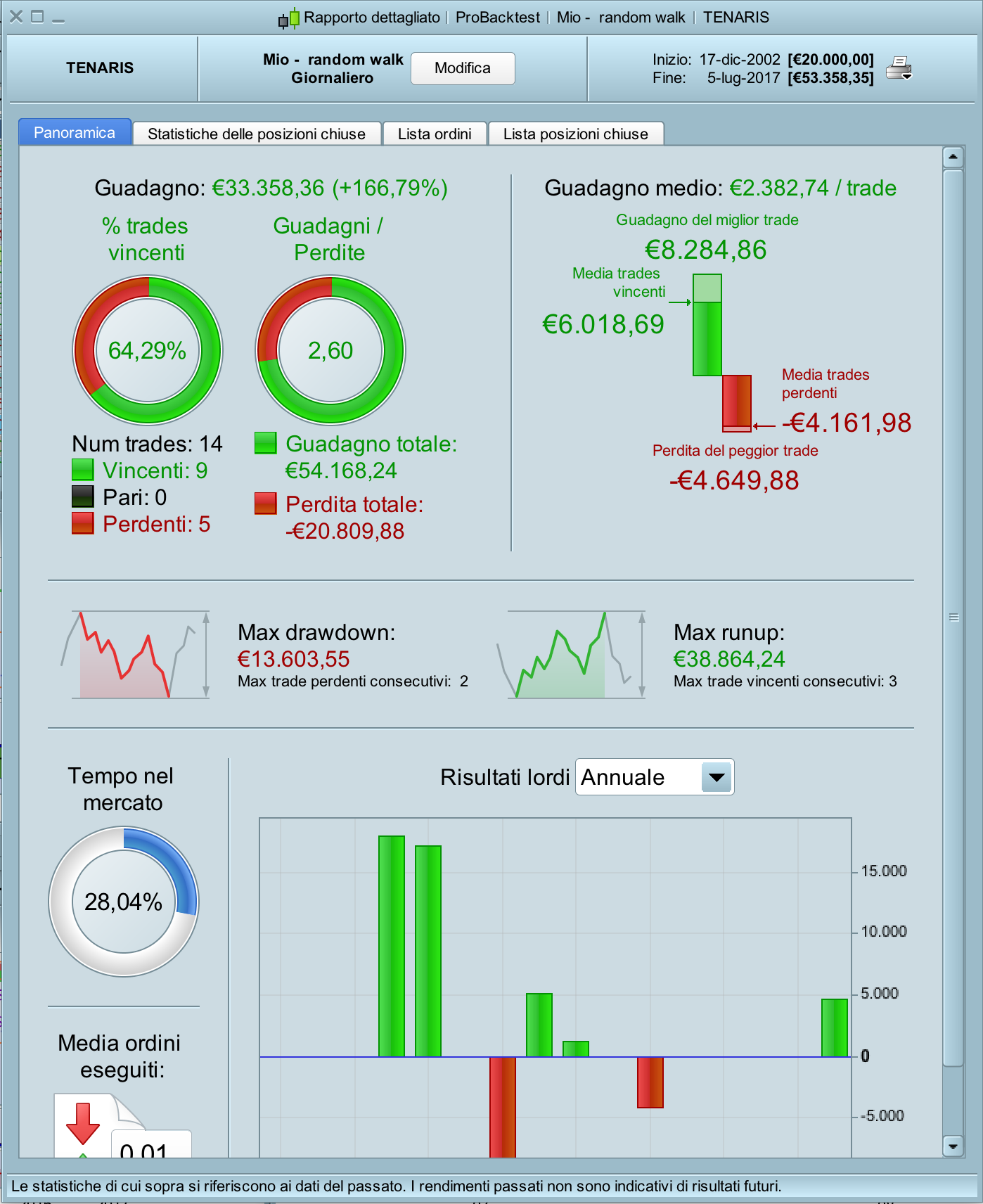

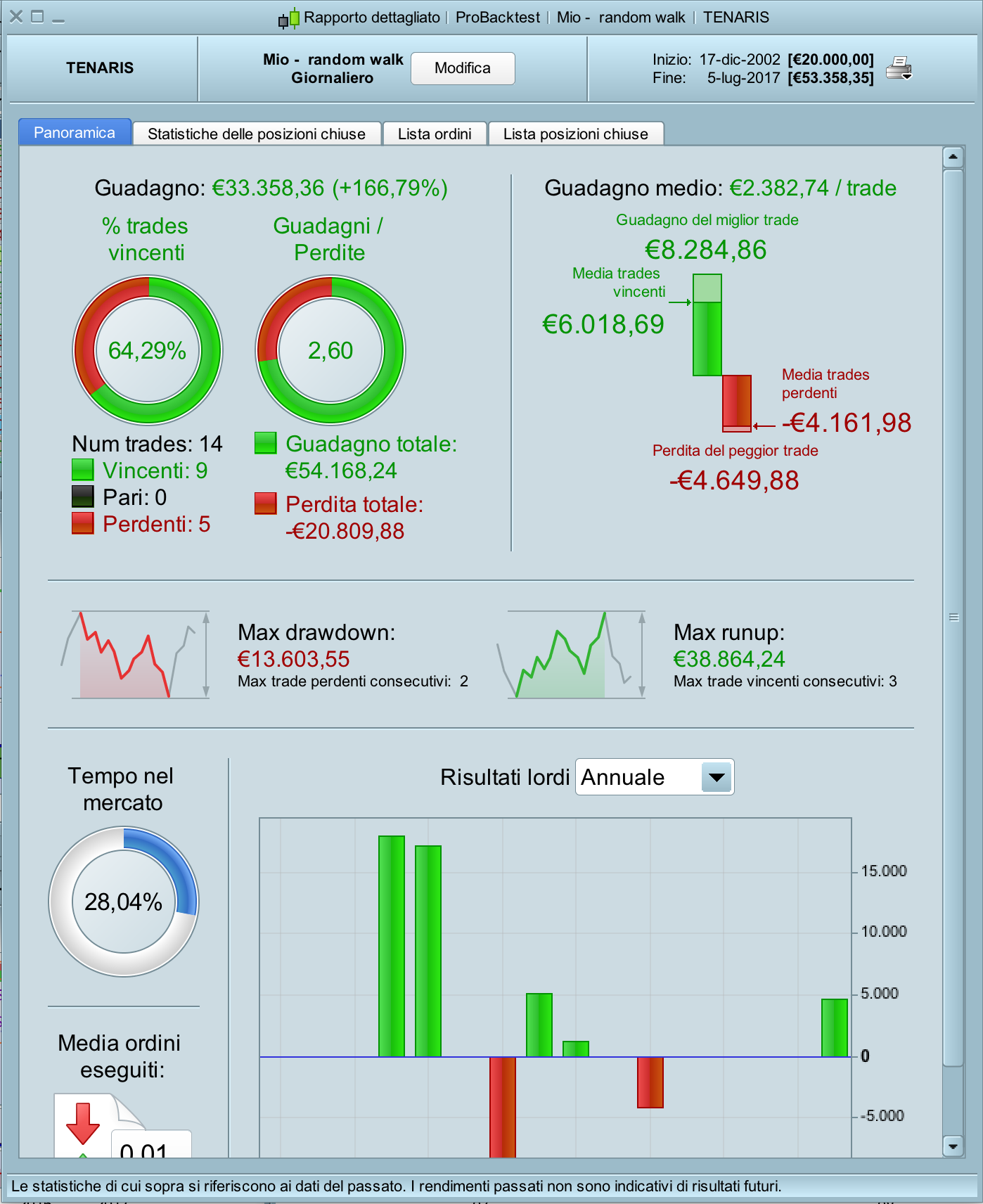

Random Walk Strategy

{kind=link}

This is a variation of the “Price Index 6 months strategy” and it’s LONG only. The selected stock has to be a good performer in terms of Price Index value. While in the former strategy the exit was made ALWAYS after a hold period of one year, in this strategy we sell in one of the following cases:

1. Gain = 40% (or whatever value chosen)

2. Loss = 20% (or half the target gain)

3. after 6 months holding time without exiting as per points 1 or 2 (you can also use 3 months max hold time)

I’ve been using this strategy real-money with portfolios of stocks from different countries for about 5 years and a half now with a annualized return of the portfolio of about 26% (I uses a portfolio with 30 to 50 stocks).

If you select the top stocks in terms of the relative strength in their sector the annualised return is approximately 35%.

Blue skies!

// Definizione dei parametri del codice

DEFPARAM CumulateOrders = False // Posizioni cumulate disattivate

p=130

out=40

// Condizioni per entrare su posizioni longs

c1 = (100*(close - close[p])/close[p])>44

IF c1 and not longonmarket THEN

BUY 20000 cash AT MARKET

ENDIF

barontrade=barindex-tradeindex

// exit long position

IF barontrade=130 THEN

SELL AT MARKET

ENDIF

set target %profit out

set stop %loss out/2{kind=link}