Short term Volume And Price Oscillator (SVAPO)

November 9, 2015, 11:27 PM

Indicators

2 Comments

{kind=link}

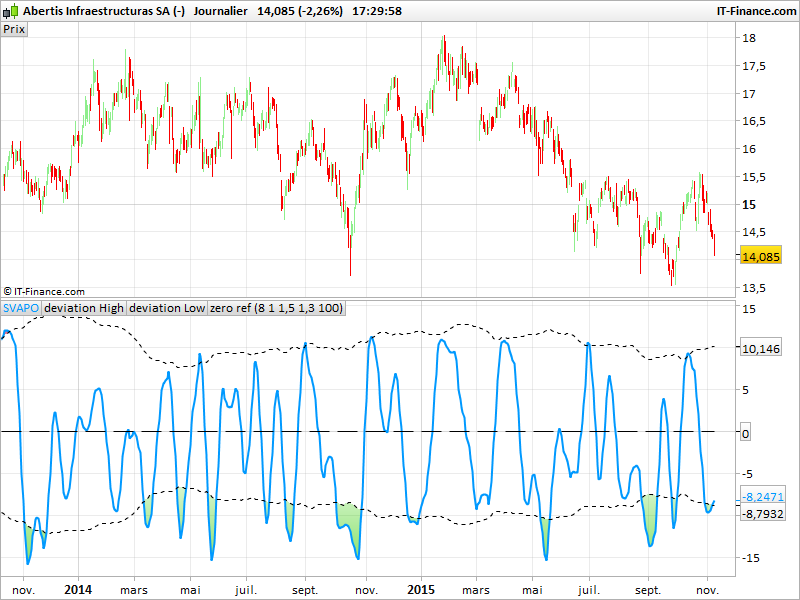

This oscillator is based between the relationship that exist between price and volume. It combines these values to help detect up and down trend.

It is devoted to detect short term trades based on standard deviation of recent moves, so bearish signals occurs when oscillator is crossing the lower deviation and bullish movement when oscillator is crossing down the upper deviation.

Parameters :

- period = 8

- cutoff = 1

- devH = 1.5

- devL = 1.3

- stdevper = 100

haOpen = ((Open[1]+High[1]+Low[1]+Close[1])+(Open[2]+High[2]+Low[2]+Close[2]))/2

haCl = ((Open+High+Low+Close)/4+haOpen+MAX(High,haOpen)+MIN(Low,haOpen))/4

haC = tema[period/1.6](haCl)

vav = average[period*5](volume)

vave = vav[1]

vmax = vave * 2

if(volume<vmax) THEN

vc = volume

else

vc = vmax

endif

vtr = tema[period](linearregressionslope[period](volume))

if haC>haC[1]*(1+cutoff/1000) AND vtr>=vtr[1] THEN

tosum = vc

ELSIF haC<haC[1]*(1+cutoff/1000) AND vtr>vtr[1] THEN

tosum = -vc

ENDIF

SVAPO = tema[period](summation[period](tosum)/(vave+1))

hi = devH*STD[stdevper](SVAPO)

lo = -devL*STD[stdevper](SVAPO)

RETURN SVAPO as "SVAPO", hi as "deviation High", lo as "deviation Low", 0 as "zero ref"

Download

{kind=link}

Filename:

Abertis-Infraestructuras-SA-.png

Downloads:

25

Download

Filename:

Short-term-Volume-Price-Osc.itf

Downloads:

134

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...