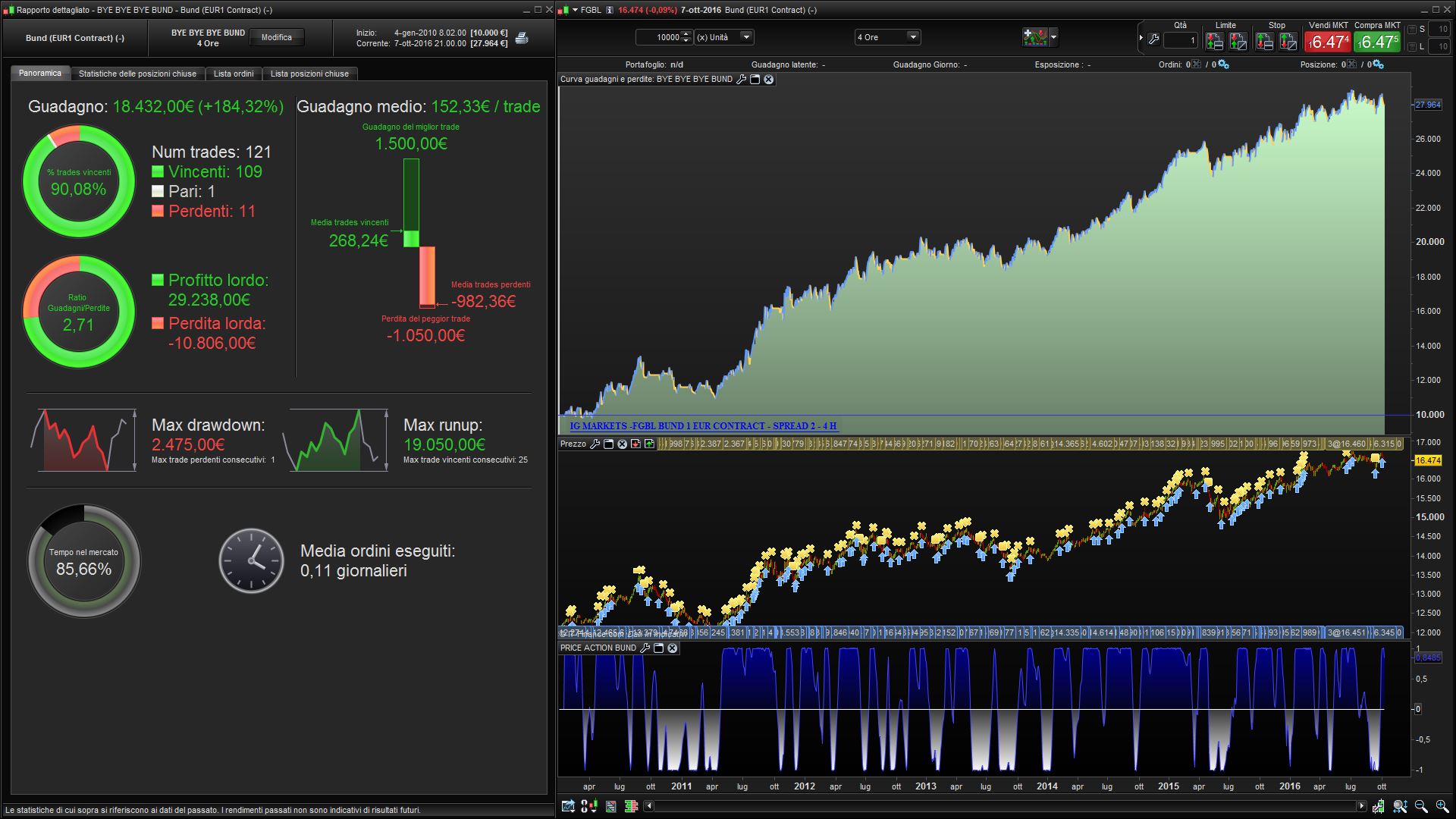

Bund CFD Strategy - 4 h

October 10, 2016, 9:47 AM

Strategies

8 Comments

Long only strategy for the BUND (1 eur per contract) on a 4 hours timeframe. Backtest with 2 points spread from mid-2010 to now.

Signals are taken from a super smoothed filter (indicator “PRICE ACTION BUND”). Profit are trailed with a soft coded trailing stop in the strategy.

//--------------------------------------------------------------------------------

// STRATEGY BYE BYE BYE BUND

// IG MARKET - FGBL BUND 1 EUR - 4 H - SPREAD 2

DEFPARAM CumulateOrders = false

PositionSize = 1

indicator1, ignored = CALL "PRICE ACTION BUND"

c1 = (indicator1 >= 1)

indicator1, ignored = CALL "PRICE ACTION BUND"

c2 = (indicator1 <=- 1)

indicator1, ignored = CALL "PRICE ACTION BUND"

c3 = (indicator1 crosses over 0)

IF c1 or c2 or c3 AND CurrentDayOfWeek <> 1 THEN

BUY POSITIONSIZE CONTRACT AT MARKET

ENDIF

// TRAILING STOP LOGIK BY KENNETH KVISTAD MODIFIED FOR LONG AND SHORT POSITION

TGL =66

if not onmarket then

MAXPRICE = 0

EXITPRICE = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

EXITPRICE = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if onmarket and EXITPRICE>0 then

SELL AT EXITPRICE STOP

ENDIF

SET STOP PLOSS 350

SET TARGET PPROFIT 500

Indicator needed to run the strategy (“PRICE ACTION BUND”)

// UNIVERSAL CODE POSTED BY NICOLAS

// INDICATOR PRICE ACTION BUND

bandedge=50

whitenoise= (Close - Close[50])

if barindex>bandedge then

// super smoother filter

a1= Exp(-1.414 * 3.14159 / bandedge)

b1= 2*a1 * Cos(1.414*180 /bandedge)

c2= b1

c3= -a1 * a1

c1= 1 - c2 - c3

filt= c1 * (whitenoise + whitenoise[1])/2+ c2*filt[1] + c3*filt[1]

filt1 = filt

if ABS(filt1)>pk[1] then

pk = ABS(filt1)

else

pk = 0.99* pk[1]

endif

if pk=0 then

denom = -1

else

denom = pk

endif

if denom = -1 then

result = result[1]

else

result = filt1/pk

endif

endif

RETURN result COLOURED(66,66,205) as "PRICE ACTION", 0 as "0"

Download

Filename:

PRICE-ACTION-BUND.itf

Downloads:

274

Download

Filename:

BYE-BYE-BYE-BUND-TS.itf

Downloads:

264

Download

{kind=link}

Filename:

BYE-BYE-BYE-BUND.jpg

Downloads:

222

Master

My name is Alessandro, i'm a trader since 2006

You can find me on my website: <a href="http://www.automatictrading.it/" rel="dofollow">www.automatictrading.it</a>

<strong>(trading programming services Italy)</strong>

Italy

Author’s Profile

Loading...