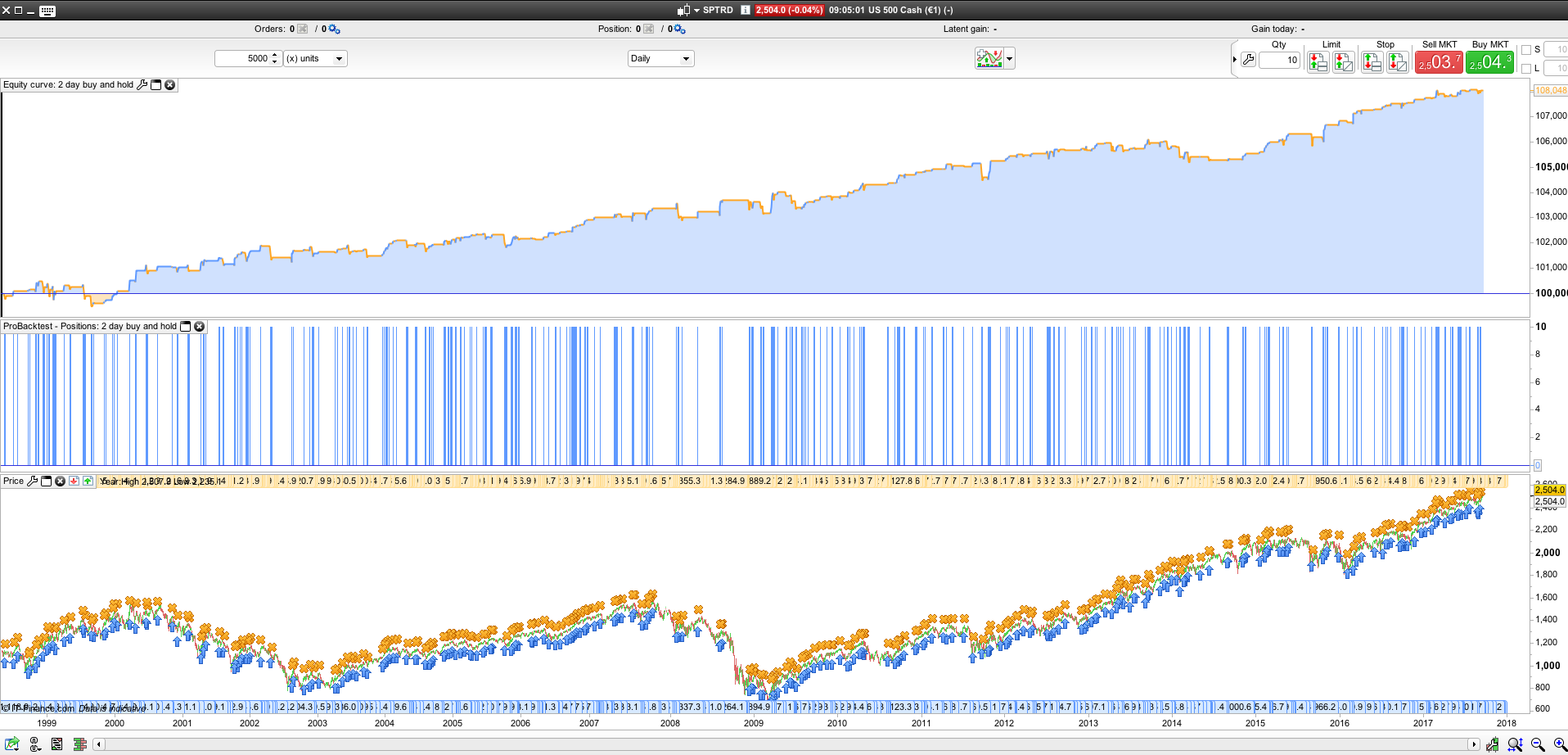

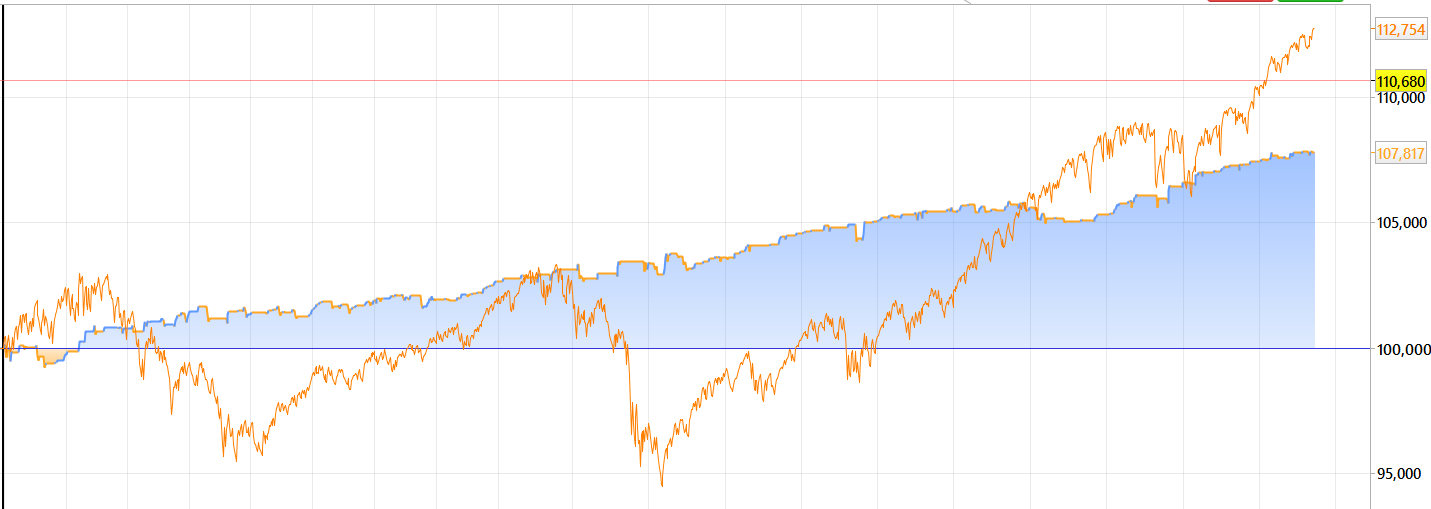

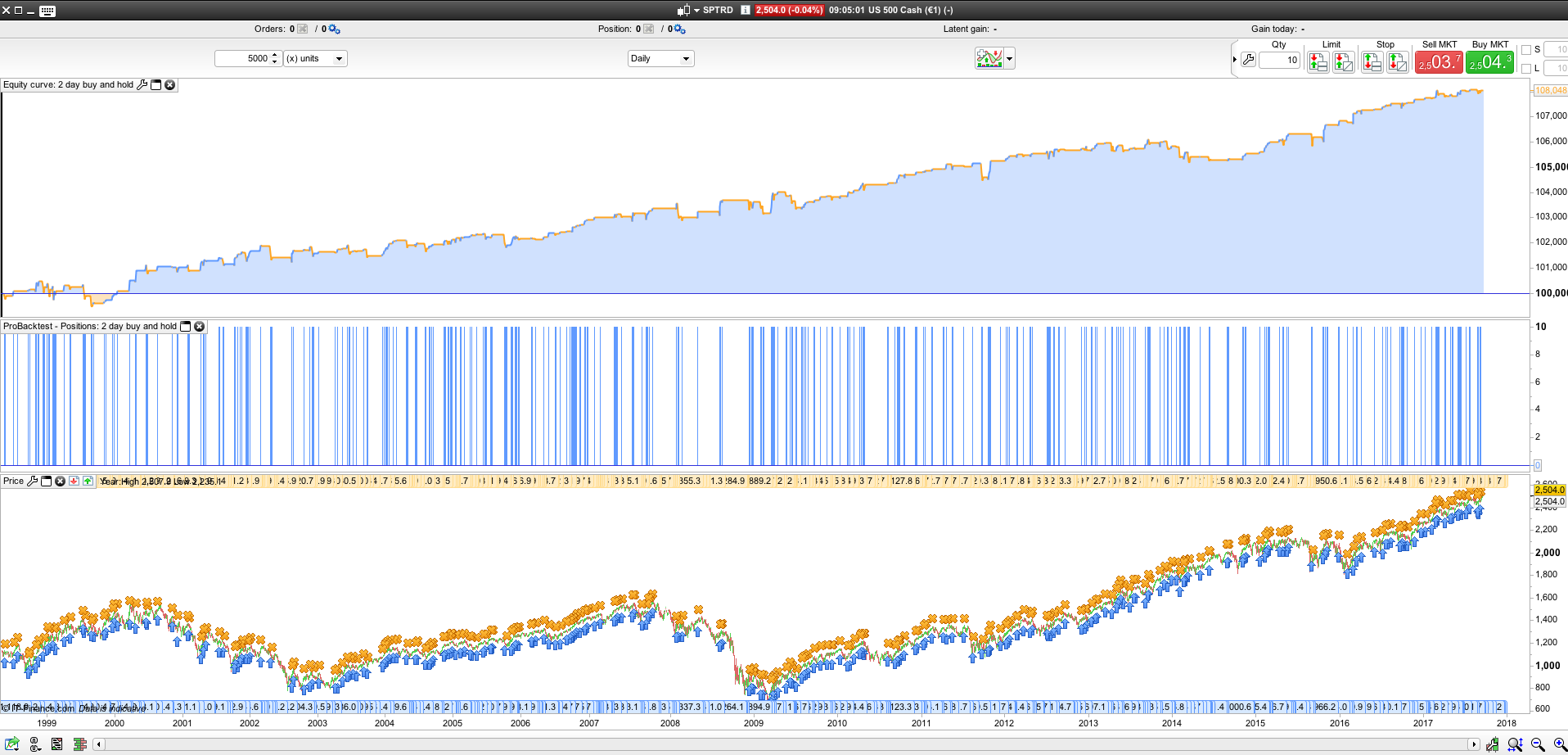

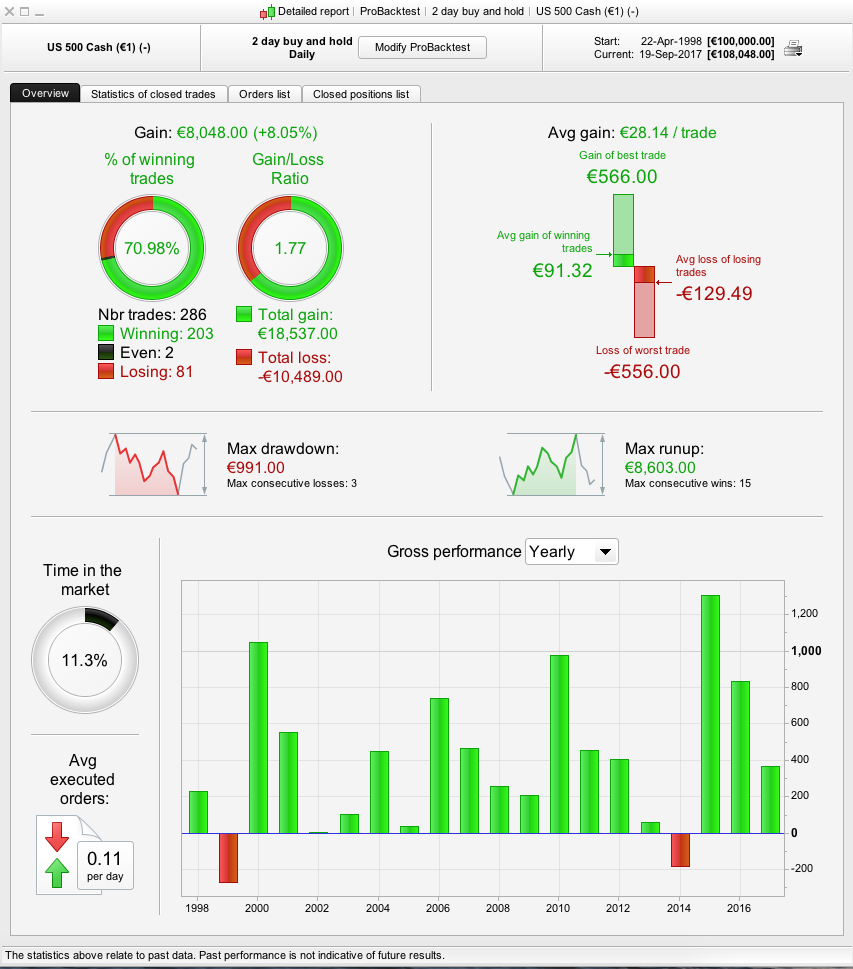

2 days buy and hold SP500

September 20, 2017, 7:29 AM

Strategies

18 Comments

{kind=link}

I found the baseline of this long only code online and did a few small changes to it.

It works as follow:

Entry rules:

- 2 periods moving average 1 day ago is greater than moving average of today.

- 2 periods moving average 10 days ago is greater than 11 days ago.

- Close above 7 periods moving average

Exit rule:

When the first entry rule is no longer true; exit.

DEFPARAM CumulateOrders = False

DEFPARAM PreloadBars = 200

//Position size

positionsize = 10

//Indicators

ma1 = average [2](close)

ma2 = average [7](close)

// Entry condition

// b1 = moving average at close of one day ago is greater than the moving average of today

// b2 = moving average at close 10 days ago is greater than the moving average of the close 11 days ago

b1 = ma1[1]>ma1[0]

b1 = b1 and ma1[10]>ma1[11]

b1 = b1 and close > ma2

// Entry

if b1 then

buy positionsize contracts at market

endif

// Exit

e1 = ma1[1]<=ma1[0]

if e1 then

sell at market

endif

// Stoploss

set stop ploss 100

Download

{kind=link}

Filename:

buy-and-hold-sp500-comparison.png

Downloads:

257

Download

Filename:

2-day-buy-and-hold.itf

Downloads:

386

Download

{kind=link}

Filename:

Skarmavbild-2017-09-19-kl.-09.05.01.png

Downloads:

157

Download

{kind=link}

Filename:

Skarmavbild-2017-09-19-kl.-09.04.44.png

Downloads:

295

Veteran

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...