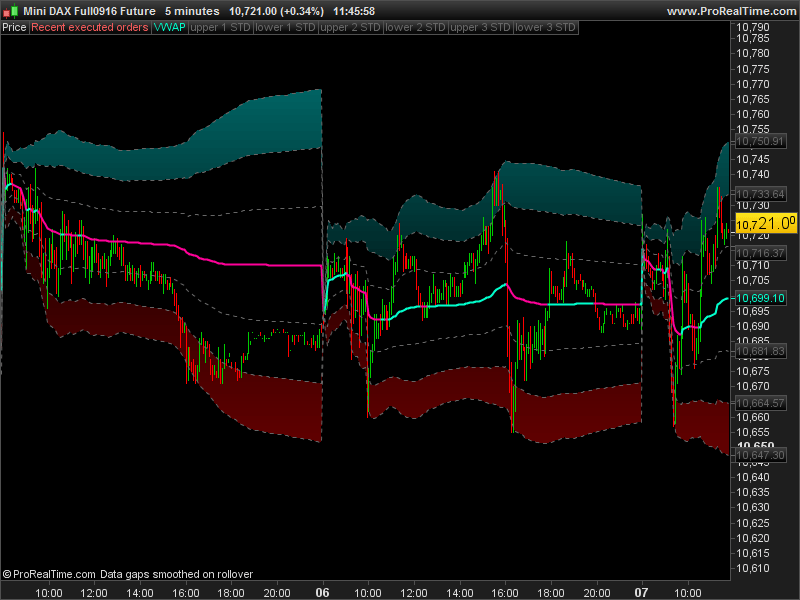

VWAP intraday

September 7, 2016, 11:10 AM

Indicators

49 Comments

{kind=link}

Volume Weighted Average Price is equal to the sum of the volume of every transaction multiplied by the price of every transaction divided by the total volume for the trading day.

This version is for intraday trading, the VWAP is resetting each day at the first intraday bar. I added the 3 standard deviation of the VWAP as upper and lower bands to expect reversal patterns. VWAP will be displayed only on instruments with volumes. This version is only compatible with Prorealtime 10.3.

The prorealtime v10.2 version of this VWAP indicator is now also available for download below this article, for everyone convenience 🙂

//PRC_VWAP intraday

//07.09.2016

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

d = max(1, intradaybarindex)

VWAP = SUMMATION[d](volume*typicalprice)/SUMMATION[d](volume)

if(intradaybarindex=0) then

sd = 0

else

sd = SUMMATION[d](max(abs(high-vwap),abs(vwap-low)))/d

endif

SDup1 = vwap+sd

SDlw1 = vwap-sd

SDup2 = vwap+sd*2

SDlw2 = vwap-sd*2

SDup3 = vwap+sd*3

SDlw3 = vwap-sd*3

if vwap>vwap[1] then

color = 1

else

color = -1

endif

RETURN VWAP coloured by color STYLE(LINE,2) as "VWAP", SDup1 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "upper 1 STD", SDlw1 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "lower 1 STD", SDup2 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "upper 2 STD", SDlw2 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "lower 2 STD", SDup3 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "upper 3 STD", SDlw3 coloured(102,102,102) STYLE(DOTTEDLINE,1) as "lower 3 STD"

Download

Filename:

PRC_VWAP-intraday-10.2.itf

Downloads:

673

Download

Filename:

PRC_VWAP-intraday.itf

Downloads:

1209

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...