Big Three Trading Strategy

November 14, 2017, 5:04 PM

Strategies

3 Comments

{kind=link}

I found this strategy description on the web and use my limited knowledge translate to PRT robot, please kindly try, comment and feel free modify to fit for your need.

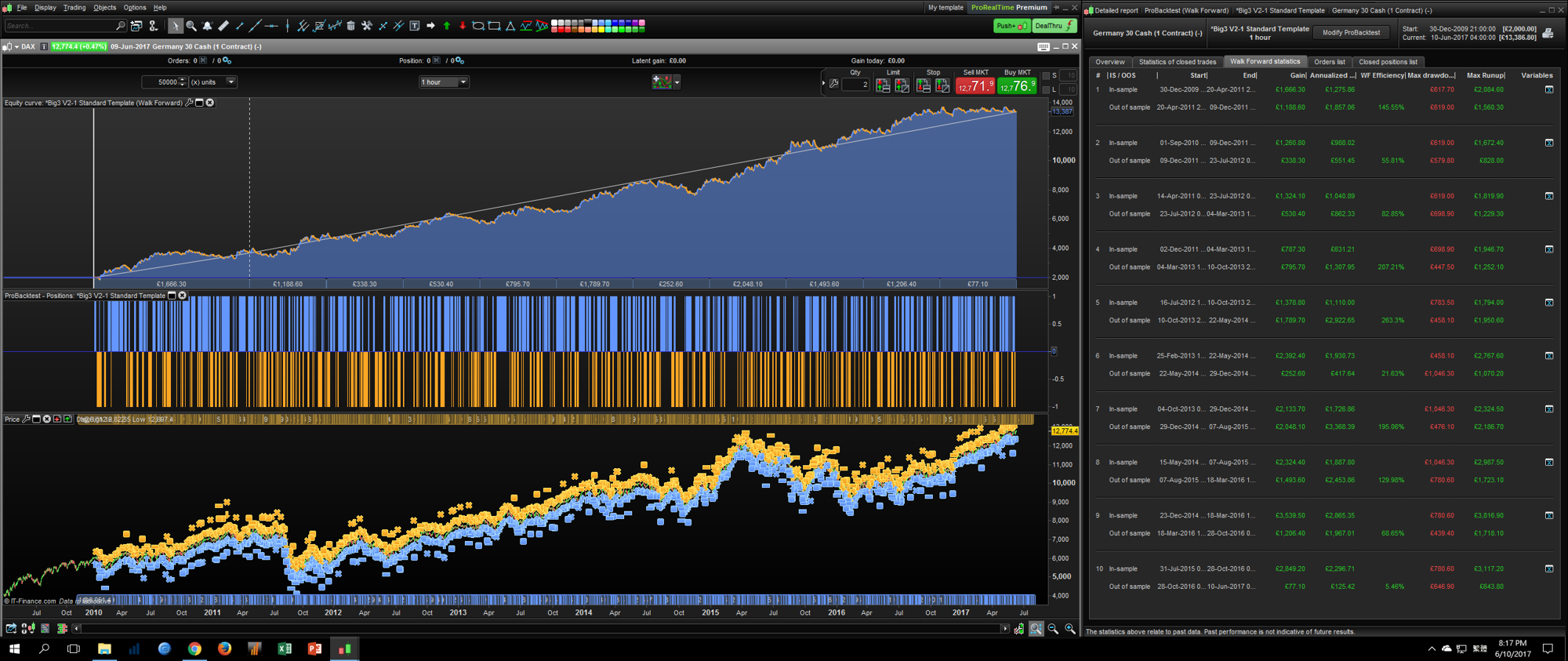

It is mainly composed of trading criteria based upon a set of 3 moving averages, breakout of recent highest high or lowest low and on a candlesticks pattern.

Settings are optimized (please read the code to find what are the optimized variables). A Walk Forward analysis is attached.

