Navigator DAX Trading Strategy 4H

{kind=link}

Hi guys,

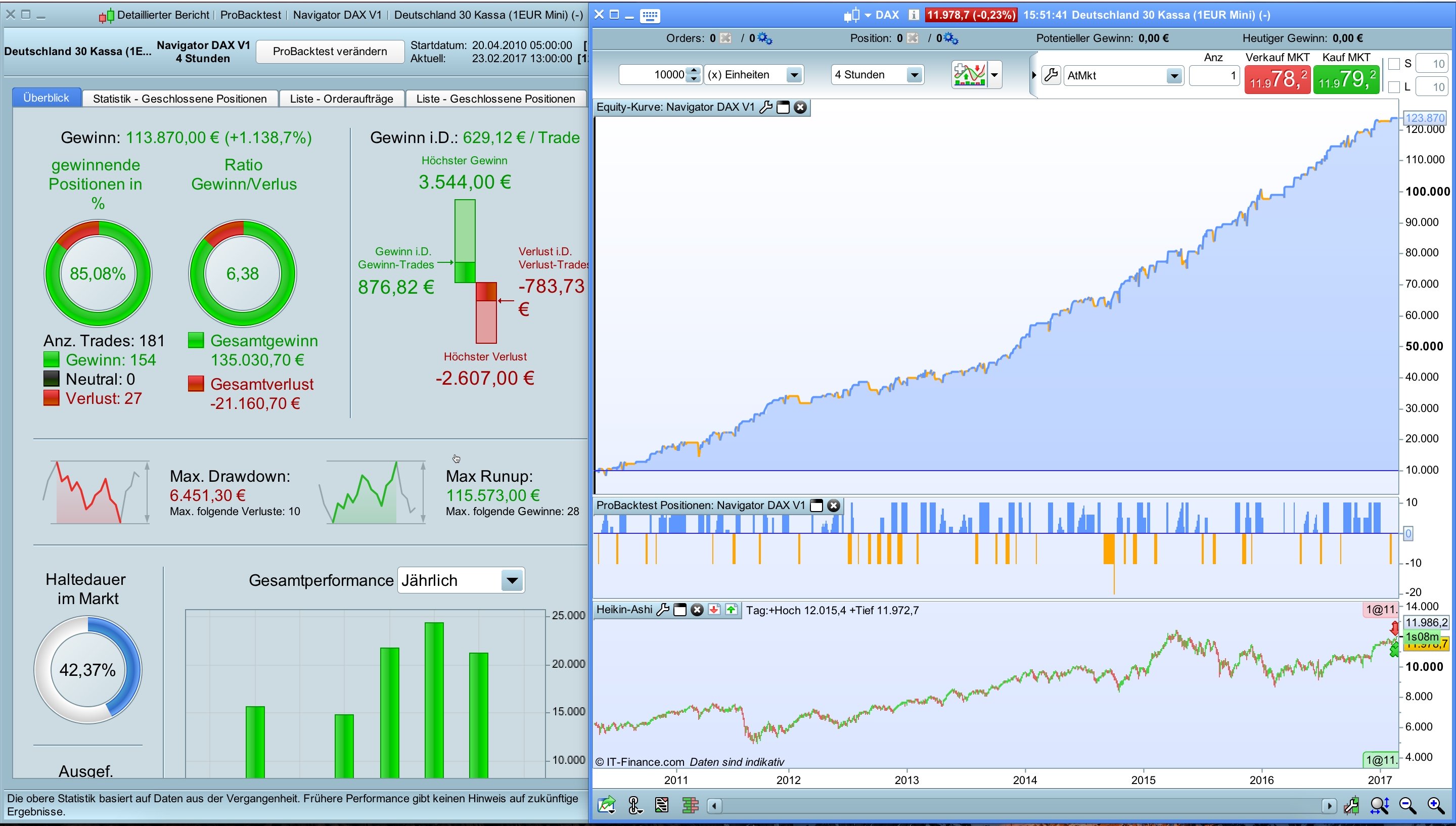

The tendency of the last and first days of the month is one of the most well known and reliable statistical setups. This pattern has been working for decades and in many indices. I would like to share a trading system that based on the TDOM (trading day of the month) idea from Larry Williams one of the famous statistical traders.

The basic idea is to short the market on the first trading day of the month and to turn the position at the statistical monthly turning point. The system uses smart position management mechanism such as order cumulation, position sizing based on historical monthly behavior and maximal position size monitoring. Money management will be done by procentage stop loss and take profit orders.

The system is very simple but amazing profitable and works without any technical indicators.

The so-called Navigator trading system works in 4 hours timeframe and the backtest was done with 200.000 candles. Please find attached the first version for the DAX.

Reviews and suggestions for improvement are welcome.

