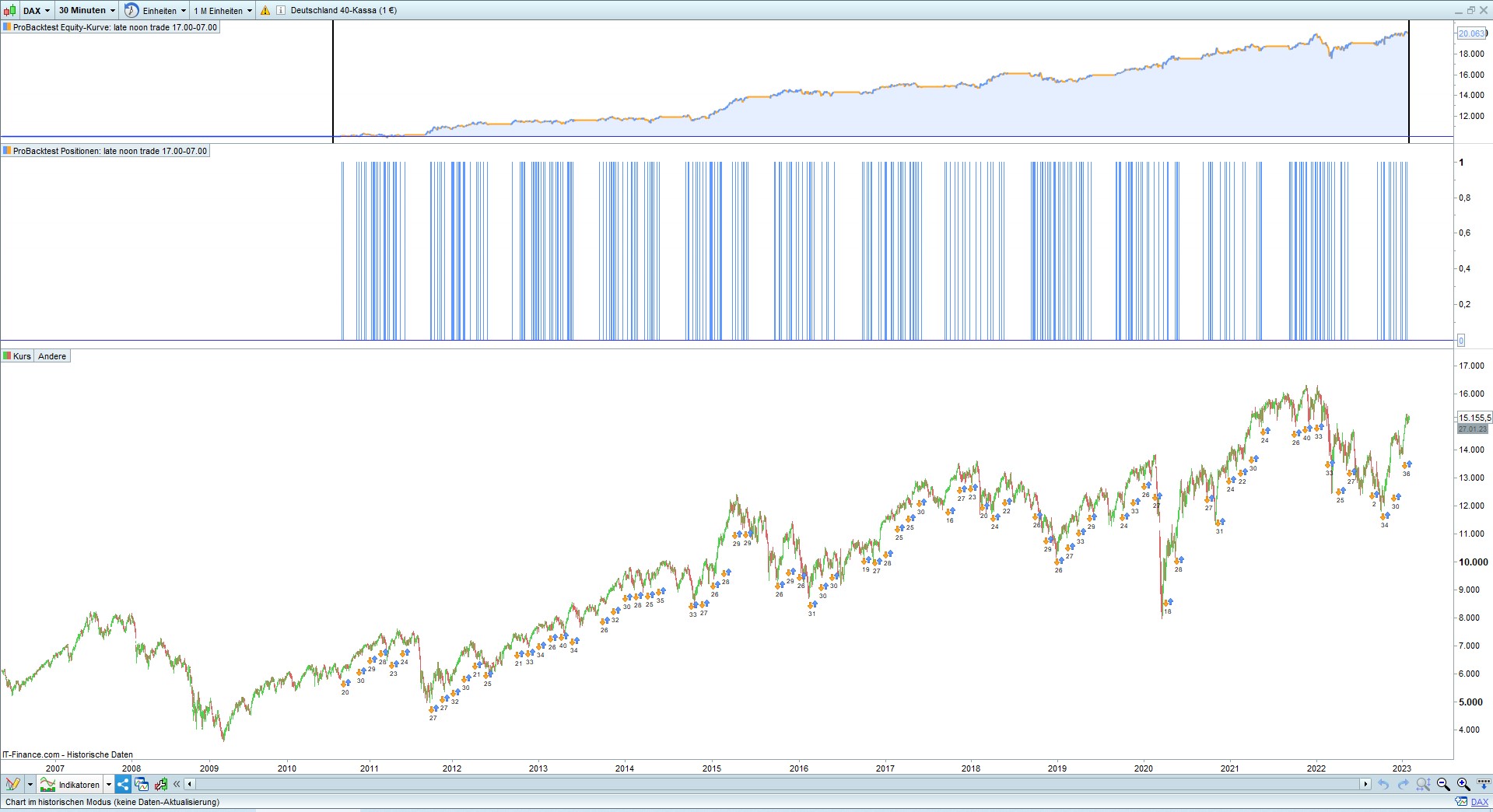

Late lunch trade DAX40 strategy

{kind=link}

While searching for profitable strategies, I came across something really simple in various forums and websites.

Basically it’s a trend following system and here we are only looking at the long side.

The trend is long when the price is above a higher average.

If the trend is long we take a long position after the morning tussle in the Dax at a late lunch. We hold the position overnight until the next morning and then liquidate it.

In my systems I like to set a filter after the time. Here for seasonal reasons some months and because of the over-weekend-risk friday are excluded.

As an explanation can be considered that the Dax follows the strong development of the S&P500 and DowJones shortly before and with their opening bell.

//-------------------------------------------------------

// late lunch trade

// instrument dax40

// timezone europe, berlin

// timeframe 30m

// created and coded by JohnScher

//-------------------------------------------------------

defparam cumulateorders= false

//defparam flatafter = 213000 // works too

once ordersize = 1

tm = openmonth <> 6 and openmonth <> 7 and openmonth <> 8

td = opendayofweek >= 1 and opendayofweek <= 4

tt = time = 133000

c = close > exponentialaverage [6] (close)

if tm and td and tt and c then

buy ordersize contracts at market

endif

if onmarket and time = 080000 then

sell at market

endif

set target %profit 1.5

// until then