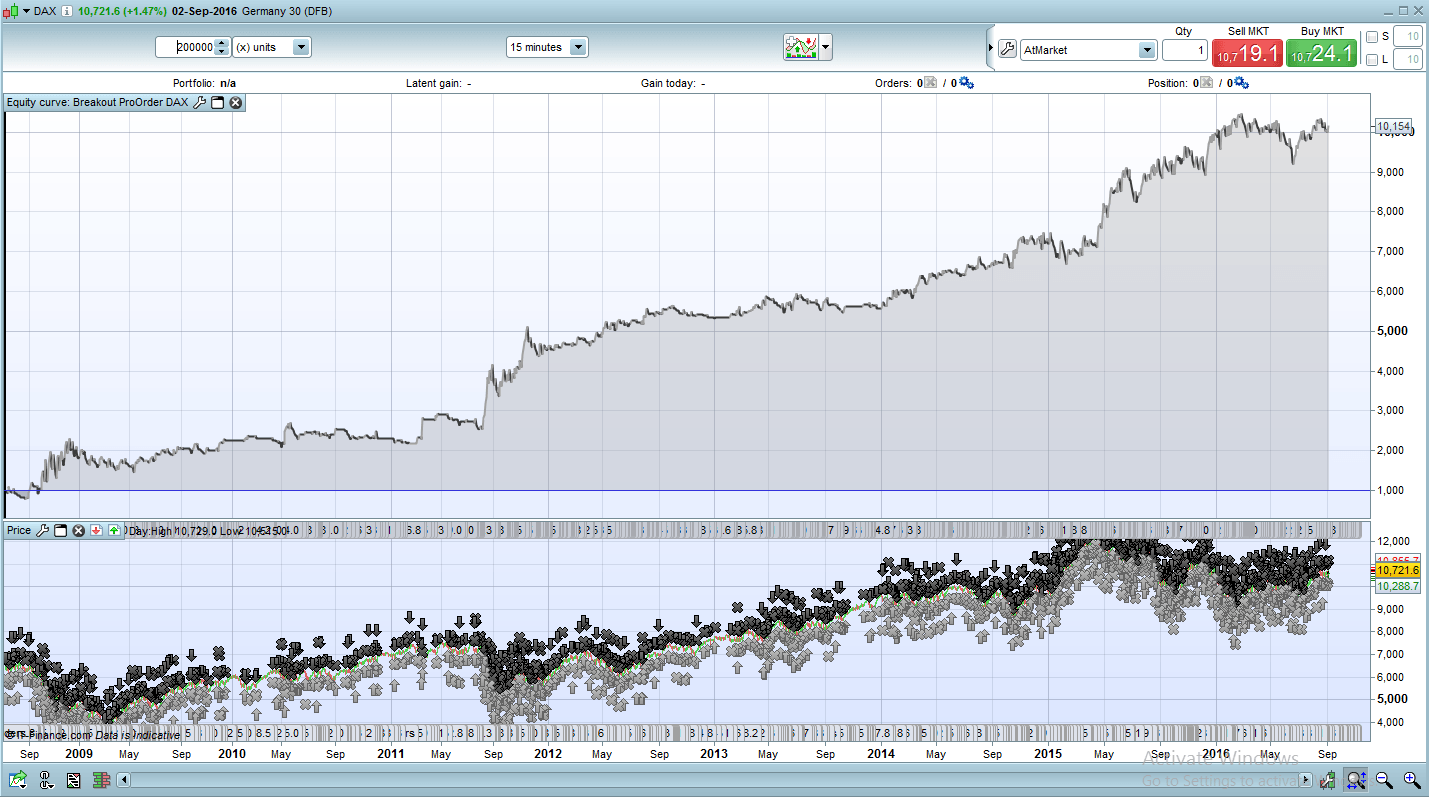

Breakout DAX 15Min

{kind=link}

Firstly, a big thank you to Nicolas for this great site and for originally introducing us to the CAC Breakout using the same code here.

I set about testing this strategy on other markets due to the fact you can backtest 8 years of data with 200,000 units on the 15Min time-frame. The other massive plus is no fake profits and only 26, 0 bars in 1500 trades! 🙂

In this version I am using a fixed position size but you can activate the re-invest system if you are happy with that. It makes for an interesting ride!

I stuck to the rules of not over optimising/curve fitting by using an IN/OUT sample as documented here. This ran from July 2008 – Jan 2014.

The results above are £1 Per Point, £1000 Start and 1.5 Spread.

I am live trading this with real money with minimum stakes to test. IG have now reduced the PPP from £2 to £1 just recently. This is very handy for forward live testing.

