Fisher Dax Daily

July 31, 2018, 10:38 AM

Strategies

3 Comments

{kind=link}

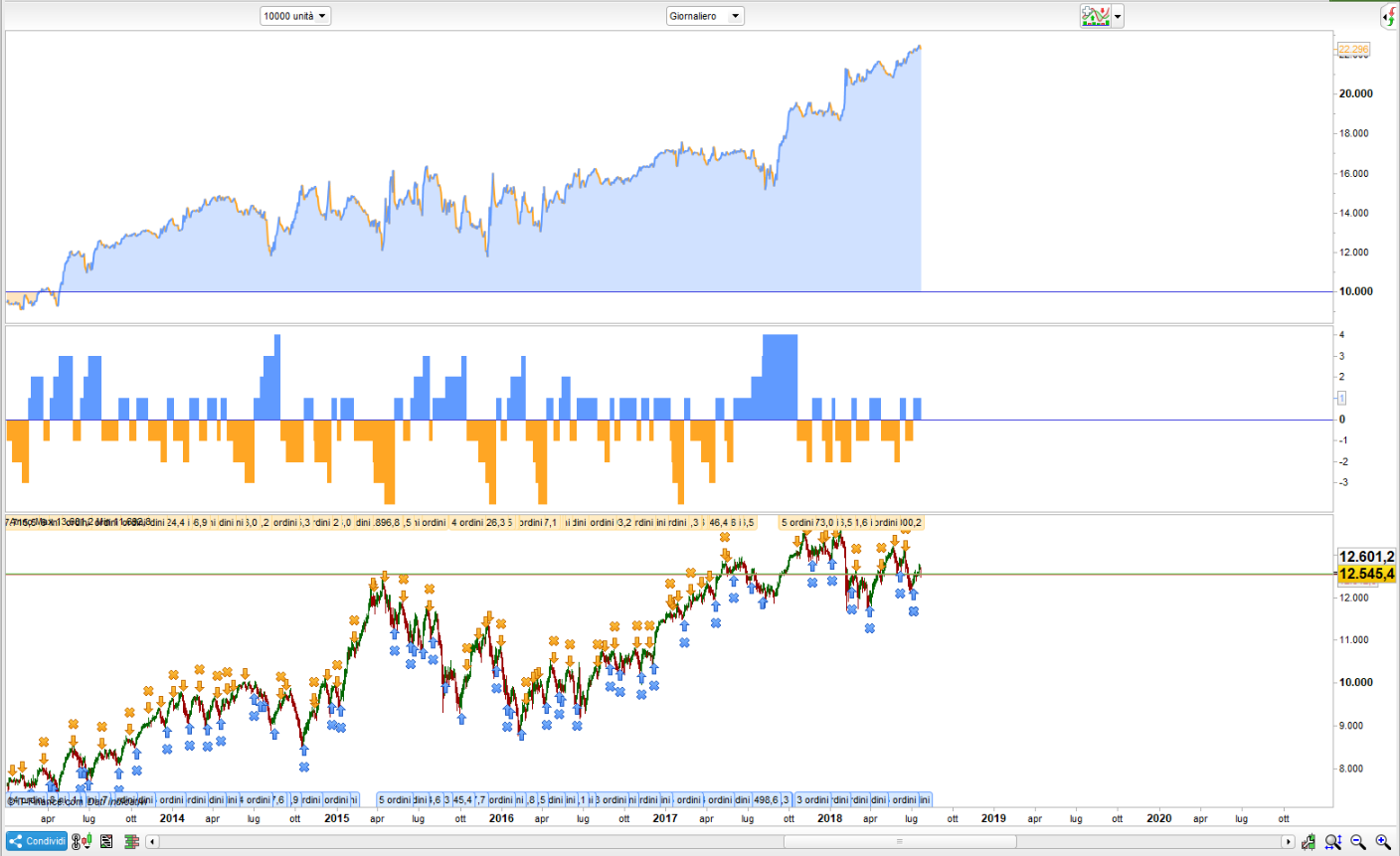

I would like to propose the following Daily Strategy on the Dax based on the Fisher Transform for any changes or opinions.

The Fisher Transform, with its rather complex mathematical formula, aims to create a function similar to a Gaussian probability density function. In this way, a very simple tool such as price is transformed into a technical indicator able to provide “extreme” signals to be exploited tactically.

the spread used is 1 tick

I left activated the cumulative functions, but they can be deactivated.

the system, as you can see, work on the stop and reverse of the fisher, almost always referring to the market.

DEFPARAM CumulateOrders = TRUE // Posizioni cumulate attivate

LEN=13

IF BARINDEX < len THEN

value1 = 0

fish = 0

ELSE

MaxH = Highest[len](TypicalPrice)

MinL = Lowest[len](TypicalPrice)

Value1 = ( (TypicalPrice - MinL)/(MaxH - MinL) - .5) + .67 * Value1

If Value1 > .99 then

Value1 = .999

ENDIF

If Value1 < -.99 then

Value1 = -.999

ENDIF

Fish = 0.5*Log((1 + Value1)/(1 - Value1)) + .5 * Fish

a=5

b=-5

ENDIF

IF fish CROSSES OVER b THEN

BUY 1 CONTRACT AT MARKET

ENDIF

IF fish CROSSES UNDER A THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

Download

Filename:

FISHER.itf

Downloads:

397

Senior

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...