Ftse mib morning inversion strategy 30 min TF

{kind=link}

Dear all,

This is my first strategy posted, I have coded this strategy based on my empirical experience, the idea is that Italy 40 index tends to invert directionality in the morning at 09:00 CET. 09:00 is the time when the future starts trading and is also the time when the index bid offer spread shrinks from around 25ticks to 6/7 ticks.

The fliter I used are:

- the previous day bar has a well defined directionality, parametrized by the variable b in the code, set at 120.

- the market is volatile enough: ATR[50] >20

The code force open and close at 30 minutes distance, open at 09:00 and closes at 09:30

In the code I also added an accumulator of positions, ading up positions as long as the strategy is profitable.

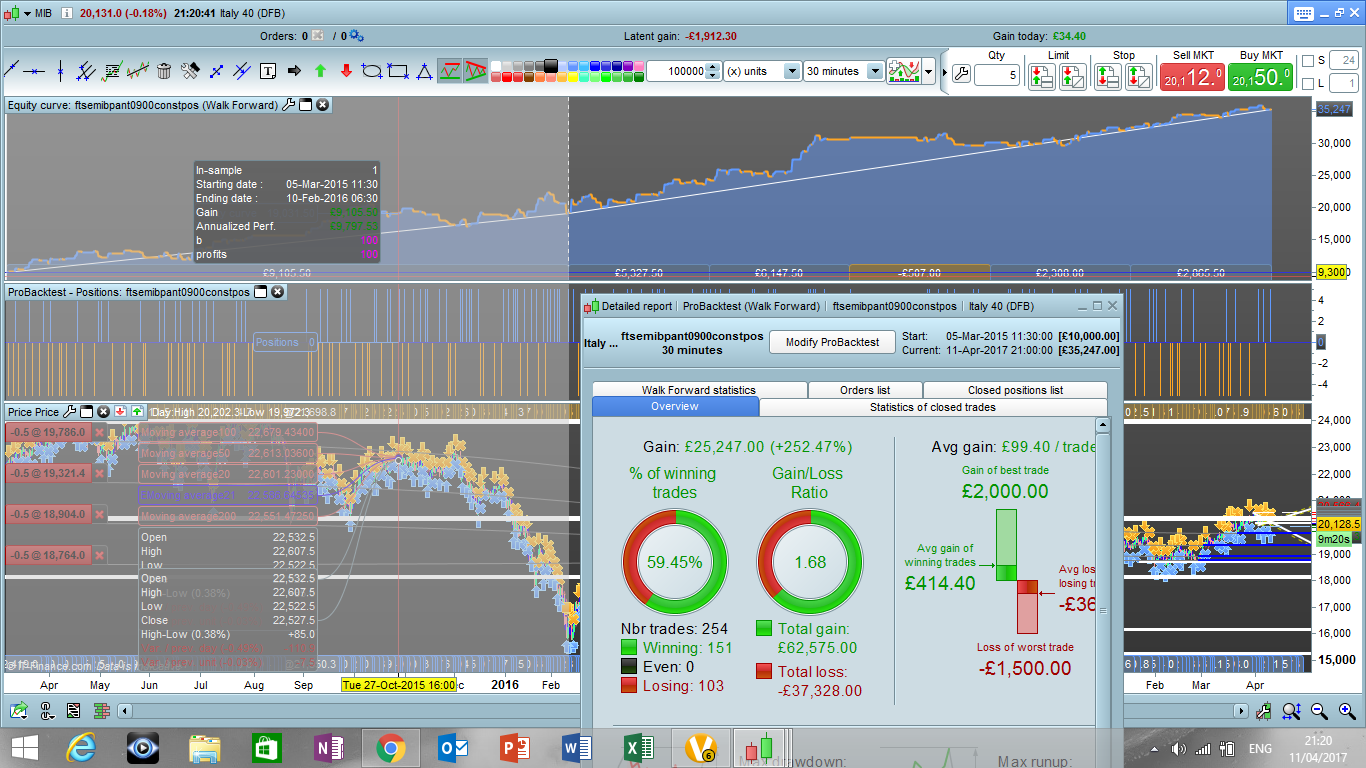

You find the results in the picture named btVP.png.

I also tried to do a walk forward analysis, with constant positions, and the results are in backtestwg.png

There is one thing to note before trying to run the code.

In the example I used a 30 minutes time frame in order to capture the longest possible timeseries, but pls be warned that in real you should open a position slightly later than 09:00:00 because the bid offer tightnes only after few seconds after. Ideally 09:01:00 should be fine.

As far as I know Nicolas has done a 200, 000 backtest and it looks that the strategy has worked consistently well up to 2013.

Any comment, improvement will be greatly appreciated.

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

timeenter = time = 090000

timeexit = time = 093000

indicator1 = AverageTrueRange[50](close)

volfilter= indicator1>20

b = 120

size = 5

increasestep = 2000

// Conditions to enter long positions

c1 = (DClose(1) <= DOpen(1)-b) and abs(dclose(1)-dopen(1))<900

NotAugust = CurrentMonth < 8 OR CurrentMonth > 8

if strategyprofit >=0 then

IF c1 AND timeenter and NotAugust and volfilter THEN

BUY size+round(strategyprofit/increasestep) PERPOINT AT MARKET

ENDIF

endif

if strategyprofit < 0 then

IF c1 AND timeenter and NotAugust and volfilter THEN

BUY size/2 PERPOINT AT MARKET

ENDIF

endif

if longonmarket AND timeexit and volfilter THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

c2 = (DClose(1) >= DOpen(1)+b)and abs(dclose(1)-dopen(1))<900

if strategyprofit >=0 then

IF c2 AND timeenter and NotAugust and volfilter THEN

SELLSHORT size+round(strategyprofit/increasestep) PERPOINT AT MARKET

ENDIF

endif

if strategyprofit < 0 then

IF c2 AND timeenter and NotAugust and volfilter THEN

SELLSHORT size/2 PERPOINT AT MARKET

ENDIF

endif

if shortonmarket AND timeexit THEN

EXITSHORT AT MARKET

ENDIF

// Stops and targets

SET STOP ploss 300

set target pprofit 400

{kind=link}

{kind=link}

{kind=link}