Yang-Zhang volatility estimator

February 12, 2016, 1:56 PM

Indicators

2 Comments

{kind=link}

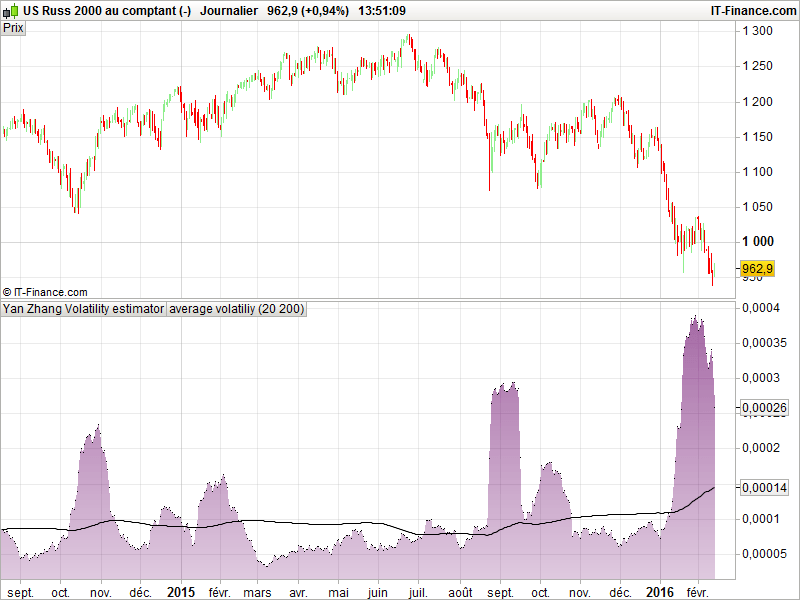

For those interested in options pricing and volatility indicator, here is one that draw recent volatility based on High, Low, Open and Close prices.

For more explanation see this paper : http://atmif.com/papers/range.pdf

//parameters

// n = 20

// averageP = 200

No = log( open ) - log( close[1] ) // normalized open

Nu = log( high ) - log( open ) // normalized high

Nd = log( low ) - log( open ) // normalized low

Nc = log( close ) - log( open ) // normalized close

Vrs = 1 / n * Summation[n]( Nu * ( Nu - Nc ) + Nd * ( Nd - Nc )) // RS volatility estimator

Noavg = 1 / n * Summation[n](No)

Vo = 1 / ( n - 1 ) * Summation[n]( SQUARE( No - Noavg ) )

Ncavg = 1 / n * Summation[n]( Nc )

Vc = 1 / ( n - 1 ) * Summation[n]( SQUARE( Nc - Ncavg ) )

k = 0.34 / ( 1.34 + ( n + 1 ) / ( n - 1 ) )

Vyangzhang = Vo + k * Vc + ( 1 - k ) * Vrs

avg = average[averageP](Vyangzhang)

return Vyangzhang, avg as "average volatiliy"

code adapted from AmiBroker

Download

Filename:

Yan-Zhang-Volatility-estimator.itf

Downloads:

103

New

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...