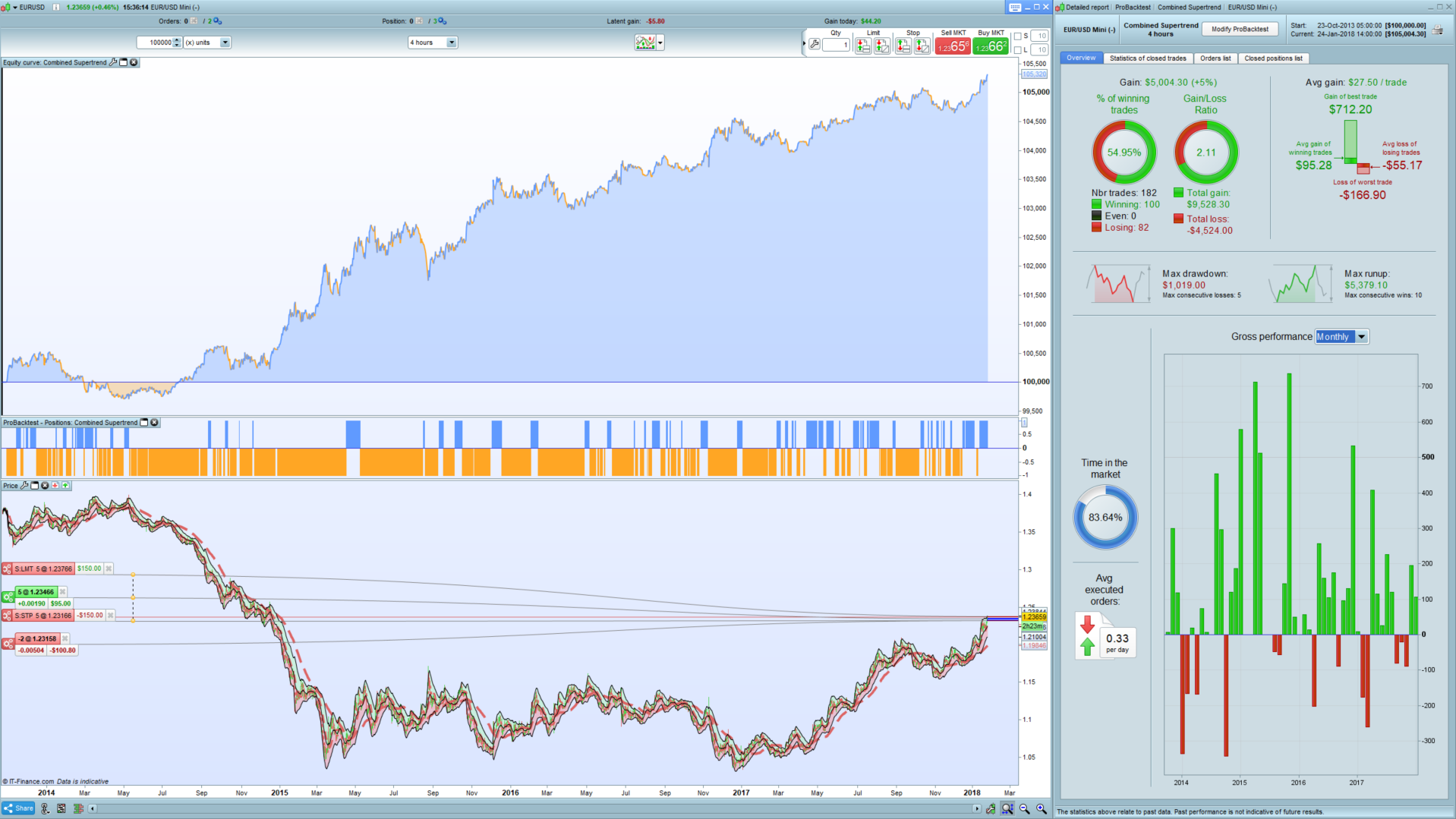

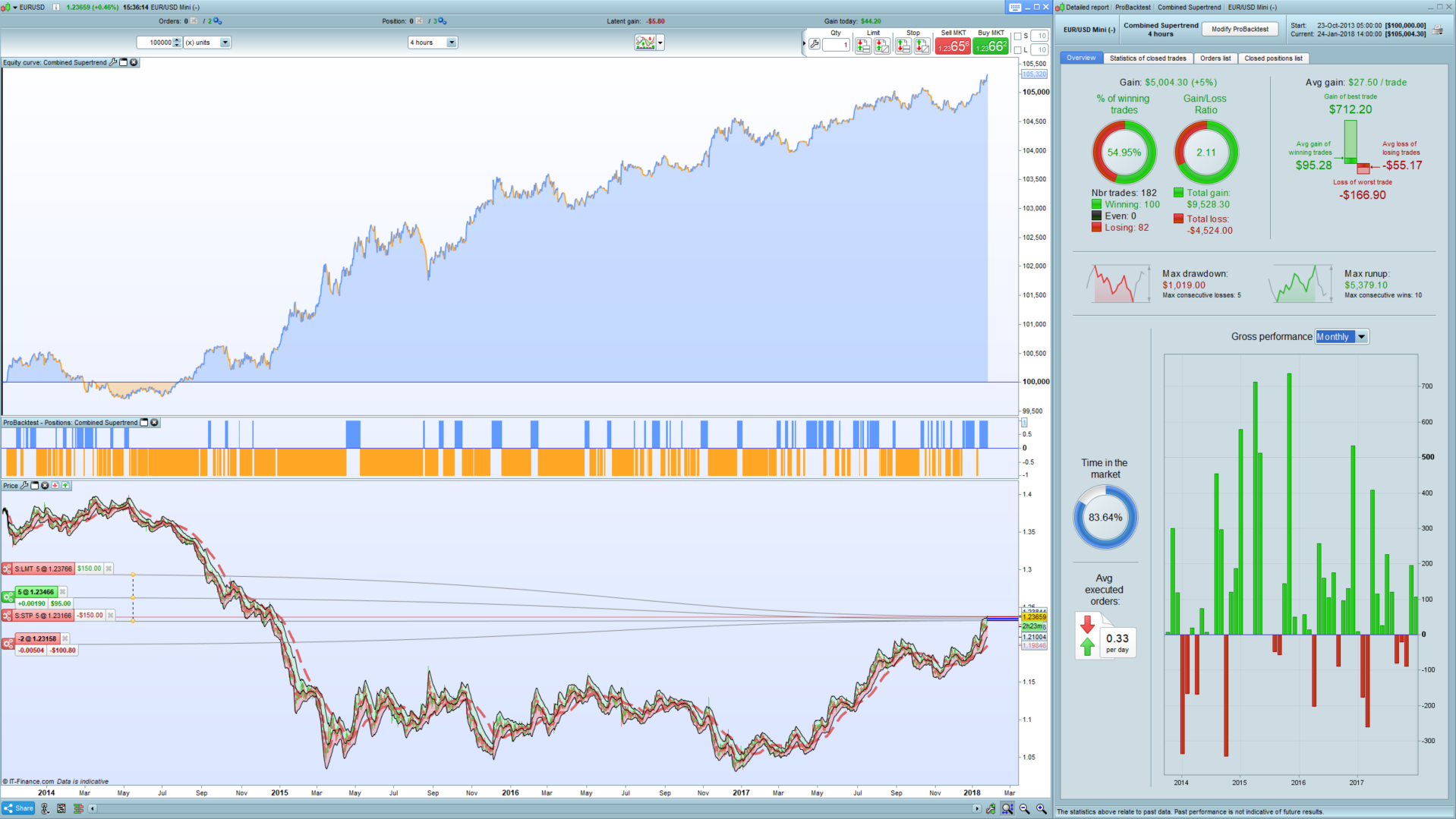

Combined Supertrend EURUSD 4Hr

January 24, 2018, 5:35 PM

Strategies

7 Comments

{kind=link}

Here is a 4Hr EURUSD strategy where I decided to combine 4 different supertrend indicators to filter out weaker trends.