The code also embed:

- a money management position sizing

- a trailing stop based on Max Favorable Excursion (MFE trailing stop)

// Big Three Trading Strategy

// Original Idea from: http://www.tradingstrategyguides.com/big-three-trading-strategy/

// Market: DAX 30

// Time Frame: 1 Hour

// Time Zone: Any

// Spread: 2.9

// Version : 2.8

// Revised on 2017-11-14

Defparam preloadbars = 3000

Defparam cumulateorders =false //true //false

//// Optional Function Switch ( 1 = Enable 0 = Disable ) ////

FixedMinMaxStopLoss = 1 // Optional Function 1

TargetProfit = 1 // Optional Function 2

TimeExit = 1 // Optional Function 3

MFETrailing = 1 // Optional Function 4

MoneyManagement = 0 // Optional Function 5

//// Core Indicator Parameter Setting ////

// Moving Average Setting (Original: 20, 40, 80)

Fast = 20 // Not Optimize

Medium = 40 // Not Optimize

Slow = 80 // Not Optimize

// Look Back Bar (Original: N/A)

CP = 3 // Variables Optimized

//// Optional Function ////

// 1) Fixed Min Max Stop Loss Setting

If FixedMinMaxStopLoss then

//Long

MaxLong = 80 // by points, Variables Optimized

MinLong = 30 // by points, Variables Optimized

//Short

MaxShort = 60 // by points, Variables Optimized

MinShort = 5 // by points, Variables Optimized

Endif

// 2) Take Profit Setting

If TargetProfit then

//Long

TakeProfitLongRate = 2.6 // by %, Variables Optimized

//Short

TakeProfitShortRate = 2.5 // by %, Variables Optimized

Endif

// 3) Time Exit Setting

If TimeExit then

//Long

ONCE maxCandlesLongWithProfit = 78 // by bar, Variables Optimized

ONCE maxCandlesLongWithoutProfit = 66 // by bar, Variables Optimized

//Short

ONCE maxCandlesShortWithProfit = 60 // by bar, Variables Optimized

ONCE maxCandlesShortWithoutProfit = 54 // by bar, Variables Optimized

Endif

// 4) MFE Step Setting

If MFETrailing then

//Long

MFELongStep = 1.5 // by %, Variables Optimized

//Short

MFEShortStep = 1 // by %, Variables Optimized

Endif

// 5) Money Management

If MoneyManagement then

LongRisk = 5 // by %, Variables Optimized

ShortRisk = 3 // by %, Variables Optimized

CloseBalanceMaxDrop = 50 // by %, Personal preference

Capital = 3000 // by $

Equity = Capital + StrategyProfit

LongMaxRisk = Round(Equity*LongRisk/100)

ShortMaxRisk = Round(Equity*ShortRisk/100)

//Max Contract

MaxLongContract = 500 // by contract, Variables Optimized

MaxShortContract = 100 // by contract, Variables Optimized

//Check system account balance

If equity<QuitLevel then

Quit

Endif

RecordHighest = MAX(RecordHighest,Equity)

QuitLevel = RecordHighest*((100-CloseBalanceMaxDrop)/100)

Endif

// Core indicator

//Big Three MA

FMA = Average[Fast](close) //green coloured(0,255,0)

MMA = Average[Medium](close) //blue coloured(0,0,255)

SMA = Average[Slow](close) //red coloured(255,0,0)

// Entry Rules

//Buy Signal

B1 = low > SMA and low>MMA and low>FMA

B2 = high >= highest[CP](high)

BC = B1 and B2

//Buy Candle

BC1 = Close[1] < Close[2]

BC2 = Close > Close[1]

BC3 = Close > Open

BCandle = BC1 and BC2 and BC3

//Sell Signal

S1 = high < FMA and high<MMA and high<SMA

S2 = low <= lowest[CP](low)

SC = S1 and S2

//Sell Candle

SC1 = Close[1] > Close[2]

SC2 = Close < Close[1]

SC3 = Close < Open

SCandle = SC1 and SC2 and SC3

// Exit Rules

LongExit = Close crosses under SMA

ShortExit = Close crosses over SMA

//Long Entry

If Not LongonMarket and BC and BCandle then

BuyPrice = Close

If FixedMinMaxStopLoss then

StopLossLong = MIN(MaxLong,MAX(MinLong,(BuyPrice - SMA)))

