Beating the S&P 500 – Long Term

February 27, 2017, 3:12 PM

Strategies

11 Comments

{kind=link}

Hello!

This is my first submission to the strategy section of this site. My goal is to build filters for market regimes that provide the biases for more short term trading strategies. This submission is a byproduct of my research:

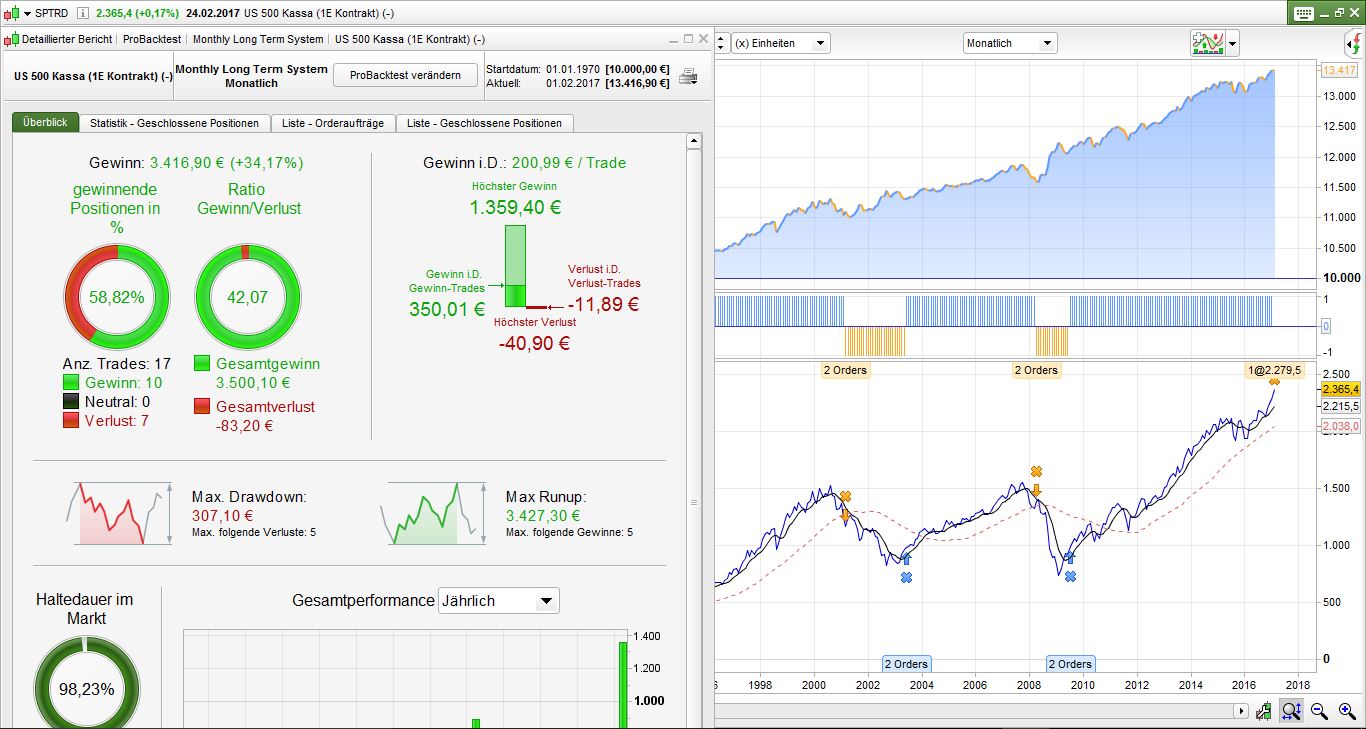

Following is a long term system based on a very simple timing model for capital preservation.

Timeframe is monthly and 2 indicators are used:

- John Ehlers Supersmoother at the standard value of 8.

- A 40 period simple moving average. The SMA has been improved and you can check it is robust to a range of variations.

The system is always on the market. Either long or short.

It doesn’t trade very often and it is not supposed to. The very upside of this model is not the profit but the maximum risk exposure of 13.22%! Maximum drawdown is 2.58 percent!

If you think this is interesting, please critique thoroughly because it will be highly appreciated.

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 40

//John Ehlers’ "Super Smoother", a 2-pole Butterworth filter combined with a 2-bar SMA that suppresses the Nyquist frequency:

Period = 8

Data = Close

PI = 3.14159

f = (1.414*PI) / Period

a = exp(-f)

c2 = 2*a*cos(f)

c3 = -a*a

c1 = 1 - c2 - c3

if barindex>Period then

S = c1*(Data[0]+Data[1])*0.5 + c2*S[1] + c3*S[2]

endif

c1 = (close > S)

c2 = (S > S[1])

IF c1 AND c2 THEN

EXITSHORT 1 CONTRACT AT MARKET

BUY 1 CONTRACT AT MARKET

ENDIF

c3 = (close CROSSES UNDER Average[40](close))

IF c3 THEN

SELL AT MARKET

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

Download

Filename:

Beating-the-SP-500.itf

Downloads:

465

Veteran

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...