The "Little Turtle" strategy

{kind=link}

I had the idea of this little code, wishing to implement a strategy deviated from the famous “Turtle” strategy : a breakout above a last high on a certain period.

The code is very simple : we trade with the breakout of the 100 last days ; and so for the exit. Of course you can test with other parameters the value “100” days , but it seems to me profitable on most indices.

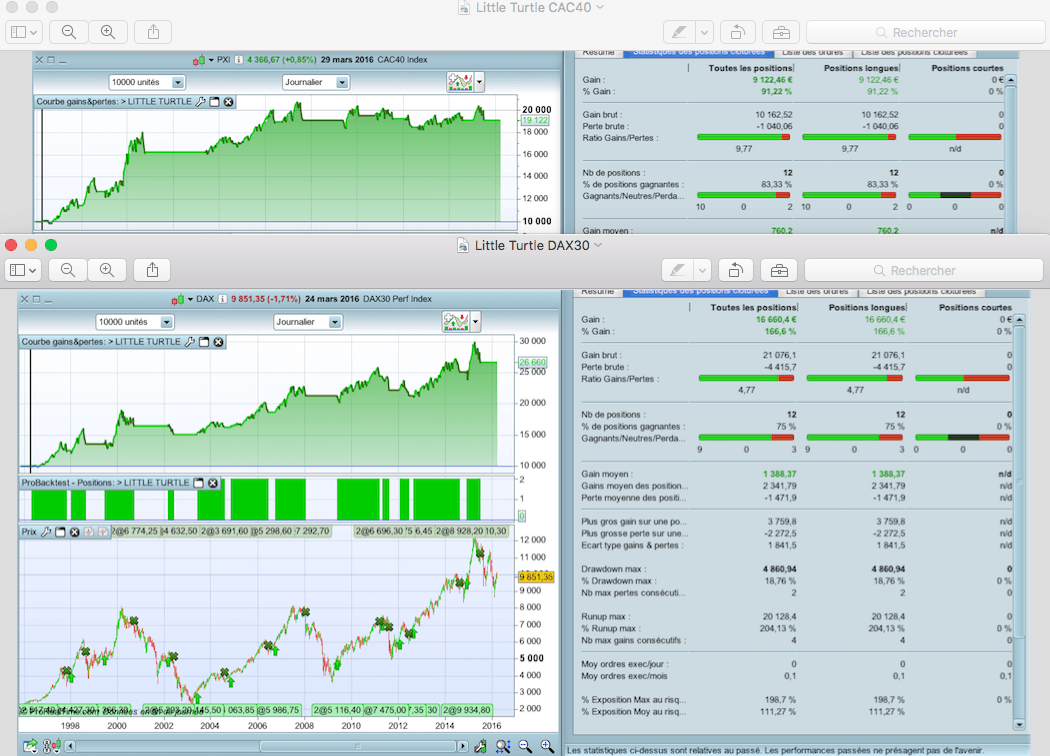

Indeed , this code is performing very well on the CAC40 (83.3 % success , profit factor of 9.7 !), The DAX30, the S&P500, even the NIKKEI, etc.

After weeks of very hard work, and with some other parameters, I did finally succeed to develop a very high-performance code on the Dax (5 times more profit than this code, with 2x less drawdown), which I use each day.

For now, I suggest you try this mini-code, which proves to be effective for long-term investment.

Defparam cumulateorders = false

n = 2

REM ACHAT

// Le + haut du jour dépasse le +haut des 100 jours précédents

ca1 = high > highest[100](high[1])

IF ca1 THEN

BUY n shares AT MARKET

ENDIF

REM SORTIE ACHAT

// Le + bas du jour dépasse le +bas des 100 jours précédents

ca2 = low < lowest[100](low[1])

IF ca2 THEN

SELL AT MARKET

ENDIF