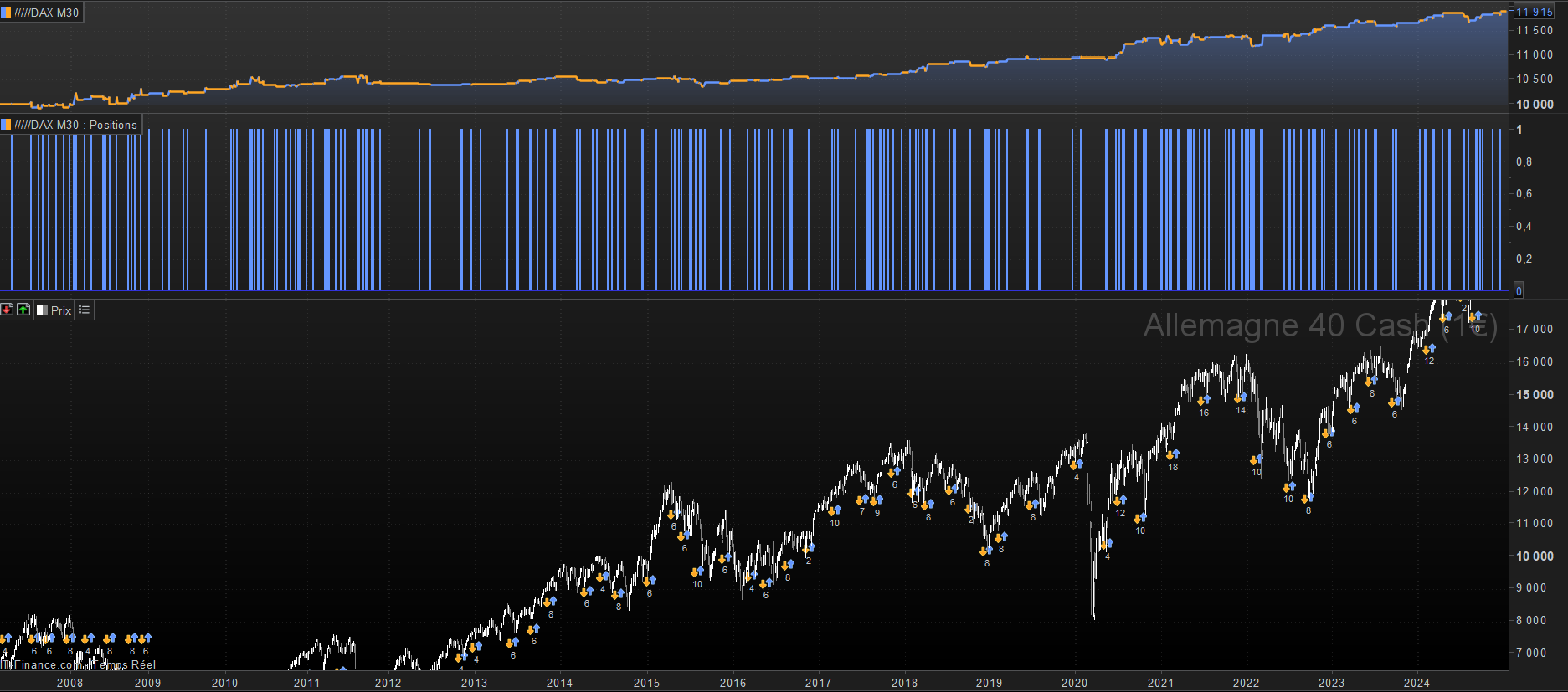

Dax Reversal Catcher M30

{kind=link}

Hi everyone,

I’m sharing this strategy I’ve been working on recently. It’s a mean reversion setup designed for the DAX working on M30 (with proper optimization it gives algo great results on the Nasdaq). The strategy targets reversals using a combination of indicators:

– Bollinger Bands for volatility and price extremes

– VWAP for intraday price reference

– EMAs for trend direction

– Higher Highs pattern confirmation

The strategy looks for oversold conditions near the lower Bollinger Band, waiting for a VWAP breakout to confirm the reversal. It includes automatic position closure before US market open.

While testing this strategy, I noticed the trade frequency is lower than expected. Although the logic behind seems to be great, I believe there’s room for improvement. Rather than keeping it to myself, I decided to share it as it could serve as a good foundation for further development for those who are interested in dedicating some time.

Potential areas for enhancement:

– Fine-tuning the BB parameters

– Adding volume filters

– Implementing more sophisticated exit rules

Feel free to modify and build upon this base (and share the final result if you want).

P.S: As always, please backtest thoroughly before using with real money.

//——————————————//

// Reversal Catcher — Thibauld Robin — FOR DAX M30

//——————————————//

// Initialization

ONCE pos = 0

BBlength = 20

BBmult = 1.5

fastEMA = 21

slowEMA = 50

rsiLength = 14

overbought = 70

oversold = 30

// Bollinger Bands

bbMA = AVERAGE[BBlength](close)

bbDev = SQRT(SUMMATION[BBlength]((close – bbMA)*(close – bbMA))/BBlength)

BBupper = bbMA + (bbDev * BBmult)

BBlower = bbMA – (bbDev * BBmult)

// EMAs

ema21 = TEMA[21](close)

ema50 = TEMA[50](close)

// VWAP

IF day<>day[1] THEN

d=1

VWAP=typicalprice

ELSE

d=d+1

IF volume > 0 THEN

VWAP = SUMMATION[d](volume*typicalprice)/SUMMATION[d](volume)

ENDIF

ENDIF

// Trend

upTrend = ema21 > ema50

// HH/LL

hhLLong = low > low[1] AND high > high[1] AND close > high[1]

// Entries

vwapBreakout = close crosses over VWAP

longCond = Low[1] < BBlower[1] AND close > BBlower AND close < BBupper AND hhLLong AND upTrend AND vwapBreakout

// Exits

exitLong = (close > BBupper) OR (ema21 crosses under ema50)

// Trading Orders

IF longCond AND pos = 0 THEN

BUY 1 SHARES AT MARKET

pos = 1

SET STOP LOSS low[1]

ENDIF

// Exits

IF pos = 1 AND exitLong THEN

SELL AT MARKET

pos = 0

ENDIF

// Close before US open

IF TIME >= 150000 AND pos <> 0 THEN

IF pos = 1 THEN

SELL AT MARKET

ENDIF

pos = 0

ENDIF