An Ichimoku Strategy

{kind=link}

I like the trading concept of Ichimoku. (However the developed Ichimoku Strategy needs to perform better..)

The concept is explained at https://www.investopedia.com/terms/i/ichimoku-cloud.asp

Furthermore I saw some of the learning videos about Ichimoku from Karen Peloille, and an strategy https://www.prorealcode.com/topic/ichimoku-strategy/ on this platform

Searching on the internet I found a strategy fully based upon Ichimoku trading, this has been worked out in the strategy attached.

Distinguished are TenkanSen, KijunSen, Senkou Span A and Senkou Span B

- TenkanSen = (highest[S](high)+lowest[S](low))/2 //Default setting S = 9

- KijunSen = (highest[M](high)+lowest[M](low))/2 // Default setting M = 26

- SenkouSpanA = (Tenkansen[M]+Kijunsen[M])/2 //Default setting M = 26

- SenkouSpanB = (highest[L](High[M])+lowest[L](Low[M]))/2 //Default setting L =52

Trading rules can be described as follows:

Open LONG BUY conditions :

- Tenkan Sen crosses over the Kijun Sen AND

- Close is within 4 periods after the crossing above the Kumo (cloud), defined as Maximum (SenkouSpanA, SenkouSpanB)

Open SHORT SELL conditions :

- Tenkan Sen crosses under the Kijun Sen AND

- lose is within 4 periods after the crossing BELOW the Kumo (cloud), defined as the Minimum (SenkouSpanA, SenkouSpanB)

The exit in for strategy is defined for long positions as when the TenkanSen crosses under the Kijunsen, vice versa for short positions.

I added 2 additional exit methods, below described for long positions, vice versa for short positions:

- Method 2 if the close closes under the upper side of the Kumo / Cloud, based upon the SenkouSpanA

- Method 3 if close closes under the lower side of the Kumo / Cloud, based upon the SenkouSpanB

However:

The default settings 9 for TenkanSen, 26 for KijunSen and 52 for SenkouSpanB do not seen to be profitable.

Therefore I played around with the default settings as well as the exit method.

In the attached ITF file with the strategy, I have left the variables S, M, L and cm (closing method) open as variables.

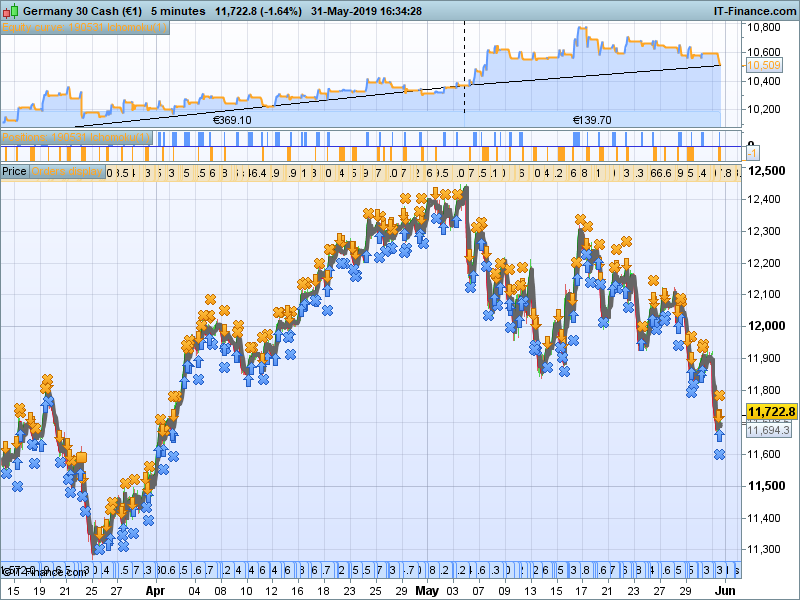

A result is found for the DAX 5 minutes, see also the screenshots, based upon 10.000 bars of the DAX 5 minutes with trading hours from 7:00 AM till 22:00 PM, settings are S =7, M = 14, L = 55 and cm is 1

No good results found so far for other indices and other periods . . . . .

Probably more robust trading strategies are out there . . , hopefully it assists into further developing of good Ichimoku trading strategies.

Comments are more than welcome.

Please download the attached ITF file to get the strategy and its variables to be optimized.

{kind=link}

{kind=link}