Else

StopLossLong = BuyPrice - SMA

Endif

If TargetProfit then

TakeProfitLong = StopLossLong * TakeProfitLongRate

TP = TakeProfitLong

Endif

SL = StopLossLong

If MoneyManagement then

PositionSizeLong = min(MaxLongContract,(max(2,abs(round((LongMaxRisk/StopLossLong)/PointValue)*pipsize))))

BUY PositionSizeLong CONTRACT AT MARKET

Else

BUY 2 CONTRACT AT MARKET

Endif

Endif

//Long Exit

If LongonMarket and LongExit then

sell at market

Endif

//short entry

If Not ShortonMarket and SC and SCandle then

SellPrice = Close

If FixedMinMaxStopLoss then

StopLossShort = MIN(MaxShort,MAX(MinShort,(SMA - SellPrice)))

Else

StopLossShort = SMA - SellPrice

Endif

If TargetProfit then

TakeProfitShort = StopLossShort * TakeProfitShortRate

TP = TakeProfitShort

Endif

SL = StopLossShort

If MoneyManagement then

PositionSizeShort = min(MaxShortContract,(max(2,abs(round((ShortMaxRisk/StopLossShort)/PointValue)*pipsize))))

SELLSHORT PositionSizeShort CONTRACT AT MARKET

Else

SELLSHORT 2 CONTRACT AT MARKET

Endif

Endif

//Short Exit

If ShortonMarket and ShortExit then

exitshort at market

Endif

// Time Exit

If TimeExit then

If LongonMarket then

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

elsif ShortonMarket then

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

Endif

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

sell at market

endif

IF SHORTONMARKET AND (m2 OR m4) THEN

exitshort at market

endif

Endif

//MFE Trailing stop

If MFETrailing then

MFELong = (TakeProfitLong/MFELongStep)

MFEShort = (TakeProfitShort/MFEShortStep)

If not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

Endif

If longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

If MAXPRICE-tradeprice(1)>=MFELong*pointsize then

priceexit = MAXPRICE-MFELong*pointsize

Endif

Endif

If shortonmarket then

MINPRICE = MIN(MINPRICE,close)

If tradeprice(1)-MINPRICE>=MFEShort*pointsize then

priceexit = MINPRICE+MFEShort*pointsize

Endif

Endif

If onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

Endif

Endif

// Stop Loss a

SET STOP LOSS SL

// Target Profit

If TargetProfit then

SET TARGET PROFIT TP

Endif

//graph BuyPrice

//graph SellPrice

//graph StopLossLong

//graph StopLossShort

Download

{kind=link}

Filename:

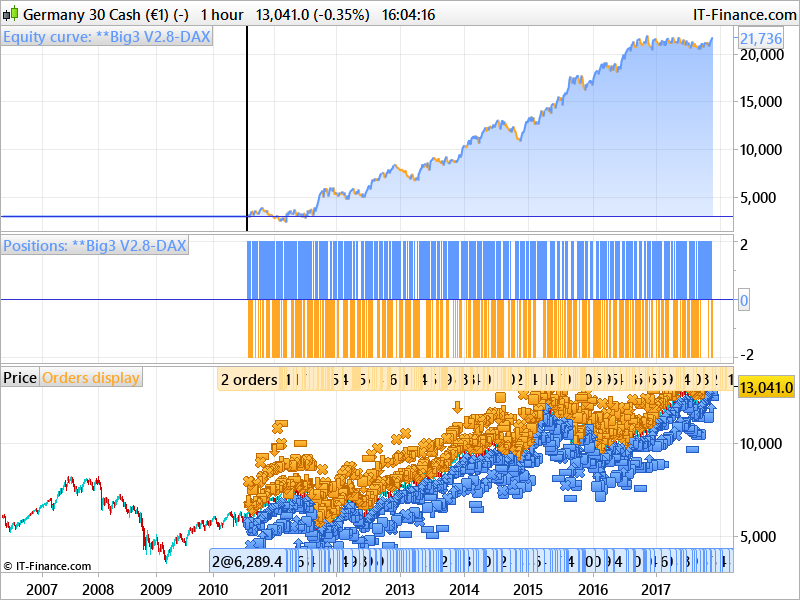

big-threed-trading-strategy-on-DAX.png

Downloads:

793

Download

Filename:

Big3-V2.8-DAX-1.itf

Downloads:

1116

Master

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...