Wilder's CSI (Commodity Selection Index)

October 16, 2017, 7:45 AM

Indicators

1 Comment

{kind=link}

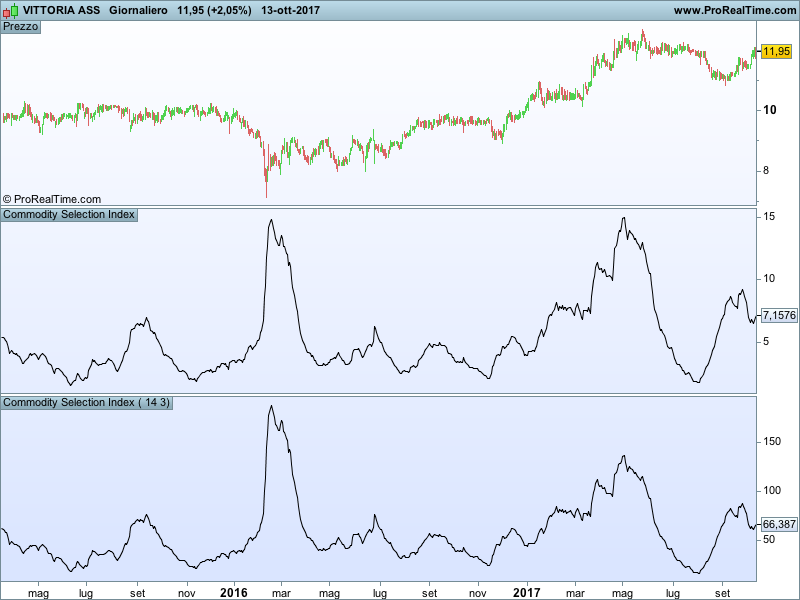

Welles Wilder introduced the CSI (Commodity Selection Index) in his bestseller “New concepts in technical trading” and uses this indicator to screen the commodities that are “strong” enough to be traded with a trend following system. The bigger the CSI the stronger the trend.

The index created originally by Wilder though is made for commodities and is not reliable for stocks. I tried to upgrade this indicator also for stocks by changing a little the formula and by redesigning the ATR formula.

I am attaching the original version and the modified version.

Blue skies!!

Code for commodities

Leverage=50

Margin=1000

Commissions=20

fact1=Leverage/(sqrt(Margin))

fact2=1/(150+Commissions)

csi=ADXR[14]*AverageTrueRange[14](close)*fact1*fact2*100

return csi as "Commodity Selection Index"

Code for stocks

//period=14

//MM=3

a=range/close[1]

b=abs(high-close[1])/close[1]

c=abs(low-close[1])/close[1]

TRbalanced=100*max(a,max(b,c))

ATRbalanced=Average[period,MM](trbalanced)

csi=ADXR[14]*atrbalanced

return csi as "Commodity Selection Index"

Download

Filename:

PRT-CSI-commodities.itf

Downloads:

41

Download

Filename:

PRT-CSI-stock.itf

Downloads:

43

Master

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...