An effective GOLD Breakout strategy

July 18, 2016, 12:02 PM

Strategies

5 Comments

{kind=link}

Hello everyone,

I have used the “London Open Breakout” on the forex, a well known strategy.

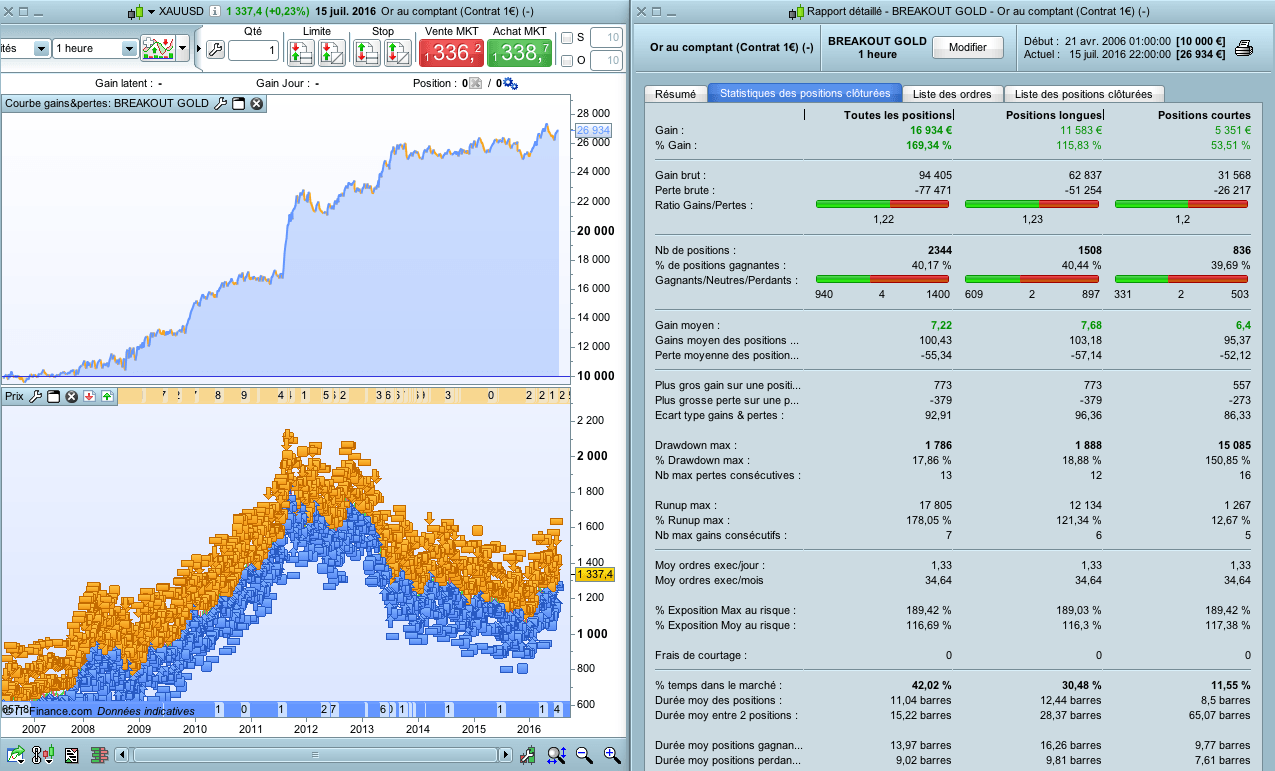

I had the idea to optimize it on Gold.

It is profitable, with the following entry rules:

- GOLD, contracts 1€, hourly timeframe

- the breakout takes reference to the period from 20PM to 5AM (8 candles for me, because on my display I have no candle between 23PM and 12AM)

- we take positions from 5AM to 18PM

- stop loss : the other side of the breakout channel

- take profit : 1.8 x stop loss

- no cumulation of orders

- if we are “long” and the next day we have a “short”, we close the “long” and go “short”

Others parameters are profitable, it should be easy to modify them and optimize this strategy :

- starting and ending of breakout channel

- starting and ending of positions

- stop loss / take profit

- accumulated positions

- etc.

This can be automated, of course.

On the screenshot, the backtest was made WITHOUT spread, as I don’t know it.

Best Regards,

Defparam cumulateorders = false

n = 10

// Timeframe : H1

// HORAIRES DU BREAKOUT : 20H à 05H

IF TIME = 050000 THEN

HAUT = highest[8](high)

BAS = lowest[8](low)

achatjour = 0

ventejour = 0

amplitude = haut-bas

ENDIF

Ctime = time >= 050000 AND time <= 180000

Ccanal = close < haut and close > bas

IF Ctime and Ccanal THEN

IF achatjour = 0 THEN

buy n shares at HAUT stop

ELSIF ventejour = 0 THEN

sellshort n shares at BAS stop

ENDIF

ENDIF

IF longonmarket THEN

achatjour = 1

ENDIF

IF shortonmarket THEN

ventejour = 1

ENDIF

set stop loss amplitude

set target profit amplitude*1.8

Download

Filename:

BREAKOUT-GOLD.itf

Downloads:

518

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...