Pathfinder DAX 4H

July 4, 2016, 8:19 AM

Strategies

192 Comments

{kind=link}

Hi guys,

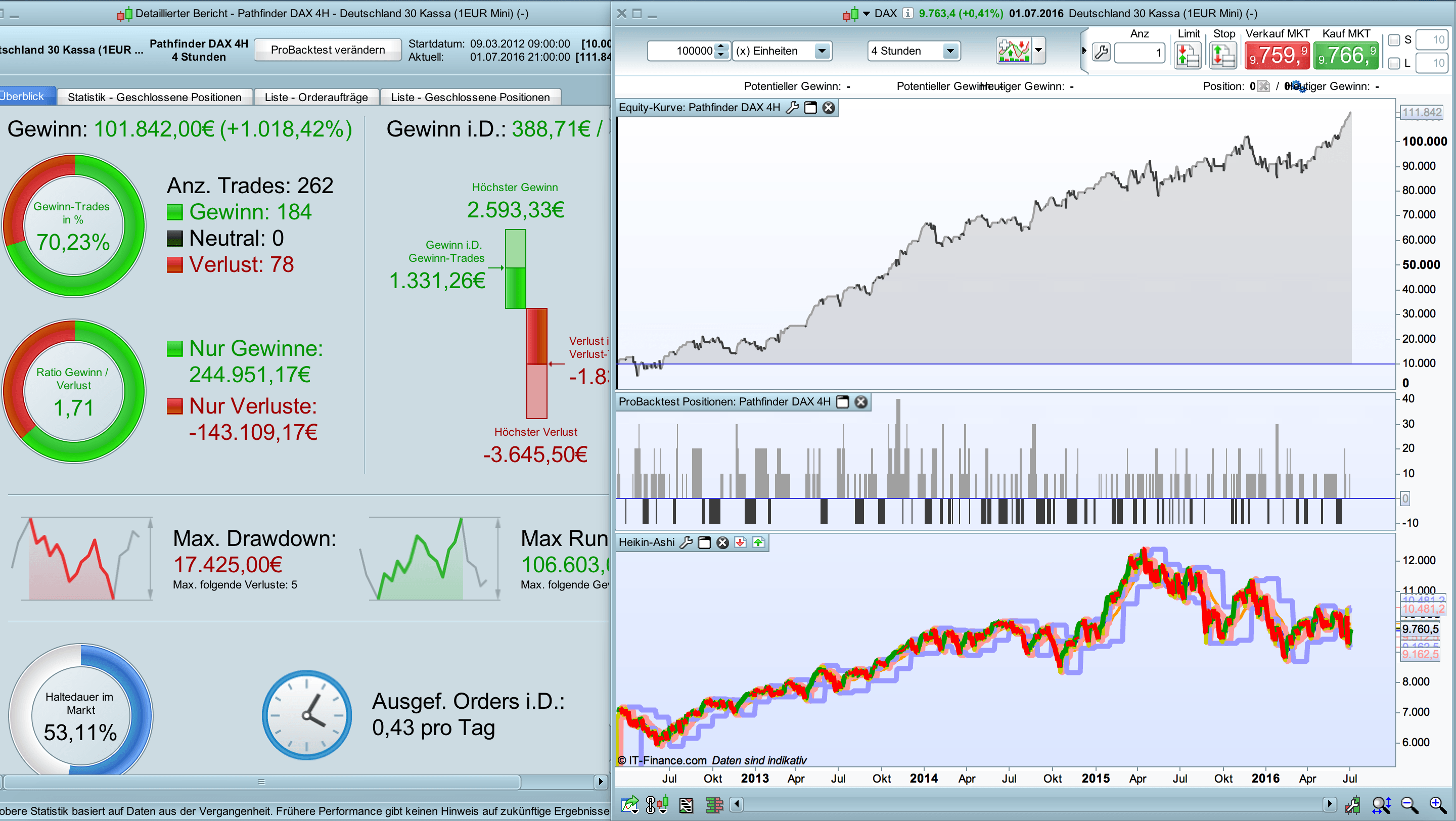

I want to share one of my DAX trading ideas based on simple daily, weekly and monthly high/low crossings. I observed that simple cross over and cross under of daily/weekly/monthly high/lows in combination with a multiple smoothed average and some simple filters could be a profitable approach. On the long side the cumulation of orders could be a performance booster for this system.

Comments and suggestions for improvement are welcome.

Have fun

Reiner

// Pathfinder DAX 4H, 9-22, 2 points spread

// DAX breakout system triggered by previous daily, weekly and monthly high/low crossings

// Version 3

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// trading window 8-22

ONCE startTime = 80000

ONCE endTime = 220000

// smoothed average parameter (signalline)

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// filter parameter

ONCE periodLongMA = 250

ONCE periodShortMA = 50

// trading paramter

ONCE PositionSize = 1

// money and position management parameter

ONCE stoppLoss = 5 // in %

ONCE takeProfitLong = 2 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE maxCandlesLongWithProfit = 18 // take long profit latest after 18 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

ONCE startShortPattern = 4 // April

ONCE endShortPattern = 9 // September

ONCE longPositionMultiplier = 2 // multiplier for long position size in case of higher saisonal probability

ONCE shortPositionMultiplier = 2 // multiplier for short position size in case of higher saisonal probability

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// trade only in trading window 8-22

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

c1 = close > Average[periodLongMA](close)

c2 = close < Average[periodLongMA](close)

c3 = close > Average[periodShortMA](close)

c4 = close < Average[periodShortMA](close)

// saisonal pattern

saisonalShortPattern = CurrentMonth >= startShortPattern AND CurrentMonth <= endShortPattern

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER monthlyLow

s3 = signalline CROSSES UNDER dailyLow

// long entry

IF ( l1 OR l4 OR l2 OR (l3 AND c2) ) THEN // cumulate orders for long trades

IF not saisonalShortPattern THEN

BUY PositionSize * longPositionMultiplier CONTRACT AT MARKET

ELSE

BUY PositionSize CONTRACT AT MARKET

ENDIF

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND c3) OR (s2 AND c4) OR (s3 AND c1) ) THEN // no cumulation for short trades

IF saisonalShortPattern THEN

SELLSHORT positionSize * shortPositionMultiplier CONTRACT AT MARKET

ELSE

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stoppLoss

SET TARGET %PROFIT takeProfit

ENDIF

Many other instruments and continuously updated versions are available in the dedicated forum topic of this automated trading strategy, everyone can read and participate here: Pathfinder trading strategy forum topic

Download

Filename:

DAX-PATHFINDER-v3.itf

Downloads:

1158

Veteran

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...