Volume-Weighted Price Z-Score

{kind=link}

1. The problem: is price actually at an extreme?

When a price makes a large move, traders typically ask the same question: is it overextended, or can it continue? Classic oscillators like RSI give a partial answer — one based solely on price movement — but they ignore a critical dimension: volume.

Volume is context. A price move backed by heavy volume carries a completely different meaning than the same move on thin participation. The Volume-Weighted Price Z-Score combines both dimensions: it measures how many standard deviations the current price sits away from its Volume-Weighted Moving Average (VWMA), expressing the result as a normalised statistical score.

The output is a zero-centred oscillator with statistically meaningful boundaries at ±1 and ±2.5. It does not say “RSI is at 70”. It says “price is 2.8 standard deviations above where volume considers fair value”. That distinction matters.

2. How the indicator is calculated

The indicator is built in four sequential steps.

Step 1 — Volume-Weighted Moving Average (VWMA)

The VWMA is computed as the volume-weighted reference price:

volSum = summation[lookback](volume)

IF volSum > 0 THEN

vwmaVal = summation[lookback](CustomClose * volume) / volSum

ELSE

vwmaVal = CustomClose

ENDIF

Price multiplied by volume is accumulated over the lookback window, then divided by total volume. The result is the true market-weighted average price — not a simple arithmetic mean of closes. If no volume is available, the current price is used as a fallback.

Step 2 — Logarithmic deviation

Instead of a simple arithmetic difference (price − VWMA), the log of their ratio is used:

IF vwmaVal > 0 THEN

logDev = log(CustomClose / vwmaVal)

ELSE

logDev = 0

ENDIF

Logarithmic deviation is symmetric: a +100% move and a −50% move carry equal absolute weight. It is also time-additive, making it suitable for cross-asset and cross-timeframe comparisons.

Step 3 — Statistical normalisation (Z-Score)

The log deviation is divided by its own historical volatility to produce the raw Z-Score:

volMeasure = std[lookback](logDev)

IF volMeasure > 0 THEN

rawZ = logDev / volMeasure

ELSE

rawZ = 0

ENDIF

This step is the core of the indicator. Dividing by the standard deviation produces a dimensionless, statistically interpretable value: a reading of +2 means price is 2 standard deviations above its volume-weighted fair value — a condition that, under a normal distribution, occurs less than 5% of the time.

Step 4 — Final smoothing

A simple moving average is applied to reduce short-term noise:

zScore = average[smoothing,1](rawZ)

The second parameter (1) specifies a simple moving average. Higher smoothing values produce a cleaner line but introduce more lag.

