Flying Fish: Trend-on-retracement rebound strategy

March 30, 2021, 12:55 PM

Strategies

19 Comments

{kind=link}

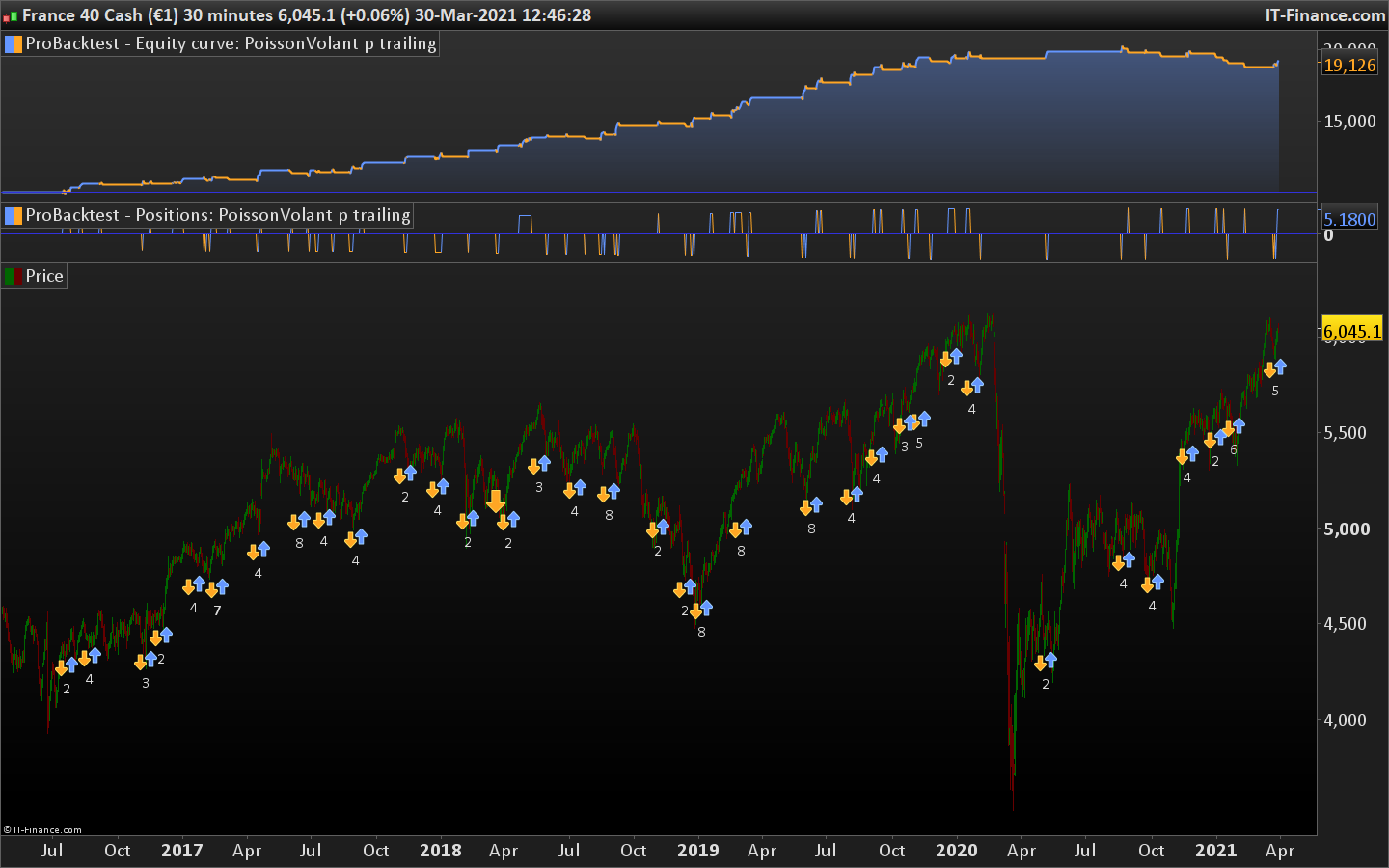

I propose this code which takes a position on trend rebounds at the 32.2% and 61.8% Fibonacci level with a Williams% R confirmation, and the Vwap Weekly as a trend indicator. I created this backtest on the CAC 40 in 30Min time frame But I think that this strategy can be applied to other assets and also be optimized.

The details are in the code in comments to help understanding.

