbperiod](close)

cl = (close >= bollup)

cl = cl AND (open >= bollup)

cs = (close <= bolldown)

cs = cs AND (open <= bolldown)

IF cs THEN

buy 5 PERPOINT AT MARKET

ENDIF

if cl then

sellshort 5 perpoint at market

endif

// Conditions to exit short positions

aver = Average[averageperiod](close)

c1 = (close CROSSES under aver)

c2 = (close CROSSES over aver)

IF c1 and longonmarket THEN

sell AT MARKET

ENDIF

if c2 and shortonmarket then

exitshort at market

endif

Download

{kind=link}

Filename:

wf_Stat.png

Downloads:

309

Download

{kind=link}

Filename:

SP_stat-1.png

Downloads:

328

Download

{kind=link}

Filename:

SP_stat.png

Downloads:

546

Download

Filename:

meanreverting_boll_SP.itf

Downloads:

807

Master

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...