I have created a forum topic for all discussions related to Navigator Trading System.

https://www.prorealcode.com/topic/navigator-trading-system/

Best, Reiner

// Navigator Trading System based on ProRealTime 10.3

// The algo based on the statistical advantage of the TDOM (trading day of the month) idea around the turn of the month

// Version 1

// Instrument: DAX mini 1 EUR, 4H, 9-17 CET, 1 point spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders

// define TDOM days

ONCE tradingDaySell = 1

ONCE tradingDayBuy = 8

// define intraday trading window

ONCE timeSell = 90000

ONCE timeBuy = 170000

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 10

ONCE maxPositionSizeShort = 10

ONCE minSizeLong = 1

ONCE midSizeLong = 5

ONCE maxSizeLong = 10

ONCE maxSizeShort = -10

ONCE stopLossLong = 8.5 // in %

ONCE takeProfitLong = 3 // in %

ONCE stopLossShort = 3.75 // in %

ONCE takeProfitShort = 1 // in %

// define position multiplier for each month (>0 - long / <0 - short / 0 - no trade)

ONCE longJanuary = 0

ONCE shortJanuary = maxSizeShort

ONCE longFebruary = 0

ONCE shortFebruary = maxSizeShort

ONCE longMarch = maxSizeLong

ONCE shortMarch = 0

ONCE longApril = minSizeLong

ONCE shortApril = 0

ONCE longMay = minSizeLong

ONCE shortMay = maxSizeShort

ONCE longJune = minSizeLong

ONCE shortJune = 0

ONCE longJuly = midSizeLong

ONCE shortJuly = maxSizeShort

ONCE longAugust = 0

ONCE shortAugust = maxSizeShort

ONCE longSeptember = 0

ONCE shortSeptember = maxSizeShort

ONCE longOctober = midSizeLong

ONCE shortOctober = maxSizeShort

ONCE longNovember = midSizeLong

ONCE shortNovember = maxSizeShort

ONCE longDecember = midSizeLong

ONCE shortDecember = maxSizeShort

// calculate TDOM

IF Month <> Month[1] THEN

tradingDay = 0

ENDIF

IF Time = 90000 THEN

IF CurrentDayOfWeek > 0 AND CurrentDayOfWeek < 6 THEN

tradingDay = tradingDay + 1

ENDIF

ENDIF

// set montly multiplier

IF CurrentMonth = 1 THEN

monthlyMultiplierLong = longJanuary

monthlyMultiplierShort = shortJanuary

ELSIF CurrentMonth = 2 THEN

monthlyMultiplierLong = longFebruary

monthlyMultiplierShort = shortFebruary

ELSIF CurrentMonth = 3 THEN

monthlyMultiplierLong = longMarch

monthlyMultiplierShort = shortMarch

ELSIF CurrentMonth = 4 THEN

monthlyMultiplierLong = longApril

monthlyMultiplierShort = shortApril

ELSIF CurrentMonth = 5 THEN

monthlyMultiplierLong = longMay

monthlyMultiplierShort = shortMay

ELSIF CurrentMonth = 6 THEN

monthlyMultiplierLong = longJune

monthlyMultiplierShort = shortJune

ELSIF CurrentMonth = 7 THEN

monthlyMultiplierLong = longJuly

monthlyMultiplierShort = shortJuly

ELSIF CurrentMonth = 8 THEN

monthlyMultiplierLong = longAugust

monthlyMultiplierShort = shortAugust

ELSIF CurrentMonth = 9 THEN

monthlyMultiplierLong = longSeptember

monthlyMultiplierShort = shortSeptember

ELSIF CurrentMonth = 10 THEN

monthlyMultiplierLong = longOctober

monthlyMultiplierShort = shortOctober

ELSIF CurrentMonth = 11 THEN

monthlyMultiplierLong = longNovember

monthlyMultiplierShort = shortNovember

ELSIF CurrentMonth = 12 THEN

monthlyMultiplierLong = longDecember

monthlyMultiplierShort = shortDecember

ENDIF

// all in if first day of month is Monday or Thuesday

IF tradingDay = tradingDayBuy AND ( CurrentDayOfWeek = 1 OR CurrentDayOfWeek = 2 ) THEN

monthlyMultiplierLong = maxSizeLong

ENDIF

// caculate current position profit

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

// open long position with order cumulation

l1 = tradingDay = tradingDayBuy

l2 = tradingDay > tradingDayBuy AND posProfit < 0

IF ( (l1 OR l2) AND Time = timeBuy) THEN

// check monthly setup and max position size

IF monthlyMultiplierLong > 0 THEN

IF (COUNTOFPOSITION + (positionSize * monthlyMultiplierLong)) <= maxPositionSizeLong THEN

BUY positionSize * monthlyMultiplierLong CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierLong <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// sell short if valid month or close position only

s1 = tradingDay = tradingDaySell

IF ( s1 AND Time = timeSell ) THEN

// check monthly setup and max position size

IF monthlyMultiplierShort < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(monthlyMultiplierShort))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(monthlyMultiplierShort) CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeShort THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort = 0 THEN

SELL AT MARKET

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit