A forex trend breakout code

May 22, 2016, 7:19 PM

Strategies

2 Comments

{kind=link}

Hello,

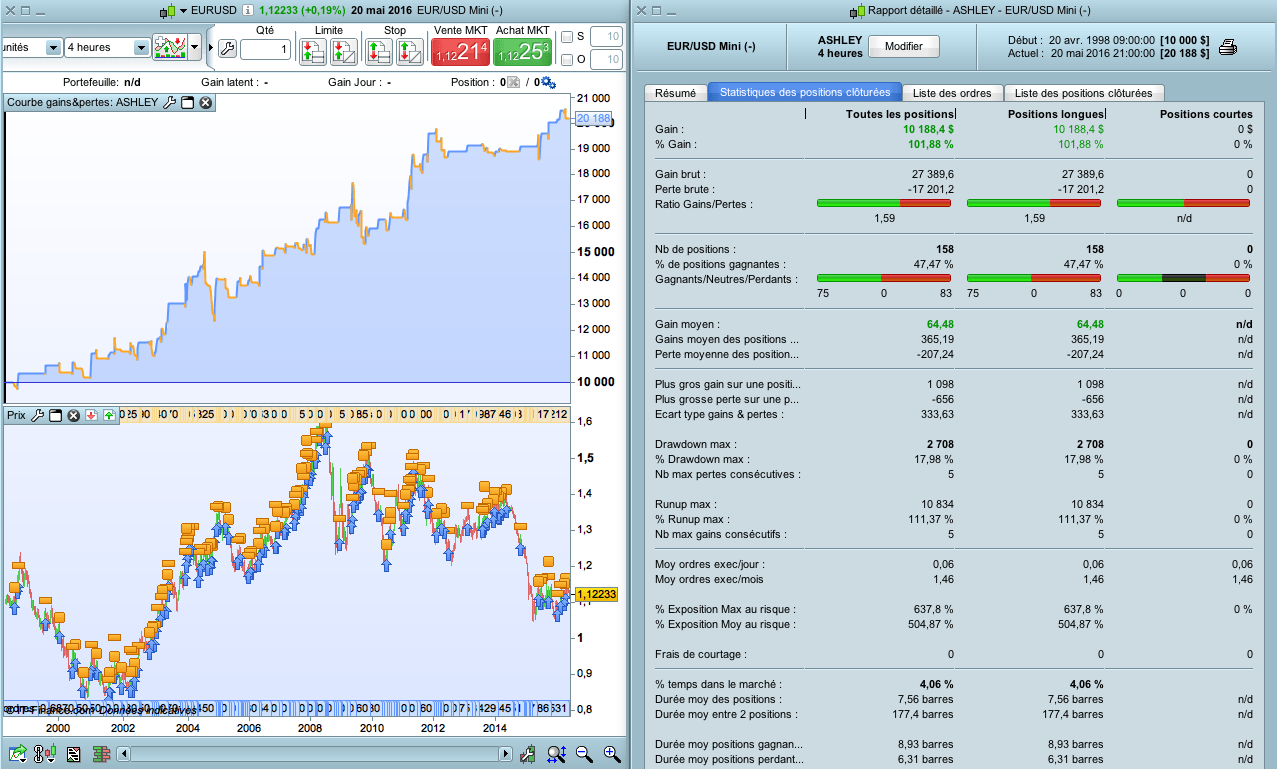

At the request of Ashley, I tried to backtest a strategy.

It was a failure on M15 and H1.

But the code works well for these conditions :

- H4 timeframe

- EUR/USD

- only long positions (works not great with shorts)

On H1, we must use “sell limit” instead of “buy stop”, it works with it !

So this code isn’t my best strategy of course, but the equity curve is sexy 🙂

// ASHLEY's strategy

// EUR/USD H4 minicontracts

EMA21 = exponentialaverage[21]

EMA40 = exponentialaverage[40]

EMA100 = exponentialaverage[100]

n = 4

Ctime = time > 040000 and time < 200000

// ACHAT

ca1 = EMA21 > EMA40 and EMA40 > EMA100

ca2 = EMA21 > EMA21[1] and EMA40 > EMA40[1] and EMA100 > EMA100[1]

ca3 = low < EMA21 and close > EMA21

ca4 = close > open and close > close[1] and close > open[1] and open <= open[1] and open <= close[1]

IF Ctime and ca1 and ca2 and ca3 and ca4 and not longonmarket THEN

SL = close - low

buy n shares at highest[1](high) stop

ENDIF

set stop loss SL

set target profit SL * 1.5

Download

Filename:

ASHLEY.itf

Downloads:

336

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...