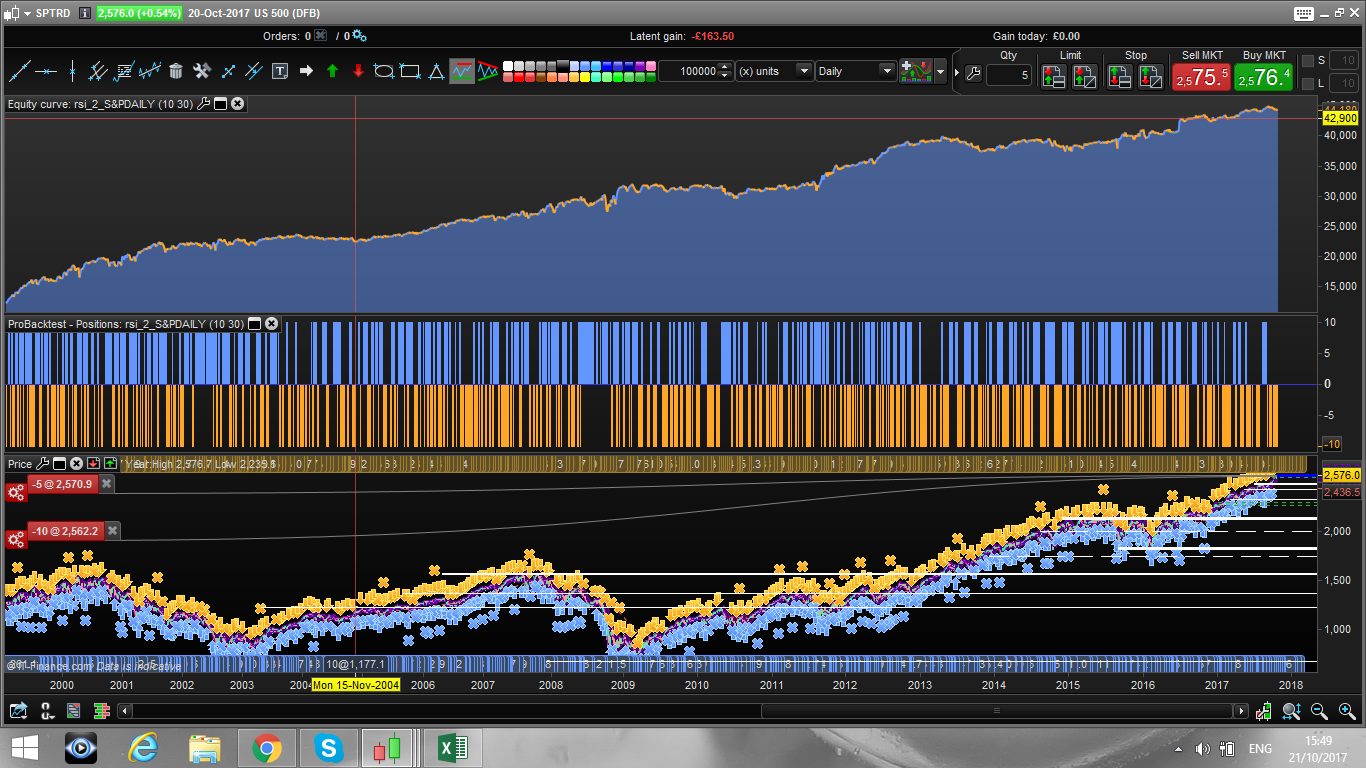

S&P 500 daily RSI(2) long short strategy

October 21, 2017, 4:36 PM

Strategies

17 Comments

{kind=link}

Hi all,

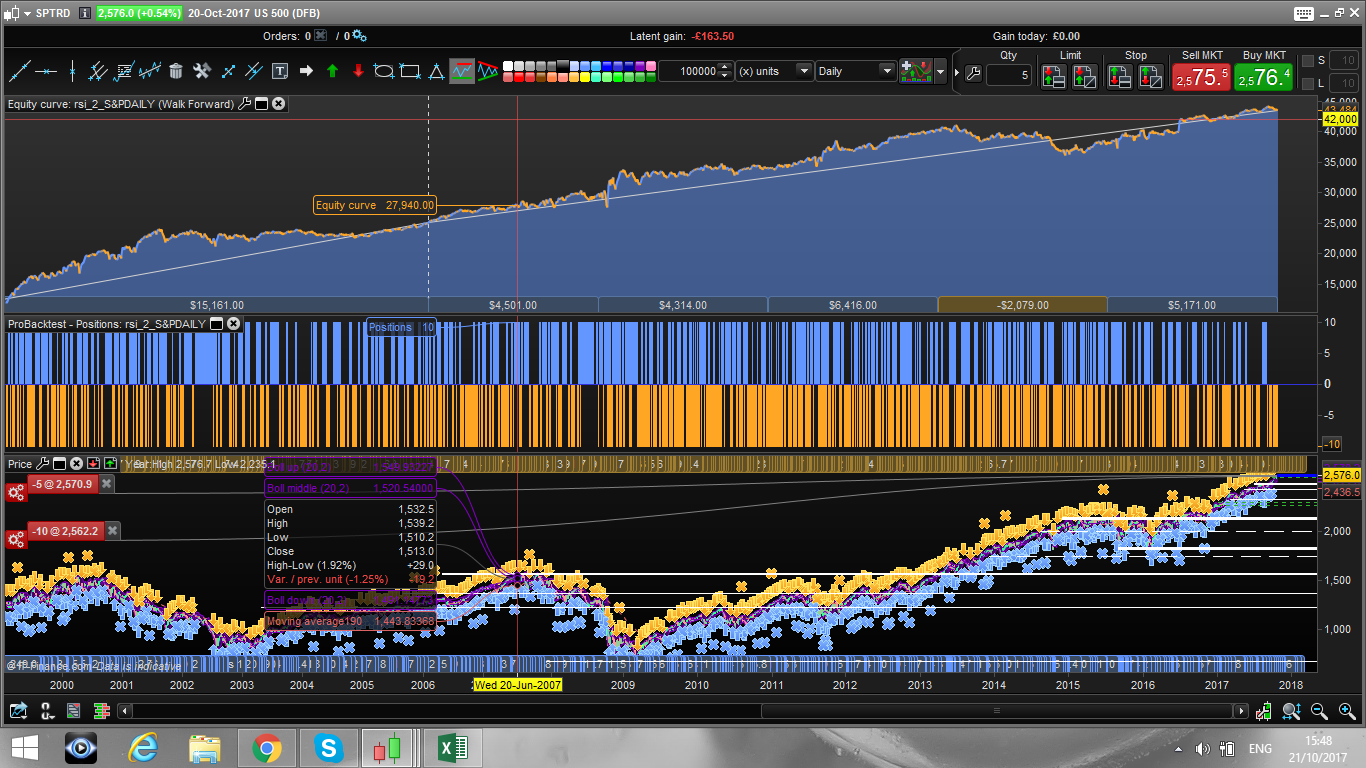

Have a look to this daily strategy on S&P 500. I guess many of you already know it, as it is made very famous by Larry Connors, I just added a bit of asymmetry between long and short, but the code is still extremely light, with only 2 parameters optimized and a stable performance of over 20 year!

defparam cumulateorders = false

cl = RSI[2]<a

cs = RSI[2]>100-a

if cl then

buy 10 contracts at market

endif

if cs then

sellshort 10 contract at market

endif

if longonmarket and RSI[2]>100-(a+b) and close < open then

sell at market

endif

if shortonmarket and RSI[2]<(a+b) then

exitshort at market

endif

Download

Filename:

rsi_2_SPDAILY.itf

Downloads:

821

Download

{kind=link}

Filename:

prc_wf_sp_daily.png

Downloads:

255

Download

{kind=link}

Filename:

prc_sp_daily.png

Downloads:

315

Master

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...