Trading Activity Index

{kind=link}

Introduction

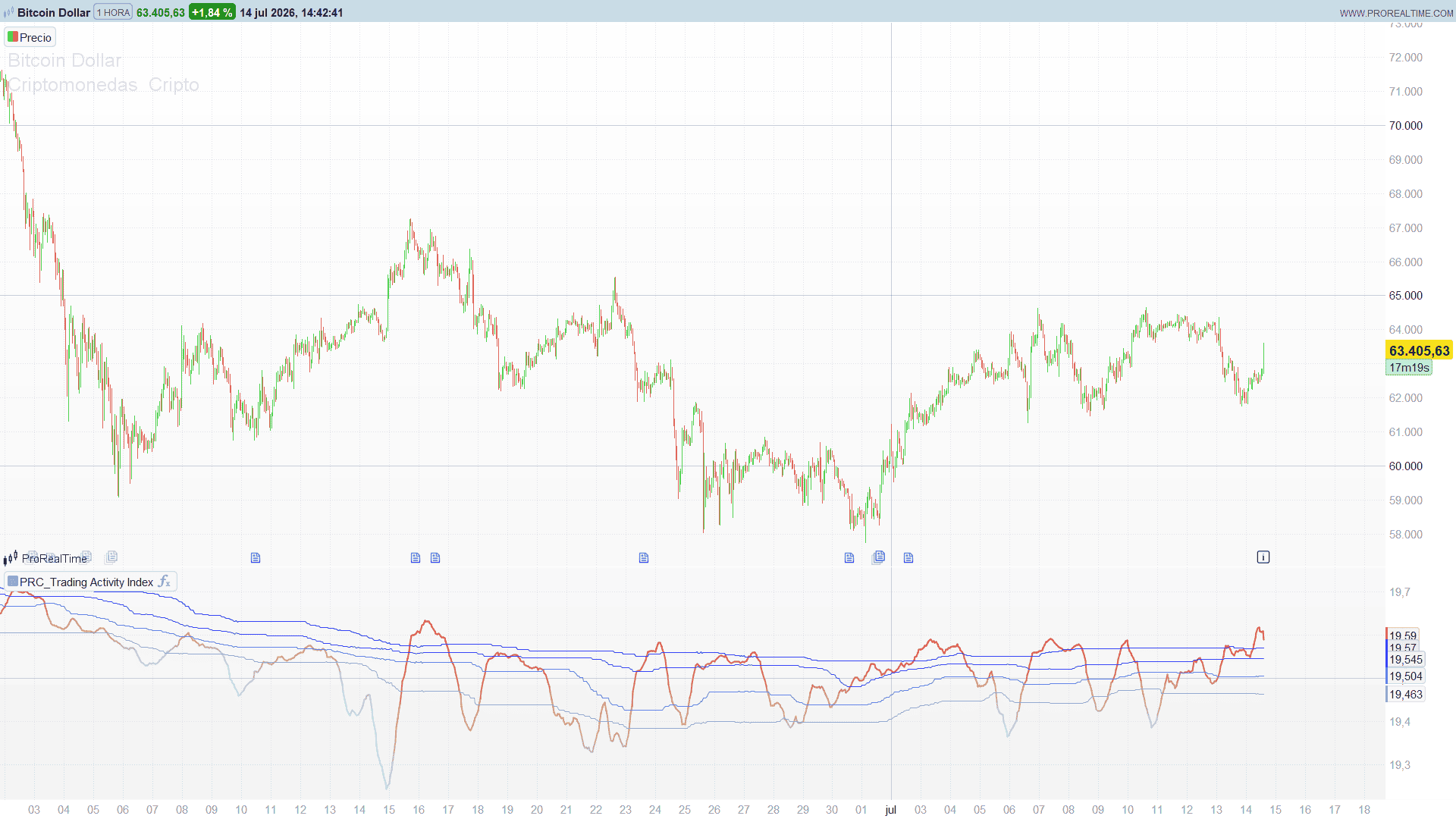

Zeiierman’s Trading Activity Index answers a deceptively simple question: is the market unusually busy right now, or unusually quiet — relative to its own recent history?

Plain volume cannot answer it well, because a fixed number of shares or contracts means very different things at different price levels, and because “busy” is only meaningful against a baseline. This indicator fixes both problems. It measures dollar volume (price times volume, a proxy for the capital changing hands), compresses it with a logarithm so the huge dynamic range becomes readable, and then ranks the result against a rolling window of its own past using percentile bands. The output is a clean sub-panel oscillator: one activity line coloured by a cool-to-warm gradient, and four quintile bands (P20/P40/P60/P80) that carve the panel into low-, normal- and high-activity zones.

