Hang seng automatic trend following strategy with volatility filter

January 16, 2019, 1:44 PM

Strategies

12 Comments

{kind=link}

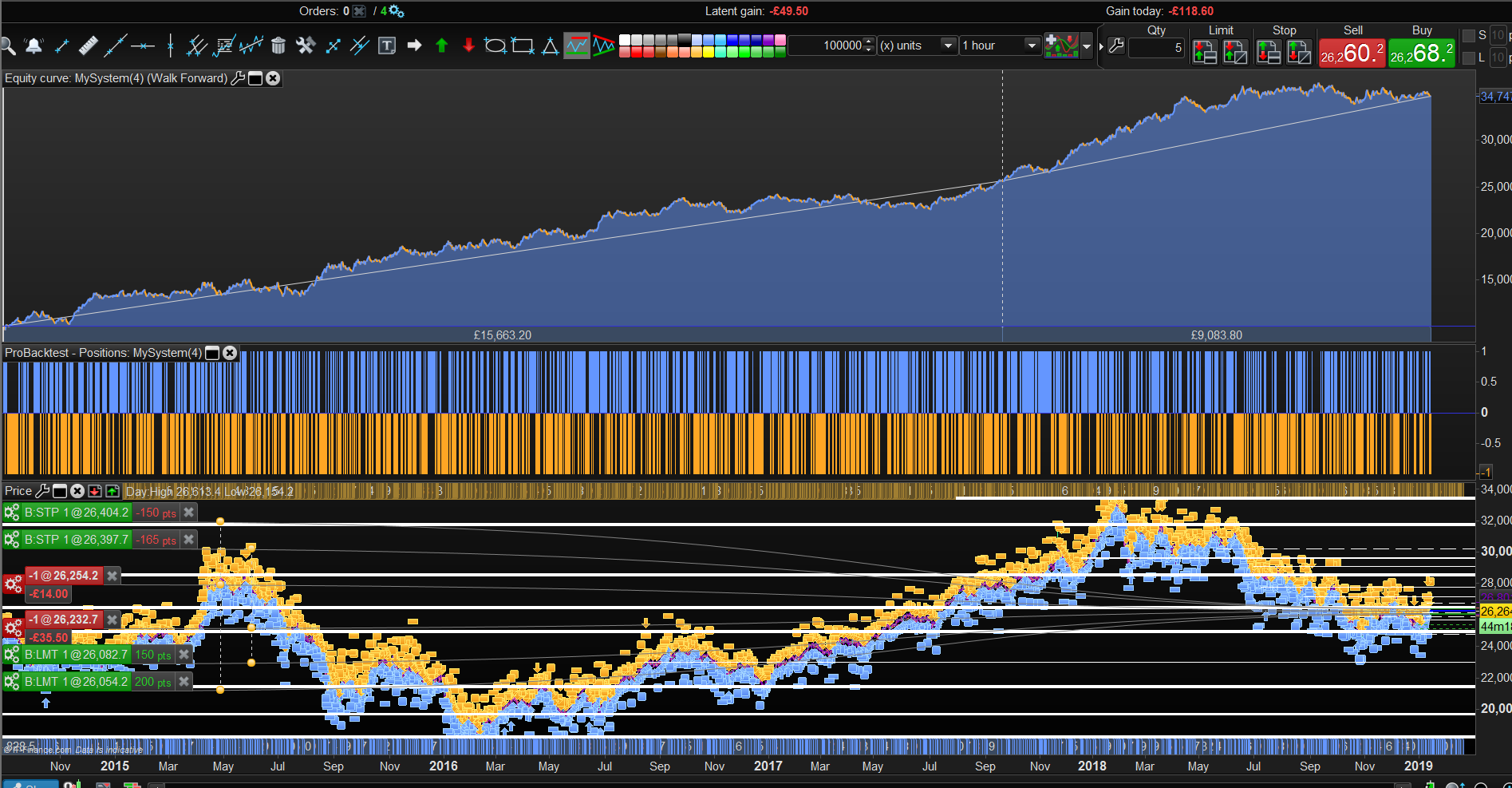

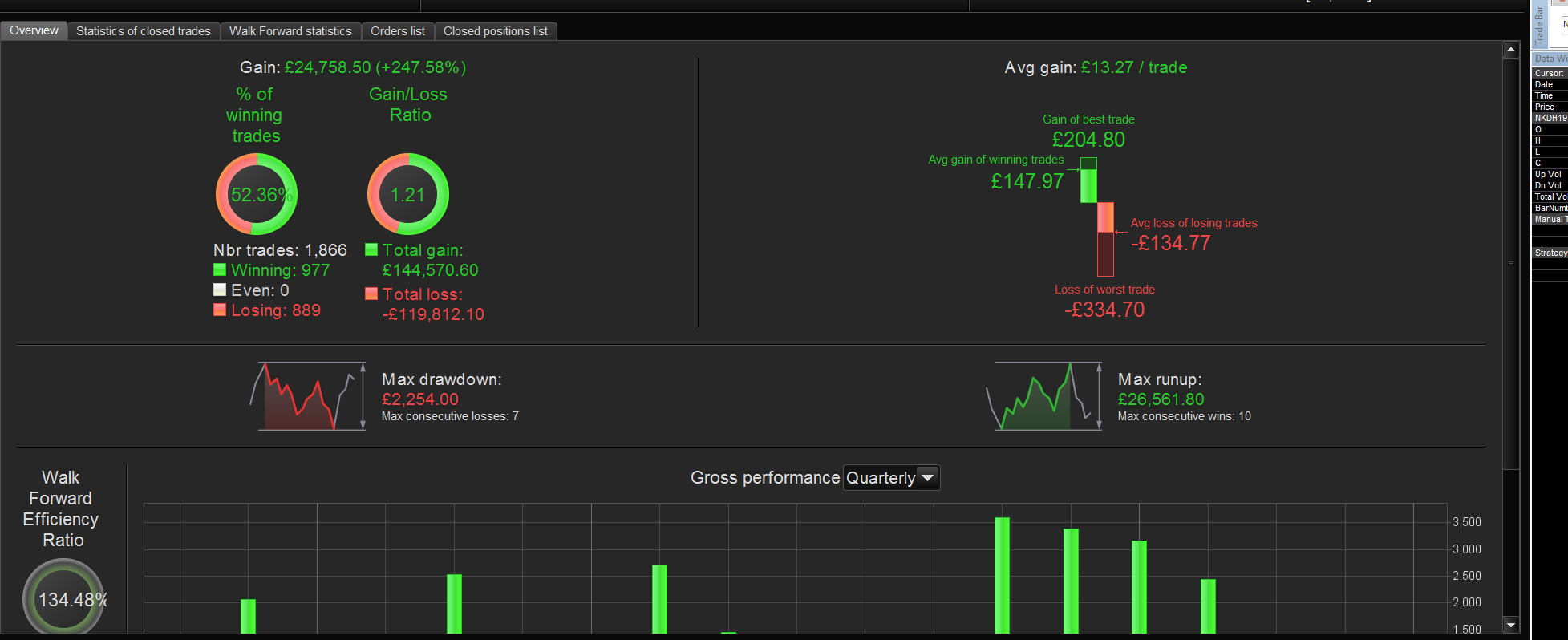

This HangSeng automatic trading strategy on the 1-hour timeframe, uses basic overbought and oversold RSI areas to open new orders and filtered with an average true range volatility filter.

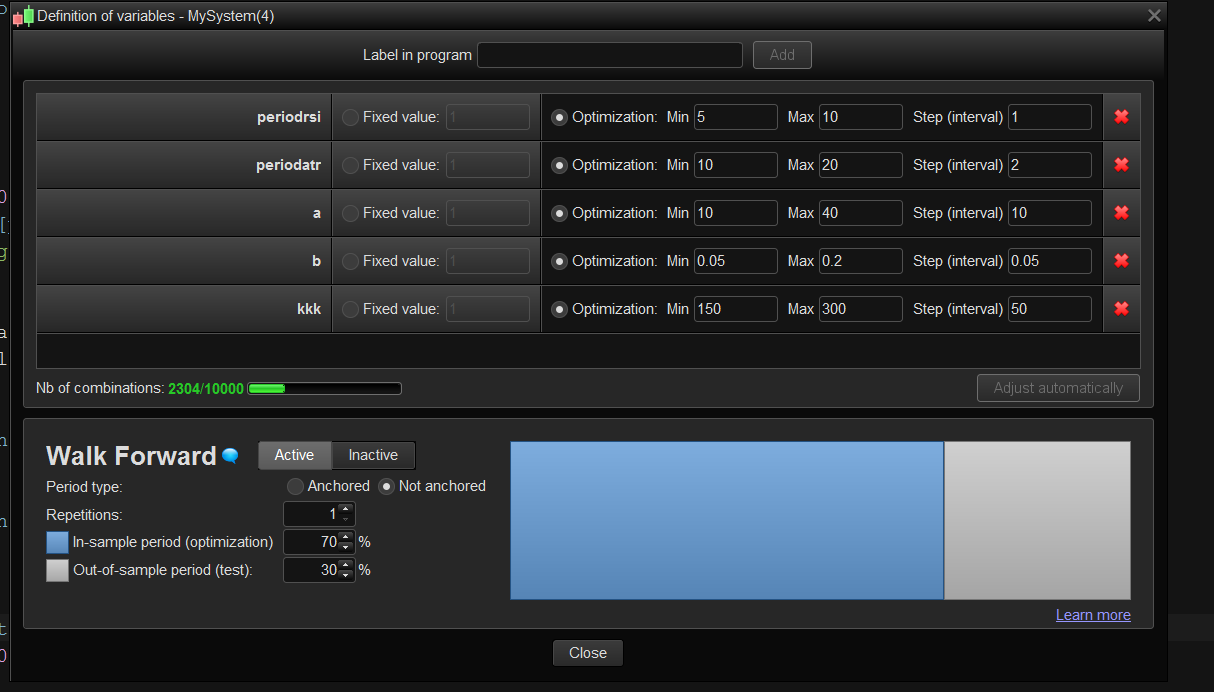

Results attached are from walk forward analysis with 1 OOS period proving robustness of the optimized variables. Variables to be optimized are also described in one of the attached picture.

Discussions about the strategy are running here: Hang seng trend following strategy with volatility filter H1 Time zone : UK

defparam cumulateorders = false

periodrsi = 8

periodatr = 16

a = 30

b = 0.15

timeok = time>20000 and time<120000

oscillator = rsi[periodrsi](close)

volindic = (averagetruerange[periodatr](close)/close)*100

oversold = oscillator<a and volindic>b and timeok

overbought =oscillator>100-a and volindic>b and timeok

if oversold then

sellshort 1 contract at market

endif

if overbought then

buy 1 contract at market

endif

set target pprofit 200

set stop ploss 150

Download

Filename:

HangSeng-H1-trend-n-volatility.itf

Downloads:

463

Download

{kind=link}

Filename:

wf_results_1-1.png

Downloads:

261

Download

{kind=link}

Filename:

wf_HS-1.png

Downloads:

264

Master

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...