Thank you

//================================================//

// ========== PARAMETRE GENERAUX ================ //

//================================================//

DEFPARAM CumulateOrders = false

// REINVESTISSEMENT DES GAINS

REINV = 1 // 0 = NON / 1 = OUI

IF REINV = 0 THEN

Capital = CapitalInit

ELSIF REINV = 1 THEN

Capital = CapitalInit + (strategyprofit*2/3)

ENDIF

//================================================//

// ========== PARAMETRES DES POSITIONS ========== //

//================================================//

// MONEY MANAGEMENT // 3 VARIABLES A PARAMETRER //

Capitalinit = 10000 // CAPITAL INITIAL

RisquePourc = 1.5 // RISQUE PAR TRADE EN %

DSL = 46 // DISTANCE AU STOP LOSS

RisquePartrade = capital*RisquePourc*0.01

RisqueParContrat = DSL*pipsize

N = RisquePartrade / RisqueParContrat

IF N < 1 then N = 1 endif // PLAGES HORRAIRES DE TRADING // CtimeAchat1 = time >= 080000 and time < 223000

//================================================//

// ========== PARAMETRE DES INDICATEURS ========= //

//================================================//

// RETRACEMENT DE FIBONACCI ET LOCALISATION DES ZONES // 1 VARIABLE A PARAMETRER //

NbCycle = 54 // NOTE : LE NOMBRE DE BOUGIE PRECEDENTE CORRESPOND A UN CYCLE , EXEMPLE 40 BOUGIES DE 30 MIN REPRESENTENT UN CYCLE DE 20H00 //

hh = highest[NbCycle](high) // hh est le plus haut des X bougies précédentes

ll = lowest[NbCycle](low) // LL est le plus bas des X bougies précédentes

amplitudefibo = ((hh - ll)/ll)*100 // L'amplitude est égale au plus haut des NBP précédentes

RT382 = ll+(hh-ll)*0.382 // Niveau de retracement 38,2%

RT618 = ll+(hh-ll)*0.618 // Niveau de retracement 61,8%

RT788 = ll+(hh-ll)*0.788 // Niveau de retracement 78,8%

// LES V-WAP YEARLY , MONTHLY ET DAYLY //

//calcule de la période

if DayOfWeek=0 or (dayofweek[1]=5 and dayofweek<>5) then

weekbar=barindex

endif

if month<>month[1] then

monthbar=barindex

endif

if year<>year[1] then

yearbar=barindex

endif

once dWeekly=1

once dMonthly=1

once dYearly=1

dWeekly = max(dWeekly, barindex-weekbar)

dMonthly = max(dMonthly, barindex-monthbar)

dYearly = max(dYearly, barindex-yearbar)

VWAPweekly = SUMMATION[dWeekly](volume*typicalprice)/SUMMATION[dWeekly](volume)

VWAPmonthly = SUMMATION[dMonthly](volume*typicalprice)/SUMMATION[dMonthly](volume)

VWAPyearly = SUMMATION[dYearly](volume*typicalprice)/SUMMATION[dYearly](volume)

// LE Volatility index //

PTotETMoving=20

PeriodET = 2 //"Ecart type"

PeriodTotET = 18 //"Période de recherche",minval=0)

PeriodEMA= 3 //"Période EMA",minval=0, type=input.integer)

BMax= 0.8 //"Borne Maximum",minval=0, type=input.float)

BMin= 0.2 //"Borne Minimum",minval=0, type=input.float)

ET = std[PeriodET]

ETmaxpostTotET=highest[PeriodTotET](ET)

if (PTotETMoving<PeriodTotET+PeriodET and barindex>PeriodET) then

PTotETMoving= PTotETMoving+1

if ETmaxPeriodET+PeriodTotET) then

ETmax=ETmaxpostTotET

endif

Volat=(ET/ETmax)

MMExp=average[PeriodEMA,1](volat)

//williams %R//

Catest = williams[22]<williams(close) and williams < -31 //================================================// // ======== LES CONDITIONS D'ENTREE LONG ======== // //================================================// //Les condition de Momentum// CaMom1 = hh > VWApWeekly // CONDITION MOMENTUM 1 :le cours cloture au dessus de la VWAP monthly

CaMom2 = VWAPWEEKLY > VWAPWEEKLY[21] // La Vwap weekly est ascendante : la vwap weekly cloture au dessus de la vwap weekly a 24 périodes

CaMom3 = MMExp < 0.2 // Le marché est toujours en zone d'accumulation : La Moyenne mobile exponentiel est au dessous de la borne Minimum Bmin //les conditions de localisation// //achat sur REBOND premier arrêt 38,2% de retracement// CaLoc4 = amplitudefibo > 0.8 //la hauteur minumum du mouvement de référence en pourcentage

CaLoc5 = amplitudefibo < 1.4 //La hauteur maximum du mouvement de référence en pourcentage

//ENTREE LONG SUR PREMIER ARRET //

//Les Conditions de figure //

CaFiG6 = LOWEST[1](low) < RT382 AND CLOSE[1] > RT382 //La bougie précédente croise les 38,2% de retracement mais cloture au dessus

//stoploss et take profit //

takeprofit = 2.02

Stoploss = (tradeprice*takeprofit/100)*0.5

If stoploss > DSL Then

stoploss = DSL

endif

If CtimeAchat1 AND CaMom1 AND CaMom2 AND CaMom3 AND CaLoc4 AND CaLoc5 AND CaFig6 and Catest THEN

BUY n SHARES AT MARKET

set target %profit takeprofit

set stop loss Stoploss ptrailing stoploss*1.02

ENDIF

//ENTREE LONG SUR RELOAD ZONE //

// les conditions de Momentum

CaMom1bis = hh > VWApWeekly // CONDITION MOMENTUM 1 :le cours cloture au dessus de la VWAP monthly

