"End of Day" forex trading strategy for USD/JPY

April 19, 2016, 3:51 PM

Strategies

30 Comments

{kind=link}

Hello everyone,

I wrote this code from a strategy that seemed extremely effective on the pair “USD / JPY “.

The problem is that the backtest I had seen did not use the spread, and had been tested over the last few years, which anyway were profitable.

So I rewrote a backtest with adaptation in H1 c

harts and spread of 1.5 points.

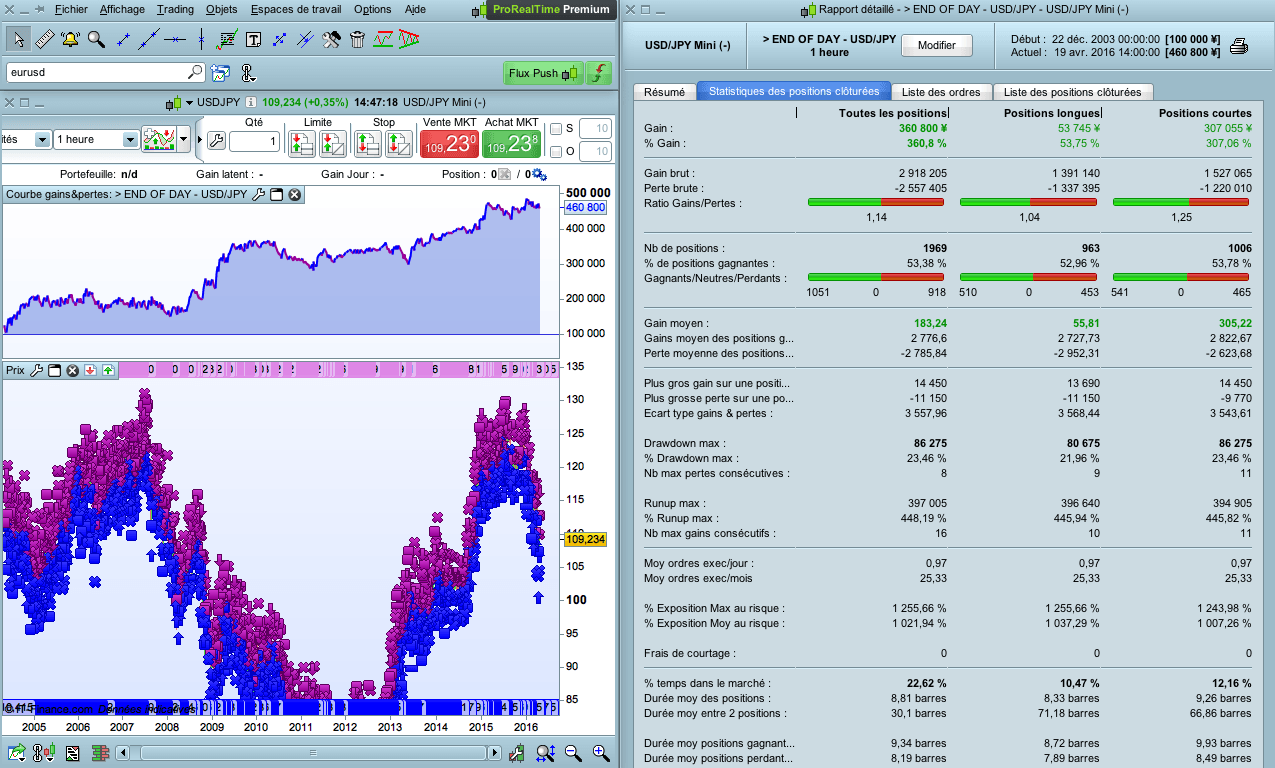

As you can see, the strategy

– is profitable in recent years

– can be positive on every forex pair (with some improvements for each pair)

– requires no indicator

Actually, we take position only between 22H and 23H, depending on the distance from the range period : 18H – 22H (this period can change with other pairs)

// Graphes H1

// Paire recommandée : USD/JPY

Defparam cumulateorders = false

// Levier (max conseillé : 1.5)

LEVIER = 1

// Choix du réinvestissement des gains ou non

REINV = 0

IF REINV = 0 THEN

n = 1*levier

ENDIF

IF REINV = 1 THEN

Capital = 100000 + strategyprofit

n = (capital / 100000)*levier

IF n <1 THEN

n = 1 // Taille minimum : 1

ENDIF

ENDIF

// Bougie référence 18 à 22H

If time = 220000 THEN

amplitude = highest[4](high) - lowest[4](low)

amplitude = amplitude*0.4

ouverture = close

ENDIF

// ACHAT & VENTE entre 22H et 23H

IF time >= 220000 and time <= 230000 THEN

Buy n shares at ouverture - amplitude limit

Sellshort n shares at ouverture + amplitude limit

ENDIF

// STOP & OBJECTIF

SET STOP %LOSS 0.6

SET TARGET %PROFIT 1.2

// SORTIE

IF time = 100000 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

Download

Filename:

End-of-Day-UsdJpy-H1.itf

Downloads:

530

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...