Super bandpass filter - John Ehlers

July 17, 2016, 7:41 PM

Indicators

4 Comments

{kind=link}

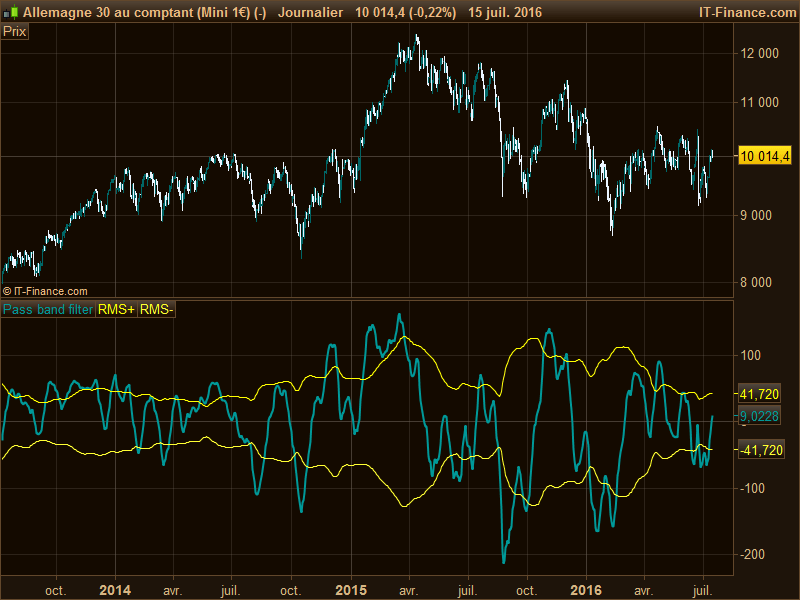

Here is the newest indicator by John Ehlers described in the new traders’tips of July 2016, like his other indicators this one is also a nearly-zero lag filter which is another attempt to filter out noises from high and low frequencies of market data.

John Ehlers describe the trading rules of this new indicator as this:

- Buy on the filter crossing above its -RMS line

- Short on the filter crossing below its RMS line

- Exit long when the filter either crosses below its RMS or crosses below -RMS (which signifies a false entry signal)

- Cover short when the filter either crosses above its -RMS or crosses above RMS (which signifies a false entry signal)

// parameters

flen = 40 //fast length

slen = 60 //slow length

if barindex>slen then

a1= 5/flen

a2= 5/slen

PB = (a1 - a2) * close + (a2*(1 - a1) - a1 * (1 - a2))* close[1] + ((1 - a1) + (1 - a2))*(PB[1])- (1 - a1)* (1 - a2)*(PB[2])

RMSa = summation[50](PB*PB)

RMSplus = sqrt(RMSa/50)

RMSminus = -RMSplus

endif

RETURN PB as "Pass band filter", RMSplus as "RMS+", RMSminus as "RMS-"

Download

Filename:

PRC_Superbandpass_filter.itf

Downloads:

576

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...