DAX Trend following - 2-hours timeframe

January 17, 2019, 11:19 AM

Strategies

15 Comments

{kind=link}

This DAX automatic trading strategy on the 2-hours timeframe, use a basic cycle oscillator to test “overbought” and “oversold” areas to open new orders.

All orders have stoploss and takeprofit.

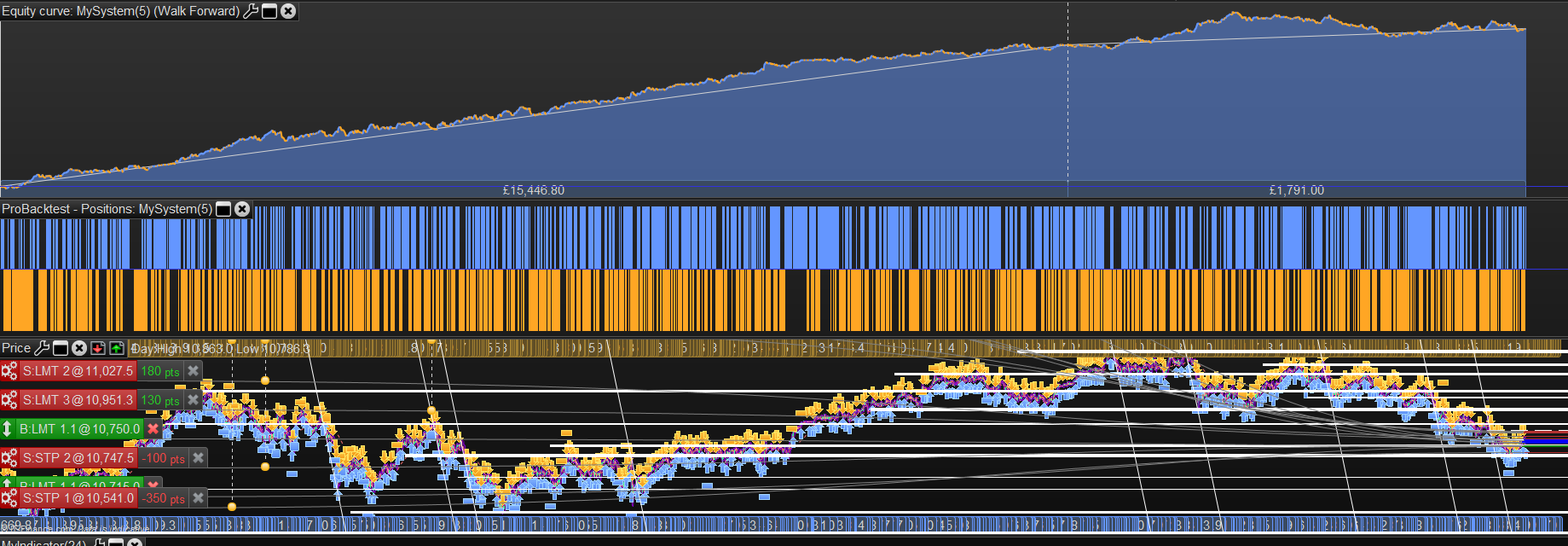

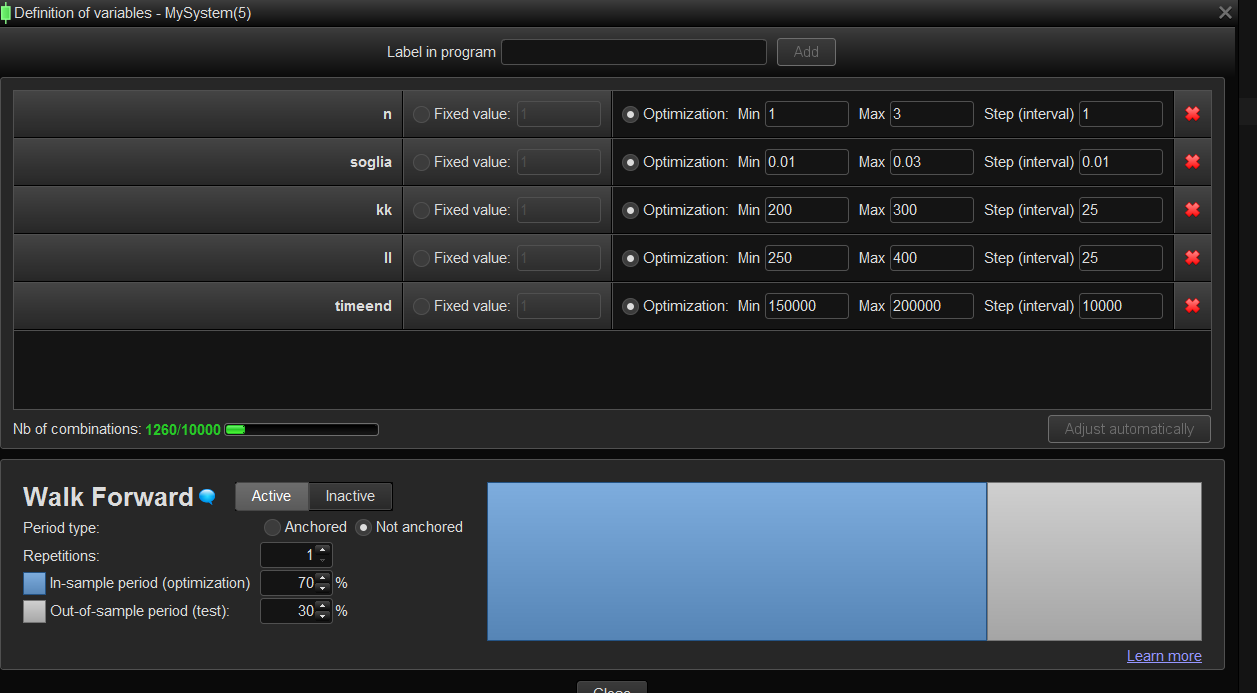

Results attached are from walk forward analysis with 1 OOS period proving robustness of the optimized variables. Variables to be optimized are also described in one of the attached picture.

Discussions about the strategy are running here: Dax Trrend Following, h2 time zone:uk

defparam cumulateorders = false

n=2

soglia = 0.02

timestart = 90000

timeend = 180000

profitti = 275

perdite = 350

timeok = time>=timestart and time<=timeend

c = (sin(atan((close-open[n])/open[n]*100/n)))

if c crosses over soglia and timeok then

buy 1 contract at market

endif

if c crosses under -soglia and timeok then

sellshort 1 contract at market

endif

set target pprofit profitti

set stop ploss perdite

Download

{kind=link}

Filename:

wf_dax_1-1.png

Downloads:

340

Download

Filename:

DAX-trend-following-2h-TF.itf

Downloads:

633

Master

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...