Machine Learning Z-Score

{kind=link}

The Machine Learning Z-Score indicator by Steversteves is a popular TV publication that combines automatic lookback selection (advertised as “Machine Learning”) with a z-score-based mean-reversion signal. A faithful ProBuilder port was requested in this forum thread.

After translating it line by line and testing it on several markets and timeframes, the results were uninspiring. This article is the rest of the process: a step-by-step audit of the original logic, the structural defects we identified, the corrections we applied, and the honest backtest of the corrected version. The final takeaway is more useful than any indicator: not every script that says “Machine Learning” deserves the label, and what looks sophisticated may be hiding very simple flaws.

What the Original Does

The original is two pieces stacked together:

- Automatic lookback selection. The script computes the correlation between price and bar index over ten windows (50, 100, 150, …, 500 bars). It picks the window with the highest R² (or absolute Pearson coefficient, both branches exist in the code) and uses that length to compute the z-score. The marketing label for this step is “Machine Learning”.

- Z-score mean-reversion. With the chosen lookback len:

- meanPrice = Average[len](close)

- stdPrice = Std[len](close)

- z = (close – meanPrice) / stdPrice

The signal logic in v1 is: BUY when z stays at the lowest value of the last len bars for more than 8 consecutive bars; SELL when symmetric. A take-profit is plotted at a “dynamic” level that, on closer inspection, equals the local mean.

Six Structural Defects of the Original

We found six issues in v1. Listed in order of impact:

1. The “Machine Learning” step picks the wrong window

Mean-reversion strategies make statistical sense in range-bound regimes, not in trending markets. The intuition is straightforward: when price is trending cleanly in one direction, a low z-score is the start of a continuation move, not the start of a reversion to the mean. The mean only matters when the mean is itself stable, which happens precisely when R² is low (no clear linear trend, sideways behaviour).

The original picks the window with maximum R², doing the opposite of what mean-reversion needs. It auto-selects the lookback in which price has the cleanest trend, then trades reversions against that trend. The two halves contradict each other by design.

The fix is to invert the criterion: pick the window with the minimum R² (the most range-bound).

2. The buy trigger is auto-satisfied

The BUY condition in v1 is:

IF c <= lowz THEN

buywait = buywait + 1

...

ENDIF

with lowz = Lowest[len](c). But c (the current z-score) is itself part of the window that Lowest[len] looks back over. Whenever c makes a new len-bar low, by definition c = lowz. The condition fires automatically on every new minimum, with no filter on signal quality at all. It is not detecting anything, it is definitionally true whenever price extends its extreme.

A robust trigger is a cross back from the extreme:

buyCross = (z[1] <= -zthreshold) AND (z > -zthreshold)

This fires when the z-score has been in deep negative territory and now crosses back up. It signals a reversion already in progress, not a continuation of the fall.

3. The “wait” counter has a reset bug

The original code is:

IF c <= lowz THEN

buywait = buywait + 1

IF buywait > 8 THEN

// emit signal

buywait = 0

ENDIF

ENDIF

There is no ELSE buywait = 0. The counter only resets when a signal fires, never when the condition fails. As a result, 5 bars of c <= lowz accumulated today, 4 bars from two months ago, and 1 bar from last year can sum to 10 and emit a “8 consecutive bars” signal that is anything but consecutive. The corrected version does not need the counter at all (the cross trigger above replaces it).

4. Z-score on raw price is biased by the trend

Computing z = (close – mean) / std on a trending price series produces a misleading z-score. As price trends up, the rolling mean trails behind; the residual (close – mean) stays positive for long stretches, and the standard deviation is dominated by the trend itself. The “extreme” reading is not extreme relative to the noise; it is just the trend.

