Index/bond strategy based on slow accumulation of contrarian orders (BUY) and MoneyManagement "antimartingala" style

{kind=link}

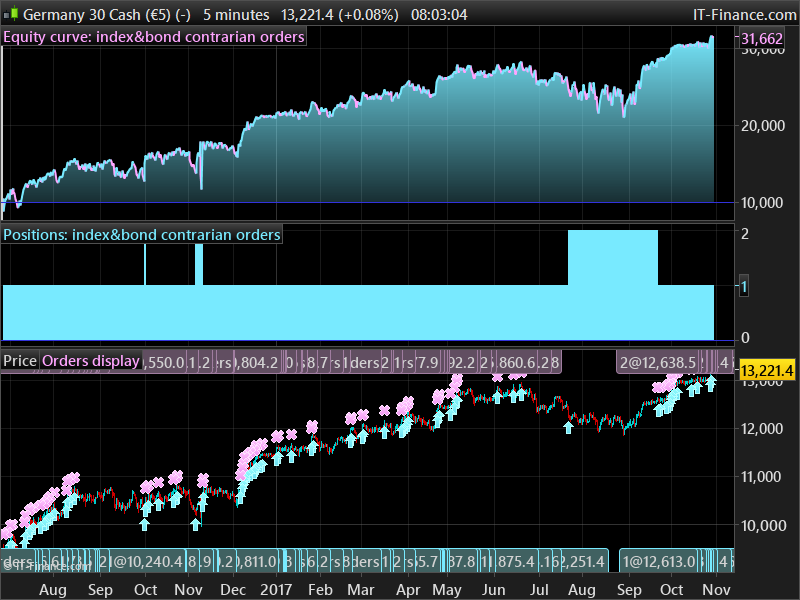

hi,

I reviewed the last strategy using contrarian orders and I added more filters in order not to accumulate too much contracts.

The base logic is “buy”.

Furthermore the system try to follow automatically the uptrend when it appears.

Inside the code I trid to explain the main parameters to use.

Actually such code is the automatisation of a my old “manual” strategy that I use since 2010 (using a simply Excel that give me the operating signals) using ETF instruments (It seems to me that even on IG it is possible to use ETF – isn’t it?).

The strategy that I am posting today works on long periods of time, so the broker (i.e. IG) withdraw an amount of cash every night (CFD cash) .

For what I know this is a blocking problem because overnight interest destroy any good strategy.

If I am wrong on what I’m saying please let me know if you can help me to resolve this problem (that’s why I sopke about ETF instrument which are not hit by this issue).

Moreover using CFD future with own expiry date I suppose that the issue on overnight interest doesn’t exist. Isn’t it?

But this way, how can I think to use an automatic strategy if I have to rollover every expiry date ?

What do you think on this ? keep in mind that I’m not an expert on future …. 🙂

Anyway I would be happy if you can “play” with the parameters of my strategy in order to know your opinion (let’s try on the main index or monetary market).

Thx a lot.

code:

//-----------------------------------------------------------------------------------------------

//TF a 12 h

//dax min 1 Eur.

//-----------------------------------------------------------------------------------------------

//TAKE PROFIT NEAR ZERO IN ORDER TO NOT ACCUMULATE TOO MUCH

//-----------------------------------------------------------------------------------------------

//IF NOT ON MARKET TRY TO ENTER AGAIN AS SOON A CORRECTION APPEARS, TRYING TO FOLLOW

//THE POTENTIAL CURRENT UPTREND

//-----------------------------------------------------------------------------------------------

//IF I BOUGHT THE PREVIOUS BAR DON'T BUY THE FOLLOWING BAR IN ORDER TO NOT ACCUMULATE TOO MUCH

//-----------------------------------------------------------------------------------------------

//MAIN PARAMETER IN ORDER TO CHANGE THE RISK LEVEL ARE:

//acc----> % of decrease of the instrument compared to the last buy price (THE LOWER IS AND MORE

// RISK AND CASH RETURN WILL APEEAR)

//-----------------------------------------------------------------------------------------------

//tp-----> % beyond which the entire position is closed (THE HIGHER IS AND MORE

// RISK AND CASH RETURN WILL APEEAR) - below zero is safer !

//-----------------------------------------------------------------------------------------------

//MONEY MANAGENT "ANTIMARTINGALA" STYLE - I SUPPOSE CLEARER RESULTS ON A LONGER PERIOD OF BACKTEST

//-----------------------------------------------------------------------------------------------

DEFPARAM cumulateorders = true

TIMEWORK = 070000

TIMESTOP = 210000

acc = 5

if justone = 0 then

capital = 10000 * pointvalue

justone = 1

endif

perccap = 0.5

margin = 0.5 * close * pointvalue / 100

period=5

stdev=STD[period](close)

//LOOK FOR A LOCAL VOLATILITY DECREASE

//I WANT TO BUY AGAIN ONLY WHEN BEAR MARKET SHOWS A LOCAL PAUSE

if (stdev[0]+stdev[1]+stdev[2]+stdev[3]+stdev[4]) < (stdev[1]+stdev[2]+stdev[3]+stdev[4]+stdev[5]) then

SWBUY=1

else

SWBUY=0

ENDIF

IF TIME > TIMEWORK AND TIME < TIMESTOP THEN

if not onmarket then

sizebuy = ROUND((capital *perccap /100)/ margin)

tp = 0.25

IF CLOSE < CLOSE[1] THEN

BUY sizebuy SHARES AT MARKET

endif

endif

if LONGONMARKET then

perf = (close - POSITIONPRICE)/POSITIONPRICE * 100

if perf > tp then

SELl AT MARKET

perfc = (close - POSITIONPRICE) * POINTVALUE * COUNTOFPOSITION

capital = capital + PERFC

ELSE

IF LASTBARBUY = 0 THEN

if (((CLOSE-TRADEPRICE)/TRADEPRICE)*100) < -acc AND SWBUY=1 then

sizebuy = ROUND((capital *perccap /100)/ margin)

BUY sizebuy SHARES AT MARKET

LASTBARBUY = 1

ENDIF

ELSE

LASTBARBUY = 0

ENDIF

ENDIF

ENDIF

ENDIF