Theory Behind the Indicator

1. Dollar volume — a better activity proxy

The engine never looks at raw volume. It builds:

dollarVolume = close × volume

A million shares trading at $5 and a million shares trading at $500 represent wildly different levels of participation; dollar volume captures that, raw volume does not. This is the same reasoning behind VWAP and behind most “smart money” flow tools: capital rotated, not units traded.

2. Log compression — making the range legible

Dollar volume spans several orders of magnitude across a session and across instruments. Plotted raw, it is a spiky mess dominated by a handful of outliers. The indicator averages it over a short formation window (20 bars) and takes the natural logarithm:

VOLSCALE = log( max( SMA(dollarVolume, 20), 1e-10 ) )

The max(…, 1e-10) is a floor that keeps the logarithm defined when volume is zero (dead bars, pre-market). The log turns a multiplicative quantity into an additive, roughly-stationary line — the blue-to-orange series you actually read. This is the “Trading Activity” plot.

3. Percentile bands — ranking activity against its own history

A value of VOLSCALE means nothing in isolation. Is 18.4 high? Only the instrument’s own history can say. So over a longer history window (252 bars) the indicator computes the 20th, 40th, 60th and 80th percentiles of VOLSCALE and draws them as four bands. They split the panel into quintiles of activity:

- Below P20 — unusually quiet; the market is ignoring this instrument.

- P20–P80 — normal range of participation.

- Above P80 — unusually busy; a spike in capital rotation, often around news, breakouts or institutional repositioning.

Because the bands are rolling percentiles, they adapt to the regime: a stock that gets structurally more liquid sees all four bands drift up, and “high activity” is re-based automatically. No fixed thresholds.

4. The colour gradient — regime at a glance

The activity line is coloured by rank01, the min-max normalised position of VOLSCALE inside the window:

rank01 = clamp( (VOLSCALE − min) / (max − min), 0, 1 )

colour = lerp( lightBlue(173,216,230) → redOrange(255,69,0), rank01 )

Cool blue when activity sits near the window’s floor, warm orange/red as it approaches the ceiling. The colour and the band position tell the same story two ways, which makes the read instantaneous.

The engineering problem: four rolling percentiles without a percentile function

This is where the translation earns its keep. Pine computes each band with ta.percentile_linear_interpolation(VOLSCALE, 252, P). ProBuilder has no percentile primitive, and the obvious workarounds are expensive:

- Bisection (discretise the value range into ~100 steps, count how many samples fall below each step): about 100 × 252 ≈ 25,200 operations per band, so ~100,000 per bar for four bands.

- k-th smallest by counting (for each candidate, count how many samples are ≤ it): O(N²) ≈ 63,500 operations per bar.

Either one, run on every bar of an intraday history, is the kind of load that makes ProRealTime crawl.

The port uses a histogram instead, and computes all four percentiles in essentially one pass over the window:

- Find the window’s min and max (one loop — reused for the colour gradient, so it is free).

- Slot every one of the 252 values into one of 100 bins: bin = floor((value − min) / binWidth). One loop over the window.

- Walk the bins once, accumulating a running count (the empirical CDF). The first bin where the cumulative fraction crosses 0.20 gives P20, 0.40 gives P40, and so on — all four in a single sweep.

Total cost is roughly N + 3·bins ≈ 700 operations per bar — about 35× cheaper than bisection, and it does not get worse if you enlarge the history window (the expensive part is the single O(N) binning pass, independent of the number of bands or bins). This is the canonical way to extract multiple quantiles at once, and it is the right tool the moment N gets large.

What was approximated, and why it does not matter

The histogram returns each percentile by inverse empirical CDF at a resolution of (max − min) / 100, whereas Pine’s percentile_linear_interpolation interpolates linearly between the two nearest ranks. With 252 samples the two disagree by less than one position out of 252 — a difference far thinner than the bands’ own line width. If you ever wanted it tighter, raising the bin count (say to 200) halves the resolution error and costs almost nothing, because it only lengthens the cheap O(bins) loops, never the O(N) binning pass. It is an honest, documented approximation, not a silent shortcut — and visually the bands are indistinguishable from the original.

Key Features at a Glance

- Dollar-volume base:

close x volume, capital rotated rather than raw units traded. - Log compression: natural log of a 20-bar average; tames the dynamic range into a readable line.

- Percentile bands: rolling P20/P40/P60/P80 over 252 bars; regime-adaptive quintiles of activity.

- Colour gradient: cool blue (quiet) to warm orange/red (busy), driven by the min-max rank.

- Sub-panel oscillator: separate panel; one activity line plus four reference bands.

How to Read the Indicator

- The activity line is the log-scaled dollar-volume flow. Rising = capital rotation increasing; falling = the market losing interest. Its colour reinforces the level: warm = active, cool = quiet.

- The bands are context. The line crossing above P80 flags unusually high activity — the fuel behind genuine breakouts and trend legs. The line sinking below P20 flags dead conditions, where breakouts are more likely to fail for lack of participation.

