Directional Index (DI) strategy

November 9, 2017, 8:41 AM

Strategies

2 Comments

{kind=link}

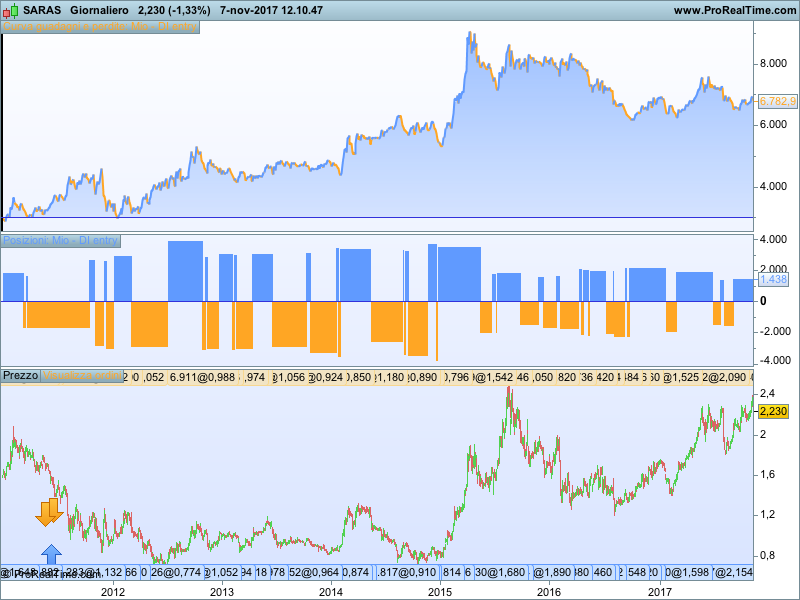

This is a strategy based on the Directional Index (DI) indicator created by Welles Wilder and modified by me at this link. It’s a “all-time-in” strategy in which you reverse your position when the signal is triggered. The trigger is based on the variations of DI index. You can also make it a long-only strategy by eliminating the short entry lines.

I strongly suggest to use this strategy with high CSI or, in case you are not a good friend of volatility, with a high ADXR.

I have never used real world this system but on the stock market, with no spread and 5 Euros of commissions seems to be pretty good.

Blue skies!!

// Definizione dei parametri del codice

DEFPARAM CumulateOrders = False // Posizioni cumulate disattivate

// Condizioni per entrare su posizioni long

ignored, ignored, mioDI, ignored, ignored, ignored = CALL "PRT - ADX e DI"[14, 2, 25]

if (mioDI[3]>mioDI[2]) and (mioDI[2]<mioDI[1]) and (mioDI>mioDI[2]) then

golong=1

goshort=0

endif

if (mioDI[3]<mioDI[2]) and (mioDI[2]>mioDI[1]) and (mioDI<mioDI[2]) then

goshort=1

golong=0

endif

if golong=1 and close>average[x](close) then

buy 3000 cash at high stop

endif

if goshort=1 and close<average[x](close)then

sellshort 3000 cash at low stop

endif

Download

Filename:

PRT-DI-strat.itf

Downloads:

295

Master

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...