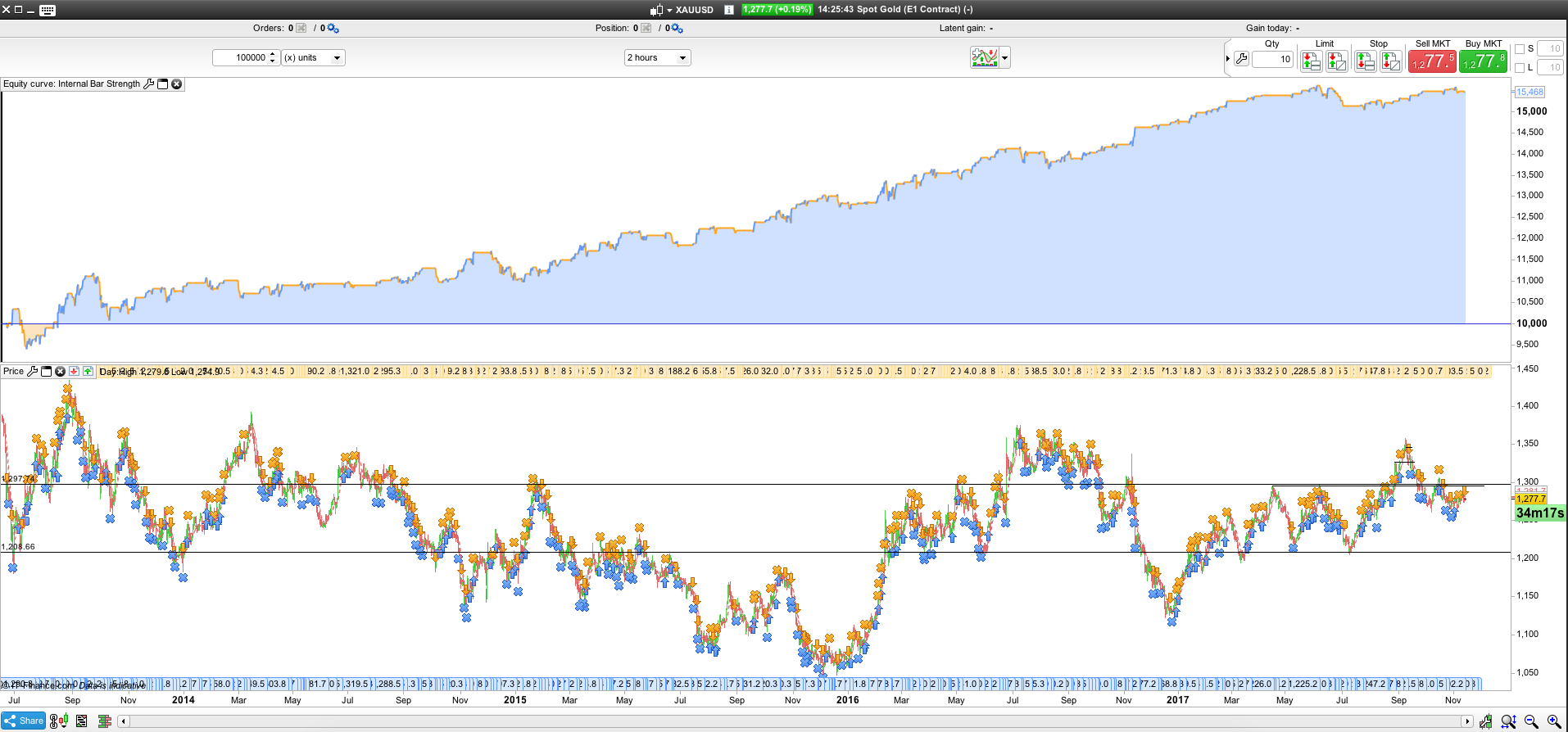

Internal Bar Strength Gold XAUUSD 2 hours TIMEFRAME

November 14, 2017, 9:48 AM

Strategies

8 Comments

{kind=link}

This strategy works on several markets but in this example I focused on gold.

The strategy is based on the Internal Bar Strength Indicator (IBS=(Close – Low) / (High – Low) * 100), and by using this indicator I’ve made a mean reversion strategy which basically gives you a high win rate thanks to a large stop loss distance. To find out if this is good or bad you need to do some further testing.

Anyhow, the main rule is as follow:

- Buy when the IBS closes below a certain value and exit when the price closes above yesterday’s high.

- Sell when the IBS closes above a certain value and exit when the price closes below yesterday’s low.

Apart from the main rule, I have also added some extra stuff to boost the performance of this backtest. You can optimise all of this in the top section.

Enjoy!

//////////////////////////////////////////////////////////////////

//// Sport Gold (E1 Contract) Spread 0.5

//////////////////////////////////////////////////////////////////

DEFPARAM CumulateOrders = False

DEFPARAM PreloadBars = 200

//////////////////////////////////////////////////////////////////

//// Opti

//////////////////////////////////////////////////////////////////

longtrigger = 9

shorttrigger = 91

maperiod = 100

maPeriod1 = 20 // Moving Average Period 100

maType1 = 2 // Moving Average function

stoplossmulti = 8

possize = 10

//////////////////////////////////////////////////////////////////

//// Indicators

//////////////////////////////////////////////////////////////////

IBS = (Close - Low) / (High - Low) * 100

ma = average[maperiod](close)

ma1 = average[maPeriod1, maType1](customClose)

slope1 = ma1 - ma1[1]

//////////////////////////////////////////////////////////////////

//// Entry conditions

//////////////////////////////////////////////////////////////////

b1 = not longonmarket // only open 1 position

b1 = b1 and close < Dhigh(1) // close below yesterday's high

b1 = b1 and IBS < longtrigger // Internal bar strength below trigger value

b1 = b1 and close > ma // close over moving average

b1 = b1 and slope1 > 0 // ma slope is positive

s1 = not shortonmarket // only open 1 position

s1 = s1 and close > Dlow(1) // close above yesterday's low

s1 = s1 and IBS > shorttrigger // Internal bar strength below trigger value

s1 = s1 and close < ma // close over moving average

s1 = s1 and slope1 < 0 // ma slope is negative

//////////////////////////////////////////////////////////////////

//// Exit conditions Short

//////////////////////////////////////////////////////////////////

el1 = close > Dhigh(1) // close above yesterday's high

es1 = close < Dlow(1) // close below yesterday's low

//////////////////////////////////////////////////////////////////

//// Execution

//////////////////////////////////////////////////////////////////

if b1 then

buy possize contract at market

endif

if s1 then

sellshort possize contract at market

endif

if el1 then

sell at market

endif

if es1 then

exitshort at market

endif

//////////////////////////////////////////////////////////////////

//// Stop loss

//////////////////////////////////////////////////////////////////

set stop ploss (averagetruerange[14] * stoplossmulti)*pointsize

Download

Filename:

Internal-Bar-Strength.itf

Downloads:

509

Veteran

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...