- Regime shifts show up as the line migrating from the lower quintiles into the upper ones (or vice versa) and holding there — an activity expansion or contraction, not a one-bar spike.

Practical Applications

- Breakout confirmation. Take price breakouts only when the activity line is in the upper quintile (above P60/P80). A breakout on sub-P20 activity is a low-conviction move.

- Filter for mean-reversion. Fade extensions preferentially in quiet regimes (line below P40), where there is no participation to sustain a trend.

- Session / instrument screening. Because the bands are self-normalising, the same “above P80” rule flags unusual activity consistently across instruments and timeframes — a natural building block for an “unusual volume” screener.

- Confluence. Combine a warm, above-P80 activity read with your own structure or momentum tools; treat cool, sub-P20 readings as a caution flag on any signal.

Indicator Configuration

The indicator ships as a single sub-panel script (the original is overlay=false, so nothing goes on the price chart).

lenForm(default 20): Formation window, the number of bars averaged before the log is taken.lenHist(default 252): History window, the bars used for the rolling percentiles and the colour range.nBins(default 100): Histogram resolution for the percentiles. Implementation detail, not in the original; higher is finer at negligible extra cost.

Code

//----------------------------------------------

//PRC_Trading Activity Index Zeiierman

//version = 0

//14.07.26

//Ivan Gonzalez @ www.prorealcode.com

//Traducido de "Trading Activity Index (Zeiierman)" (PineScript v6)

//Autor original: Zeiierman

//Sharing ProRealTime knowledge

//----------------------------------------------

// --- Parametros (ajustables en el panel del indicador) ---

lenForm = 20 // Formation Window (barras): promedio del dollar volume

lenHist = 252 // History Window (barras): percentiles y bandas

nBins = 100 // Resolucion del histograma de percentiles

//----------------------------------------------

// --- Dollar Volume medio y VOLSCALE (log) ---

//----------------------------------------------

dv = close * volume

dlrVolAvg = average[lenForm](dv)

vscale = log(max(dlrVolAvg, 0.0000000001))

//----------------------------------------------

// --- Defaults (warmup) ---

//----------------------------------------------

p20 = undefined

p40 = undefined

p60 = undefined

p80 = undefined

rMain = 173

gMain = 216

bMain = 230

//----------------------------------------------

validStart = lenForm - 1

if barindex >= validStart then

neff = min(lenHist, barindex - validStart + 1)

// --- Min / Max de la ventana (color y escala del histograma) ---

vMin = vscale

vMax = vscale

for i = 0 to neff - 1 do

if vscale[i] > vMax then

vMax = vscale[i]

endif

if vscale[i] < vMin then

vMin = vscale[i]

endif

next

// --- rank01 -> color gradiente de la linea principal ---

if vMax > vMin then

rank01 = (vscale - vMin) / (vMax - vMin)

if rank01 < 0 then

rank01 = 0

endif

if rank01 > 1 then

rank01 = 1

endif

else

rank01 = 0.5

endif

rMain = round(173 + 82 * rank01)

gMain = round(216 - 147 * rank01)

bMain = round(230 - 230 * rank01)

// --- Percentiles P20/P40/P60/P80 por histograma O(N + bins) ---

if vMax > vMin then

stepf = (vMax - vMin) / nBins

for b = 0 to nBins do

$bc[b] = 0

next

for m = 0 to neff - 1 do

idx = floor((vscale[m] - vMin) / stepf)

if idx < 0 then

idx = 0

endif

if idx > nBins - 1 then

idx = nBins - 1

endif

$bc[idx] = $bc[idx] + 1

next

p20 = vMin

p40 = vMin

p60 = vMin

p80 = vMin

d20 = 0

d40 = 0

d60 = 0

d80 = 0

cum = 0

for s = 0 to nBins do

fr = cum / neff

testv = vMin + stepf * s

if d20 = 0 and fr >= 0.2 then

p20 = testv

d20 = 1

endif

if d40 = 0 and fr >= 0.4 then

p40 = testv

d40 = 1

endif

if d60 = 0 and fr >= 0.6 then

p60 = testv

d60 = 1

endif

if d80 = 0 and fr >= 0.8 then

p80 = testv

d80 = 1

endif

if s < nBins then

cum = cum + $bc[s]

endif

next

else

p20 = vMin

p40 = vMin

p60 = vMin

p80 = vMin

endif

endif

//----------------------------------------------

return vscale as "Trading Activity" coloured(rMain, gMain, bMain, 255) style(line, 2), p20 as "P20" coloured(138, 173, 235, 255), p40 as "P40" coloured(104, 130, 240, 255), p60 as "P60" coloured(69, 86, 245, 255), p80 as "P80" coloured(35, 43, 250, 255)