Dax survivor long/short mean reverting/breakout

April 29, 2017, 8:36 AM

Strategies

7 Comments

{kind=link}

Dear all

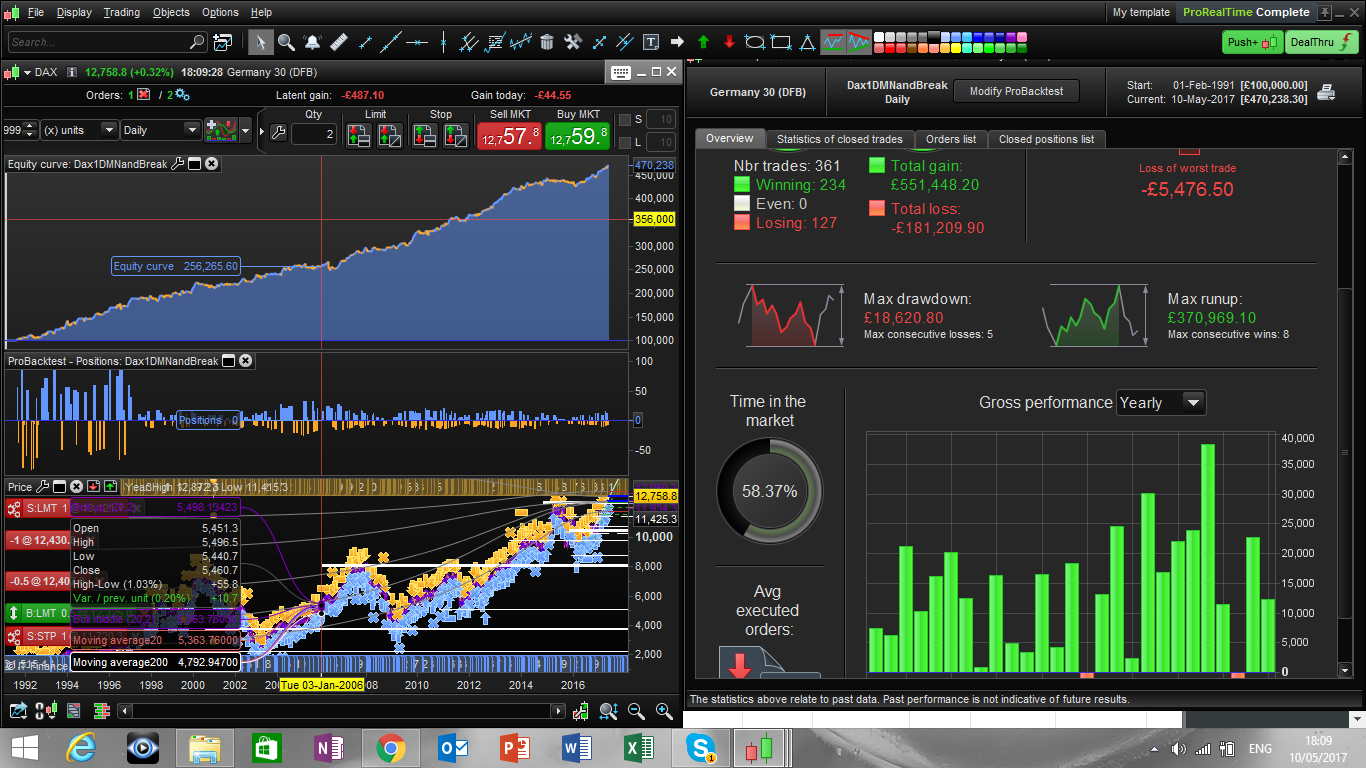

I have tested a slight variation on the them of my previously described strategy on short TF.

This time I took a very long timeseries, used Daily timeframe and modified the exit strategy in term of number of bars, all is optimized with Reiner’s seasonal parameters

Although the return of 180% with a drawdown of ~20k on a such a long timeseries is not great, I though it was worth posting because of the ability of this strategy to survive all the 1998/2001/2008 shocks and because it’s relative smoothness.

Any idea to reduce the drawdown even more would be greatly appreciated.

Best Regards

Francesco

// DAX(mini) - IG MARKETS

// TIME FRAME 1Day

// SPREAD 1.0 Point

DEFPARAM CumulateOrders = False

//DEFPARAM FLATBEFORE =090000

//DEFPARAM FLATAFTER =210000

golong = 1

goshort = 1

exitafternbars =1 // the strategy has an exit strategy of the type n bars

// variables optimized

adxvallong = 36 // set the adx value for long position under which the strategy is mean reverting and above which the strategy is breakout

atrmaxlong = 100//set the max vol accetable for long position

adxvalshort = 24// set the adx value for short poistions under which the strategy is mean reverting and above which the strategy is breakout

atrmaxshort = 200//set the max vol acceptable for short positions

along= 30//number of cons bar for a long trade

mlong = 1// sets the atr multiplier to enter into a mean reverting strategy for long positions

nlong = 1//sets the atr multiplier to enter into a breakout strategy for long positions

ashort=5//number of cons bars for a short trade

mshort = 1//sets the atr multiplier to enter into a mean reverting strategy for short positions

nshort = 2//sets the atr multiplier to enter into a breakout strategy for short positions

//

vollongok = atr<atrmaxlong

volshortok = atr<atrmaxshort

brekoutlong = marketregimeindicator>adxvallong

meanreversionlong = marketregimeindicator <adxvallong

brekoutshort = marketregimeindicator>adxvalshort

meanreversionshort = marketregimeindicator<adxvalshort

adxperiod = 14

atrperiod = 14

marketregimeindicator = adx[adxperiod]

atr = AverageTrueRange[atrperiod]

positionshort = round(1000/atr) //define the size of short positions

positionlong = saisonalpatternmultiplier*round(1000/atr/2.16666) // define the size of long positions

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 0 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 0 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

endif

//long meanreversion

IF (abs(open-close) > (atr*mlong) and close < open and golong and vollongok and meanreversionlong) THEN

buy positionlong CONTRACTS AT MARKET

ENDIF

// long breakout

IF (abs(open-close) > (atr*nlong) and close > open and golong and vollongok and brekoutlong) THEN

buy positionlong CONTRACTS AT MARKET

ENDIF

//short meanrevesrion

IF (abs(open-close) > (atr*mshort) and close > open and goshort and volshortok and meanreversionshort) THEN

sellshort positionshort CONTRACTS AT MARKET

ENDIF

// short

IF (abs(open-close) > (atr*nshort) and close < open and goshort and volshortok and brekoutshort) THEN

sellshort positionshort CONTRACTS AT MARKET

ENDIF

if exitafternbars then

IF shortonmarket and BarIndex - TradeIndex >= ashort Then

exitshort positionshort contracts at Market

EndIF

endif

if exitafternbars then

IF longonmarket and BarIndex - TradeIndex >= along Then

sell positionlong contracts at Market

EndIF

endif

//set target profit p*atr

//set stop ploss l*atr

Download

Filename:

Dax1Dsurvivor_v2.itf

Downloads:

317

Download

{kind=link}

Filename:

daxsurvivor_2.png

Downloads:

237

Download

Filename:

Dax1DMNandBreak.itf

Downloads:

318

Download

{kind=link}

Filename:

statdax1d.png

Downloads:

185

Master

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...