A cleaner approach is to z-score the residuals of a linear regression rather than raw close:

trendline = LinearRegression[len](close)

src = close - trendline

meanSrc = Average[len](src)

stdSrc = Std[len](src)

z = (src - meanSrc) / stdSrc

By construction the residuals have near-zero mean and a standard deviation that measures dispersion orthogonal to the trend. The z-score now measures how far price is from its own trend, not how far it is from a lagging average. We expose this as an optional input (useDetrend) so both modes can be compared.

5. No regime filter

Mean-reversion longs in the middle of a clean downtrend keep catching falling knives. The original has no regime filter, so every extreme z-score fires regardless of context. We add an optional one (regimeFilter) with two modes:

- MA slope: longs only when the moving average is rising (ma > ma[slopeBars]), shorts only when falling. Note we deliberately do not use close > MA here; that condition collides with the very setup the z-score is detecting (price stretched below mean), so as soon as malen is reduced the filter blocks almost everything. The slope test sidesteps that problem.

- ADX low: signals only when ADX is below a configurable threshold (operate only in non-trending markets).

6. The “smoothed z-score” used as TP is mathematically noise

The original computes:

sma = Average[len](c)

z0 = a + sma * b // "dynamic take-profit"

But Average[len] of the z-score c, where c itself is (price – mean) / std and the inner mean is computed over the same len, is approximately zero by construction. The “smoothed z-score” is dominated by noise around zero. Multiplying it by b and adding it to a produces a target level that is essentially a plus a small random offset. There is no statistical content in this construction.

The replacement is simple. The take-profit reference is the local mean directly:

IF useDetrend = 1 THEN

tpRef = LinearRegression[len](close) + meanSrc

ELSE

tpRef = meanSrc

ENDIF

This guarantees tpRef is always in price units and represents the actual expected reversion target.

Additional Practical Layers

Beyond fixing the six defects above, the v2 adds practical layers that make the indicator usable as a study tool:

- Fixed stop loss at slMult × ATR from entry (configurable; predictable risk per trade).

- Risk/reward filter: signals are dropped at source if (tpRef – entry) / (entry – stop) < minRR. The default minRR = 1 guarantees every emitted signal has at least 1R reward potential.

- Cooldown: minimum cooldownBars between two signals on the same side. Prevents clusters of 2-3 entries in adjacent bars when the z-score oscillates near the threshold.

- Inline trade tracking: the indicator detects, bar by bar, whether each emitted trade closes at TP or SL. Counters accumulate trades, wins, losses, sum of R, broken down by long/short. The result is rendered in a small statistics panel anchored to the top-right corner of the chart via ANCHOR(TOPRIGHT, XSHIFT, YSHIFT). Conservative tie-break: if both TP and SL are touched on the same bar, the SL wins.