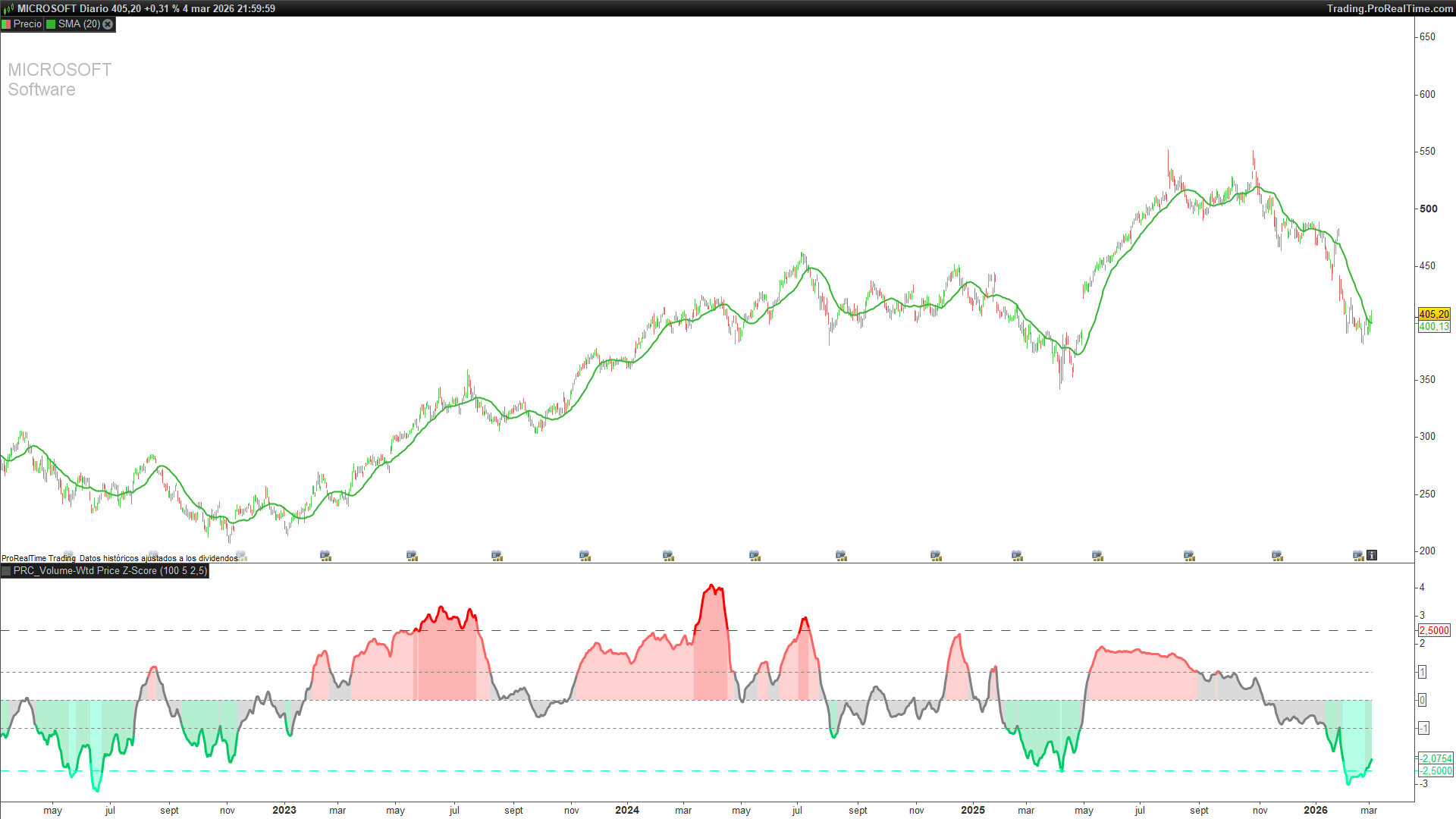

3. Reading the indicator

The Z-Score oscillates around zero. The key reference levels are ±1 (one standard deviation) and ±2.5 (the extreme threshold). Five colour zones make interpretation immediate:

• Bright red (Z ≥ +2.5): Extreme overbought. Price is statistically far above its volume-weighted mean. Less than 1.2% of observations in a normal distribution.

• Soft red (+1 to +2.5): Elevated bullish zone. Market is stretched. Use caution when looking for long entries.

• Grey (−1 to +1): Neutral zone. Price is close to volume-weighted fair value. No statistical edge in either direction.

• Soft green (−2.5 to −1): Moderate bearish zone. Potential area of interest for long setups with additional confirmation.

• Bright green (Z ≤ −2.5): Extreme oversold. Price is statistically far below its volume-weighted mean. Potential reversal candidate.

A few practical notes on reading the indicator:

• The indicator provides context, not standalone buy/sell signals. Always combine with price action or other confirmation tools.

• Zero-line crossovers are meaningful: a move from negative to positive territory with rising volume can signal a bias shift.

• Extreme readings (≥ ±2.5) are the most actionable, especially when accompanied by volume divergence or price divergence.

• In strong trending markets, the Z-Score can remain elevated for many bars. This is not a malfunction — it means the trend is consistently backed by volume.

4. Parameters and presets

The indicator has three configurable parameters:

• lookback (default: 100): Calculation window for the VWMA, log deviation, and volatility measurement. Larger values produce smoother output and fewer false signals, at the cost of added lag.

• smoothing (default: 5): Periods of the final simple moving average applied to the raw Z-Score. Reduces short-term noise.

• extremeThresh (default: 2.5): Statistical threshold defining overbought/oversold extremes. Typical range: 2.0 (more signals) to 3.0 (only genuine extremes). For highly volatile assets such as crypto or small caps, consider raising it to 3.0. For low-volatility instruments such as bond ETFs, 2.0 may capture meaningful extremes more frequently.

Three presets are included in the code. Uncomment the relevant block before applying the indicator:

• Default (lookback=100, smoothing=5): Swing trading on daily and 4H charts.

• Fast Response (lookback=50, smoothing=3): Intraday trading and scalping on 15-min charts or below.

• Smooth Trend (lookback=200, smoothing=8): Position trading on weekly charts.

5. Full ProRealTime code

The code below is ready to paste into the ProBuilder editor.

//--------------------------------------------

// PRC_Volume-Weighted Price Z-Score(by QuantAlgo)

// version = 0

// 05.03.2026

// Iván González @ www.prorealcode.com

// Sharing ProRealTime knowledge

//--------------------------------------------

//=== PRESET CONFIGURATION ===

//--------------------------------------------

lookback = 100

smoothing = 5

//=== THRESHOLD ===

extremeThresh = 2.5

//--------------------------------------------

//=== VWMA CALCULATION ===

//--------------------------------------------

volSum = summation[lookback](volume)

IF volSum > 0 THEN

vwmaVal = summation[lookback](CustomClose * volume) / volSum

ELSE

vwmaVal = CustomClose

ENDIF

//--------------------------------------------

//=== Z-SCORE ===

//--------------------------------------------

IF vwmaVal > 0 THEN

logDev = log(CustomClose / vwmaVal)

ELSE

logDev = 0

ENDIF

volMeasure = std[lookback](logDev)

IF volMeasure > 0 THEN

rawZ = logDev / volMeasure

ELSE

rawZ = 0

ENDIF

zScore = average[smoothing,1](rawZ)

//--------------------------------------------

//=== DISCRETE COLOR RANGES (5 tramos) ===

//--------------------------------------------

IF zScore >= extremeThresh THEN

cr = 255

cg = 0

cb = 0

ELSIF zScore >= 1 THEN

cr = 255

cg = 100

cb = 100

ELSIF zScore > -1 THEN

cr = 128

cg = 128

cb = 128

ELSIF zScore > -extremeThresh THEN

cr = 0

cg = 200

cb = 100

ELSE

cr = 0

cg = 255

cb = 170

ENDIF

//--------------------------------------------

//=== FILL BETWEEN Z-SCORE AND ZERO ===

//--------------------------------------------

zeroLine = 0

colorbetween(zScore, zeroLine, cr, cg, cb, 75)

//--------------------------------------------

//=== REFERENCE LEVELS ===

//--------------------------------------------

posThresh = extremeThresh

negThresh = -extremeThresh

sigmaP1 = 1

sigmaN1 = -1

//--------------------------------------------

RETURN zScore coloured(cr, cg, cb) style(line, 3) AS "Z-Score", zeroLine coloured(128,128,128) style(dottedline) AS "Zero", posThresh coloured(255,0,0) style(dottedline2) AS "+Extreme", negThresh coloured(0,255,170) style(dottedline2) AS "-Extreme", sigmaP1 coloured(128,128,128) style(dottedline) AS "+1s", sigmaN1 coloured(128,128,128) style(dottedline) AS "-1s"