RSI 3 periods QQQ Powerness

February 8, 2016, 7:12 PM

Strategies

4 Comments

{kind=link}

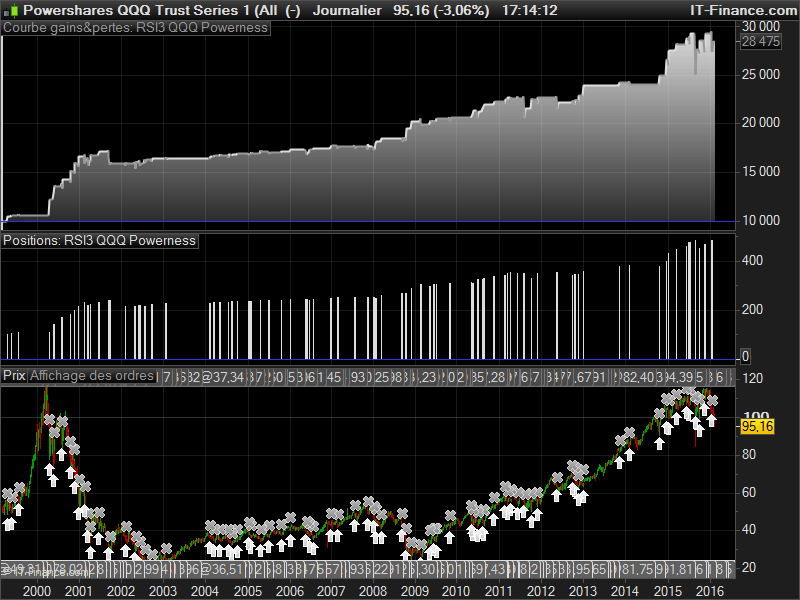

Another long only strategy built with mean reversion in mind with a classic Relative Strength Index indicator on 3 periods. Buying the deep RSI 3 periods (under 10 level) and sold the long position when RSI rise above the 50 level.

I also add a dynamic lot calculation made upon the strategyprofit. You can change the value of the “initial lot” (100 shares at start) and the “step profit” which add more shares whenever the strategy gain a new stepprofit (50$ by default).

14.5% drawdown while almost being 8% of traded time in the market. Annualized return of 11.5% profit, 16 years long.

//indicator

myRSI = RSI[3](close)

//initial lot

initLOT = 100

//profit step of the strategy to increase lot

stepPROFIT = 50

myLOT = max(initLOT,initLOT+ROUND((strategyprofit-stepPROFIT)/stepPROFIT))

IF NOT LongOnMarket AND myRSI<10 THEN

BUY myLOT CONTRACTS AT MARKET

ENDIF

If LongOnMarket AND myRSI>50 THEN

SELL AT MARKET

ENDIF

No files found.

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...