All times in the code are UK so please adjust to your timezone.

I have some more of these ported to other markets but need to spend a little more time getting them right before posting in the library. Expect them soon.

I have not had enough time to test different time frames. Maybe I will try that next if time allows.

Good luck and enjoy your weekend.

//-------------------------------------------------------------------------

// Main code : Breakout ProOrder EN DAX

//-------------------------------------------------------------------------

// We do not store data until the system starts.

// If it is the first day that the system is launched and if it is afternoon,

// it will wait until the next day for defining sell and buy orders.

//All times are UK Time Zone

DEFPARAM PreLoadBars = 0

// Position is closed at 20h00 PM

DEFPARAM FlatAfter = 200000

// No new position will be initiated after the 16:00PM candlestick. Any existing orders cancelled at 16:30pm

LimitHour = 161500

// Market scan begin with the 15 minute candlestick that closed at 8:30AM

StartHour = 081500

// The 24th-31st days of December will not be traded because the market closes early.

IF (Month = 5 AND Day = 1) OR (Month = 12 AND (Day = 24 OR Day = 25 OR Day = 26 OR Day = 30 OR Day = 31)) THEN

TradingDay = 0

ELSE

TradingDay = 1

ENDIF

// Variables that would be adapted to your preferences

if time = 074500 then

//PositionSize = max(1,1+ROUND((strategyprofit-1000)/1000)) //gain re-invest trade volume

PositionSize = 1 //constant trade volume over the time

endif

MaxAmplitude = 170

MinAmplitude = 22

OrderDistance = 9

PourcentageMin = 19

// Variable initilization once at system start

ONCE StartTradingDay = -1

// Variables that can change in intraday are initiliazed

// at first bar on each new day

IF (Time <= StartHour AND StartTradingDay <> 0) OR IntradayBarIndex = 0 THEN

BuyTreshold = 0

SellTreshold = 0

BuyPosition = 0

SellPosition = 0

StartTradingDay = 0

ELSIF Time >= StartHour AND StartTradingDay = 0 AND TradingDay = 1 THEN

// We store the first trading day bar index

DayStartIndex = IntradayBarIndex

StartTradingDay = 1

ELSIF StartTradingDay = 1 AND Time <= LimitHour THEN

// For each trading day, we define each 15 minutes

// the higher and lower price value of the instrument since StartHour

// until the buy and sell tresholds are not defined

IF BuyTreshold = 0 OR SellTreshold = 0 THEN

HighLevel = Highest[IntradayBarIndex - DayStartIndex + 1](High)

LowLevel = Lowest [IntradayBarIndex - DayStartIndex + 1](Low)

// Spread calculation between the higher and the

// lower value of the instrument since StartHour

DaySpread = HighLevel - LowLevel

// Minimal spread calculation allowed to consider a significant price breakout

// of the higher and lower value

MinSpread = DaySpread * PourcentageMin / 100

// Buy and sell tresholds for the actual if conditions are met

IF DaySpread <= MaxAmplitude THEN

IF SellTreshold = 0 AND (Close - LowLevel) >= MinSpread THEN

SellTreshold = LowLevel + OrderDistance

ENDIF

IF BuyTreshold = 0 AND (HighLevel - Close) >= MinSpread THEN

BuyTreshold = HighLevel - OrderDistance

ENDIF

ENDIF

ENDIF

// Creation of the buy and sell orders for the day

// if the conditions are met

IF SellTreshold > 0 AND BuyTreshold > 0 AND (BuyTreshold - SellTreshold) >= MinAmplitude THEN

IF BuyPosition = 0 THEN

IF LongOnMarket THEN

BuyPosition = 1

ELSE

BUY PositionSize CONTRACT AT BuyTreshold STOP

ENDIF

ENDIF

IF SellPosition = 0 THEN

IF ShortOnMarket THEN

SellPosition = 1

ELSE

SELLSHORT PositionSize CONTRACT AT SellTreshold STOP

ENDIF

ENDIF

ENDIF

ENDIF

// Conditions definitions to exit market when a buy or sell order is already launched

IF LongOnMarket AND ((Time <= LimitHour AND SellPosition = 1) OR Time > LimitHour) THEN

SELL AT SellTreshold STOP

ELSIF ShortOnMarket AND ((Time <= LimitHour AND BuyPosition = 1) OR Time > LimitHour) THEN

EXITSHORT AT BuyTreshold STOP

ENDIF

// Maximal risk definition of loss per position

// in case of bad evolution of the instrument price

SET STOP PLOSS MaxAmplitude

//SET TARGET PPROFIT 190