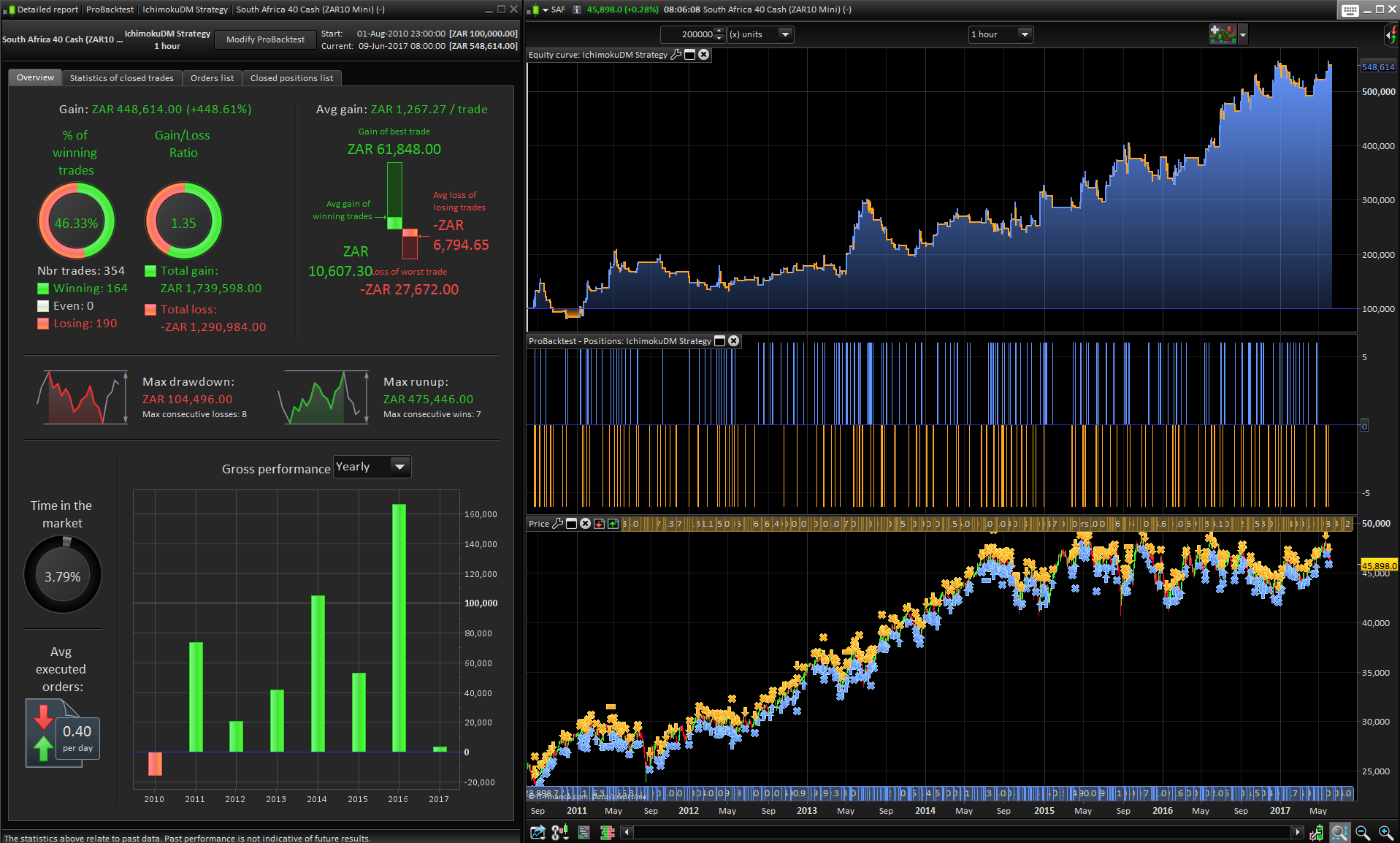

Ichimoku DM strategy SAF40 - 1 hour

June 9, 2017, 1:04 PM

Strategies

14 Comments

{kind=link}

I wrote this strategy today after studying some Ichimoku Trading Stategies.

It is mainly based around Ichimoku breakout strategy but also includes checks for Directional Movement and Divergence.

I wrote it for my local market (South Africa 40 Cash) on the 1Hr Timeframe on which it performs okay, which is no mean feat.

But to be completely honest i am disappointed with Ichimoku as an automated strategy in general.

But enough mumbling. Here is the code, maybe someone will find it useful.

Time schedule are adapted to intraday spread (8 points).

//Stategy: IchimokuDM

//Market: South Africa 40 Cash (ZAR2 Micro)

//Timeframe: 1Hr

//Spread: 15

//Timezone: UTC +2

Defparam Cumulateorders = False

Defparam Flatbefore = 073000

Defparam Flatafter = 163000

If hour < 9 or hour > 17 then //Works in conjunction with Flat Before/After time

possize = 0

If longonmarket then

SELL AT MARKET

ElsIf shortonmarket then

EXITSHORT AT MARKET

EndIf

Else

possize = 2 //Minimum position size

EndIf

P = 11 //Standard Period

R = P*2 //Standard Period x 2

I = P*3 //Standard Period x 3

TS = (highest[P](high)+lowest[P](low))/2 //Tenkan-Sen

KS = (highest[I](high)+lowest[I](low))/2 //Kijun-Sen

CS = close[I] //Chikou-Span

SA = (TS+KS)/2 //Senkou-Span A

SB = (highest[I](high)+lowest[I](low))/2 //Senkou-Span B

DP = DIplus[R](close) //DI+

DN = DIminus[R](close) //DI-

AX = ADX[R] //ADX

ATR = AverageTrueRange[P](close)

If RSI[R](close) > RSI[R](close[I]) Then

If close < CS Then

BDIV = 1 //Buy Divergence Present

SDIV = 0

EndIf

EndIf

If RSI[R](close) < RSI[R](close[I]) Then

If close > CS Then

BDIV = 0 //Sell Divergence Present

SDIV = 1

EndIf

EndIf

If countofposition = 0 and BDIV = 1 and AX > 17 and DP > 20 and DP > DN and close > SA and close > SB and TS > KS and close > CS and Close > SA[I] and Close > SB[I] Then

Buy possize*3 contracts at close + ATR stop

EndIf

If countofposition = 0 and SDIV = 1 and AX > 17 and DN > 20 and DP < DN and close < SA and close < SB and TS < KS and close < CS and Close < SA[I] and Close < SB[I] Then

Sellshort possize*3 contracts at close - ATR stop

EndIf

If Longonmarket then

If close < TS Then //If close below Tenkan-Sen Line

If close < close[1] Then

Sell at Market //Close position at next lower close

EndIf

EndIf

ElsIf Shortonmarket then

If close > TS Then //If close below Tenkan-Sen Line

If close > close[1] Then

Exitshort at Market //Close position at next higher close

EndIf

EndIf

EndIf

Set Stop pLOSS ATR*4

Set Target pPROFIT ATR*5

Download

Filename:

IchimokuDM-Strategy.itf

Downloads:

369

Master

My name is Juan Jacobs and I am an algorithmic trader and trading coach. After 7 years of corporate work as a Systems Analyst, I have decided to pursue my passion of trading on a full-time basis. My current focus area is that of 'smart' strategies based on 'Machine Learning'. You can find me at www.FXautomate.com or visit my PRC Marketplace Store here: https://market.prorealcode.com/store/fxautomate/

Author’s Profile

Loading...