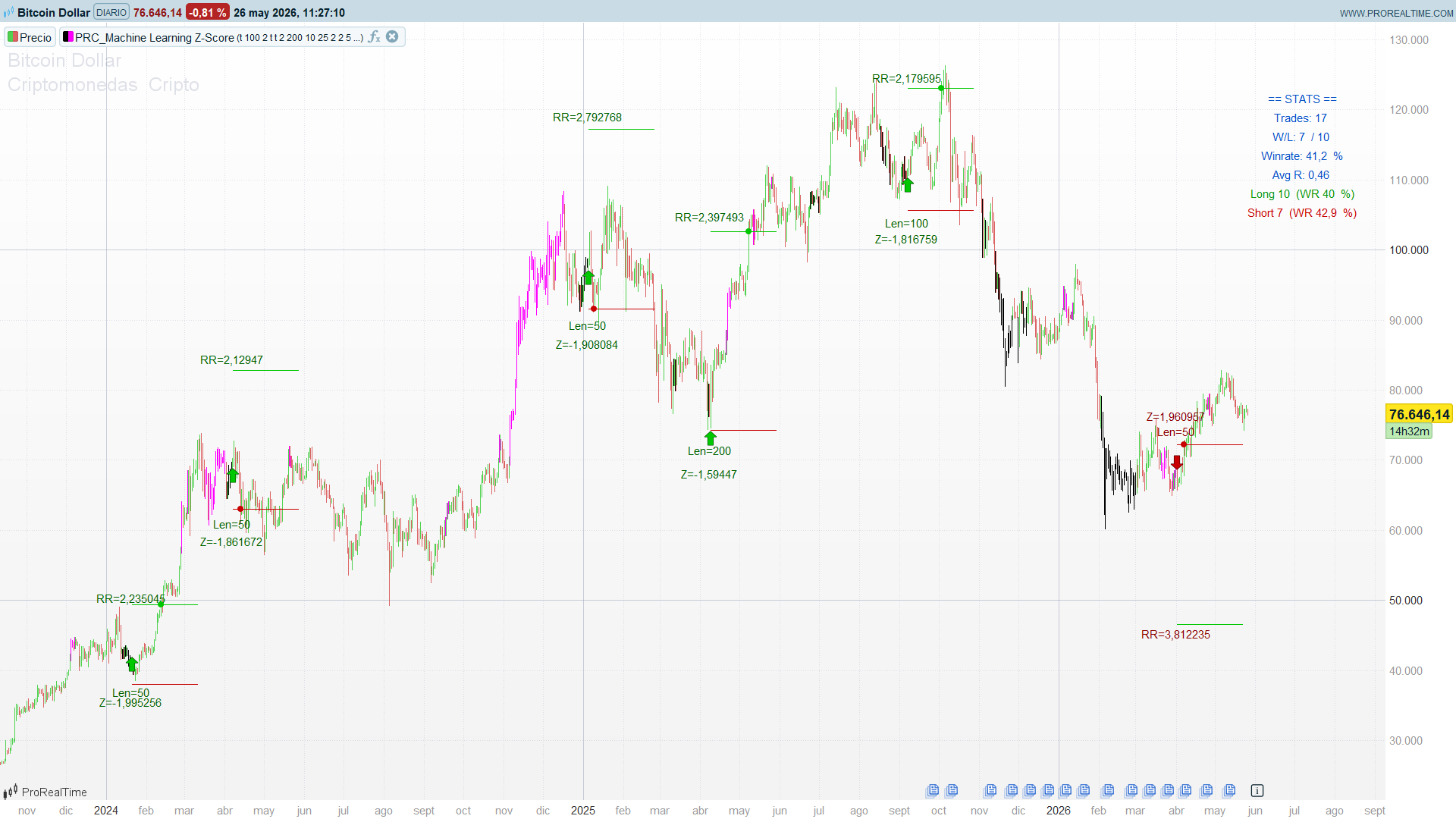

How to Read the Stats Box

When the indicator is loaded, a fixed panel appears in the top-right corner:

== STATS ==

Trades: 49

W/L: 22 / 27

Winrate: 44.9 %

Avg R: 0.57

Long 36 (WR 47.2 %)

Short 13 (WR 38.5 %)

Interpretation:

- Avg R > 0 means positive expectancy (every average trade gains R-units). Below zero, the system is not operable as-is.

- Winrate around 45% with Avg R near 0.5 is the typical signature of a reasonable mean-reversion system with minRR = 1 and the actual TP often farther than 1R from entry.

- Long WR ≠ Short WR flags directional asymmetry that may be exploitable via the regime filter.