The parameters are mostly standard (as originally found) with the exception of a variable named ‘margin’ that defines the minimum distance between two of the specific trend lines.

Defparam cumulateorders = false

possize = 1

//////////////////////////////////////////////////////////////

//Andrew Abraham Trend Trader

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Length = 21

Multiplier = 3

avrTR = weightedaverage[Length](AverageTrueRange[1](close))

highestC = highest[Length](high)

lowestC = lowest[Length](low)

hiLimit = highestC[1]-(avrTR[1]*Multiplier)

lolimit = lowestC[1]+(avrTR[1]*Multiplier)

if(close > hiLimit AND close > loLimit) THEN

ret = hiLimit

ELSIF (close < loLimit AND close < hiLimit) THEN

ret = loLimit

ELSE

ret = ret[1]

ENDIF

/////////////////////////////////////////////////////////////

//Simplified supertrend (without volatility component ATR)

//Posted by @verdi55 in PRC Library

/////////////////////////////////////////////////////////////

ONCE direction = 1

ONCE STlongold = 0

ONCE STshortold = 1000000000000

factor = 0.005

indicator1 = medianprice

indicator3 = close

indicator2 = indicator3 * factor

STlong = indicator1 - indicator2

STshort = indicator1 + indicator2

If direction = 1 and STlong < STlongold then

STlong = STlongold

endif

If direction = -1 and STshort > STshortold then

STshort = STshortold

endif

If direction = 1 and indicator3 < STlong then

direction = -1

endif

If direction = -1 and indicator3 > STshort then

direction = 1

endif

STlongold = STlong

STshortold = STshort

If direction = 1 then

ST = STlong

else

ST = STshort

endif

/////////////////////////////////////////////////////////////

//PRC_adaptive SuperTrend (r-square method) | indicator

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Period = 10

mult = 2

Data = customclose

SumX = 0

SumXX = 0

SumXY = 0

SumYY = 0

SumY = 0

if barindex>Period then

// adaptive r-squared periods

for k=0 to period-1 do

tprice = Data[k]

SumX = SumX+(k+1)

SumXX = SumXX+((k+1)*(k+1))

SumXY = SumXY+((k+1)*tprice)

SumYY = SumYY+(tprice*tprice)

SumY = SumY+tprice

next

Q1 = SumXY - SumX*SumY/period

Q2 = SumXX - SumX*SumX/period

Q3 = SumYY - SumY*SumY/period

iRsq=((Q1*Q1)/(Q2*Q3))

avg = supertrend[mult,round(Period+Period*(iRsq-0.25))]

EndIf

//////////////////////////////////////////////////////////////////

OriginalST = Supertrend[3,5]

/////////////////////////////////////////////////////////////////

margin = 7*pointsize

If countofposition = 0 and abs(ret[1]-ST[1]) > margin and abs(ret-ST) > margin Then

If close > ret and close > ST and close > avg Then

Buy possize contract at market

ElsIf close < ret and close < ST and close < avg Then

Sellshort possize contract at market

EndIf

ElsIf longonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close < ret and close < ST and close < avg and close < OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] < avg[1] and close[1] < OriginalST[1]))) Then

Sell at market

ElsIf shortonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close > ret and close > ST and close > avg and close > OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] > avg[1] and close[1] < OriginalST[1]))) Then

Exitshort at market

EndIf

Download

Filename:

Combined-Supertrend.itf

Downloads:

673

Download

{kind=link}

Filename:

CombinedSupertrend.png

Downloads:

292

Master

My name is Juan Jacobs and I am an algorithmic trader and trading coach. After 7 years of corporate work as a Systems Analyst, I have decided to pursue my passion of trading on a full-time basis. My current focus area is that of 'smart' strategies based on 'Machine Learning'. You can find me at www.FXautomate.com or visit my PRC Marketplace Store here: https://market.prorealcode.com/store/fxautomate/

Author’s Profile

Loading...