CaMom2bis = VWAPWEEKLY > VWAPWEEKLY[54] // La Vwap weekly est ascendante : la vwap weekly cloture au dessus de la vwap weekly a 24 périodes

CaMom3bis = MMExp < 0.18 // Le marché est toujours en zone d'accumulation : La Moyenne mobile exponentiel est au dessous de la borne Minimum Bmin CaLoc4bis = amplitudefibo > 0.8

CaLoc5bis = amplitudefibo < 1.4

//Les Conditions de figure //

CaFiG6bis = LOWEST[1](low) < RT618 AND CLOSE[1] > RT618 //La bougie précédente croise les 61,8% de retracement mais cloture au dessus

CaFig7bis = open>close

//stoploss et take profit //

takeprofitbis = 2.51

Stoplossbis = (tradeprice*takeprofit/100)*0.4

If stoplossbis > DSL Then

stoplossbis = DSL

endif

If CtimeAchat1 AND CaMom1bis AND CaMom2bis AND CaMom3bis AND CaLoc4bis AND CaLoc5bis AND CaFig6bis AND CaFig7bis and catest THEN

BUY n SHARES AT MARKET

set target %profit takeprofitbis

set stop loss Stoplossbis ptrailing stoplossbis*1.54

ENDIF

//===============================================//

// ======= LES CONDITIONS D'ENTREE SHORT ======= //

//===============================================//

//achat sur REBOND premier arrêt 38,2% de retracement//

//Les condition de Momentum//

CvMom1 = hh < VWApWeekly[75] // CONDITION MOMENTUM 1 :le cours cloture en dessous de la VWAP monthly

CvMom2 = VWAPWEEKLY < VWAPWEEKLY[22] // La Vwap weekly est ascendante : la vwap weekly cloture en dessous de la vwap weekly a 22 périodes CvMom3 = MMExp > 0.27 // Le marché est toujours en zone d'accumulation : La Moyenne mobile exponentiel est au dessous de la borne Minimum Bmin

CvWill = williams[9]<williams(close) //les conditions de localisation// CvLoc4 = amplitudefibo > 0.8 //la hauteur minumum du mouvement de référence en pourcentage

CvLoc5 = amplitudefibo < 1.95 //La hauteur maximum du mouvement de référence en pourcentage //ENTREE LONG SUR PREMIER ARRET SHORT// //Les Conditions de figure // CvFiG6 = HIGHEST[1](HIGH) > RT618 AND CLOSE[1] < RT618 //La bougie précédente croise les 38,2% de retracement mais cloture EN DESSOUS //stoploss et take profit // takeprofit = 1.98 StoplossV = (tradeprice*takeprofit/100)*0.44 If stoplossV > DSL Then

stoplossV = DSL

endif

If CtimeAchat1 AND CvMom1 and CvMom2 AND CvMom3 AND CvWill AND CvLoc4 AND CvLoc5 AND CvFig6 THEN

sellshort n SHARES AT MARKET

set target %profit takeprofit

set stop loss StoplossV ptrailing stoplossV*1.08

ENDIF

//achat sur REBOND premier arrêt 61.8% de retracement//

//Les condition de Momentum//

CvMom1Vbis = hh < VWApWeekly[64] // CONDITION MOMENTUM 1 :le cours cloture en dessous de la VWAP monthly

CvMom2Vbis = VWAPWEEKLY < VWAPWEEKLY[21] // La Vwap weekly est ascendante : la vwap weekly cloture en dessous de la vwap weekly a 22 périodes

CvMom3Vbis = MMExp < 0.49 // Le marché est toujours en zone d'accumulation : La Moyenne mobile exponentiel est au dessous de la borne Minimum Bmin

CvWillVbis = williams[43]<williams(close) and williams > -23

//les conditions de localisation//

CvLoc4Vbis = amplitudefibo > 0.8 //la hauteur minumum du mouvement de référence en pourcentage

CvLoc5Vbis = amplitudefibo < 1.3 //La hauteur maximum du mouvement de référence en pourcentage //ENTREE LONG SUR PREMIER ARRET SHORT// //Les Conditions de figure // CvFiG6Vbis = HIGHEST[1](HIGH) > RT382 AND CLOSE[1] < RT382 //La bougie précédente croise les 61.2% de retracement mais cloture EN DESSOUS //stoploss et take profit // takeprofitVbis = 2.57 StoplossVbis = (tradeprice*takeprofit/100)*0.44 If stoplossVbis > DSL Then

stoplossVbis = DSL

endif

If CtimeAchat1 AND CvMom1Vbis AND CvMom2Vbis AND CvMom3Vbis AND CvWillVbis AND CvLoc4Vbis AND CvLoc5Vbis AND CvFig6Vbis THEN

sellshort n SHARES AT MARKET

set target %profit takeprofitVbis

set stop loss StoplossVbis ptrailing stoplossVbis*1.1

ENDIF

Download

Filename:

PoissonVolant.itf

Downloads:

991

Average

Operating in the shadows, I hack problems one by one. My bio is currently encrypted by a complex algorithm. Decryption underway...

Author’s Profile

Loading...