Blue Monday DAX

May 22, 2016, 11:58 AM

Strategies

19 Comments

{kind=link}

Hi guys,

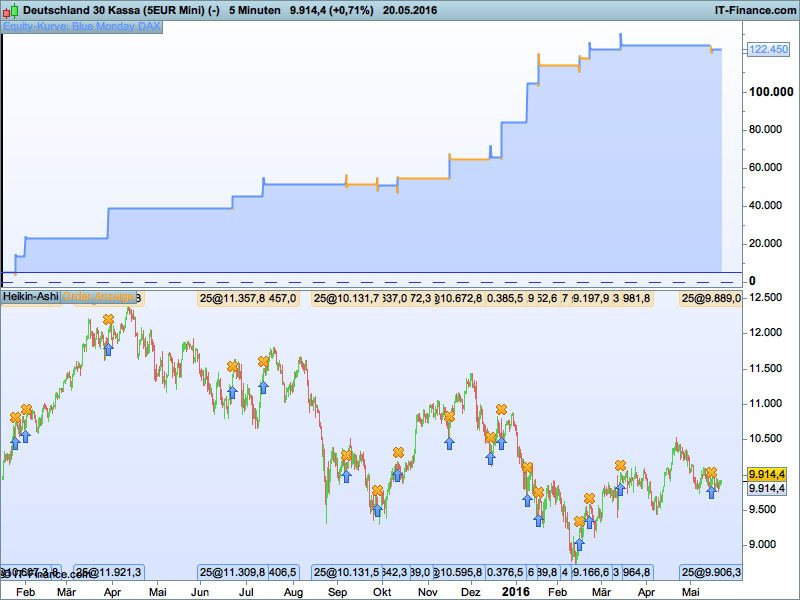

here is another DAX trading idea. It is very simple and generates only few trades but it seems very profitable if it happens.

Have fun

Reiner

// Blue Monday DAX

// Code-Parameter

DEFPARAM FlatAfter = 095500

// trading window

ONCE BuyTime = 85500

ONCE SellTime = 95500

ONCE CloseDiff = 50

ONCE PositionSize = 25

ONCE sl = 50

// Long all in, if it's Monday and the market is 50 points higher

IF Not LongOnMarket AND Time = BuyTime AND (CurrentDayOfWeek = 1) THEN

Diff = close - DClose(1)

IF Diff > CloseDiff THEN

BUY PositionSize CONTRACT AT MARKET

ENDIF

ENDIF

// exit position

IF LongOnMarket AND Time = SellTime THEN

SELL AT MARKET

ENDIF

// stop

SET STOP pLOSS sl

Download

Filename:

Blue-Monday-Dax.itf

Downloads:

413

Veteran

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...