The Code

//-------------------------------------------------------------

// PRC_Machine Learning Z-Score v2.4

// version = 2.4

// Mejorado por Ivan Gonzalez @ www.prorealcode.com

// Basado en la idea original de Steversteves (v1 publicada 10.09.25)

//Sharing ProRealTime knowledge

//-------------------------------------------------------------

// ===== Inputs =====

//-------------------------------------------------------------

autoadjust = 1 // 1 = pick lookback with min R2, 0 = use lengthinput

lengthinput = 100 // Fixed lookback when autoadjust = 0

zthreshold = 2.0 // Extreme z-score threshold (+/-2 sigma)

useDetrend = 0 // 1 = z-score on LinReg residuals, 0 = raw price

regimeFilter = 0 // 1 = apply regime filter, 0 = no filter

regimeMode = 1 // 1 = MA slope, 2 = ADX low

malen = 200 // MA length for regime filter

slopeBars = 10 // Bars back for MA slope test

adxLimit = 25 // ADX threshold (regimeMode = 2)

slMult = 2.0 // Stop loss = slMult * ATR from entry

minRR = 1.0 // Minimum reward/risk ratio to emit signal

cooldownBars = 5 // Minimum bars between signals on the same side

plottgt = 1 // Draw TP / SL segments at each signal

showTradeClose = 1 // Draw a point where TP or SL is hit

showStats = 1 // Show stats panel in top-right corner

barcolor = 1 // Colour candles in extreme zones

//-------------------------------------------------------------

// ===== Seleccion automatica de lookback (R2 minimo) =====

//-------------------------------------------------------------

cor1 = R2[50](close)

cor2 = R2[100](close)

cor3 = R2[150](close)

cor4 = R2[200](close)

cor5 = R2[250](close)

cor6 = R2[300](close)

cor7 = R2[350](close)

cor8 = R2[400](close)

cor9 = R2[450](close)

cor10 = R2[500](close)

mincor = MIN(MIN(MIN(MIN(MIN(cor1,cor2),cor3),MIN(cor4,cor5)),MIN(cor6,cor7)),MIN(MIN(cor8,cor9),cor10))

IF autoadjust = 1 THEN

IF mincor = cor1 THEN

len = 50

ELSIF mincor = cor2 THEN

len = 100

ELSIF mincor = cor3 THEN

len = 150

ELSIF mincor = cor4 THEN

len = 200

ELSIF mincor = cor5 THEN

len = 250

ELSIF mincor = cor6 THEN

len = 300

ELSIF mincor = cor7 THEN

len = 350

ELSIF mincor = cor8 THEN

len = 400

ELSIF mincor = cor9 THEN

len = 450

ELSE

len = 500

ENDIF

ELSE

len = lengthinput

ENDIF

//-------------------------------------------------------------

// ===== Detrending opcional =====

//-------------------------------------------------------------

IF useDetrend = 1 THEN

trendline = LinearRegression[len](close)

src = close - trendline

ELSE

src = close

ENDIF

//-------------------------------------------------------------

// ===== Z-Score =====

//-------------------------------------------------------------

meanSrc = Average[len](src)

stdSrc = Std[len](src)

IF stdSrc > 0 THEN

z = (src - meanSrc) / stdSrc

ELSE

z = 0

ENDIF

//-------------------------------------------------------------

// ===== Filtro de regimen =====

//-------------------------------------------------------------

allowLong = 1

allowShort = 1

IF regimeFilter = 1 THEN

IF regimeMode = 1 THEN

ma = Average[malen](close)

IF ma > ma[slopeBars] THEN

allowLong = 1

allowShort = 0

ELSIF ma < ma[slopeBars] THEN

allowLong = 0

allowShort = 1

ELSE

allowLong = 1

allowShort = 1

ENDIF

ELSE

adxV = ADX[14]

IF adxV < adxLimit THEN

allowLong = 1

allowShort = 1

ELSE

allowLong = 0

allowShort = 0

ENDIF

ENDIF

ENDIF

//-------------------------------------------------------------

// ===== Niveles TP y SL =====

//-------------------------------------------------------------

atr = AverageTrueRange[14](close)

slLong = close - slMult * atr

slShort = close + slMult * atr

IF useDetrend = 1 THEN

tpRef = LinearRegression[len](close) + meanSrc

ELSE

tpRef = meanSrc

ENDIF

//-------------------------------------------------------------

// ===== Ratios RR =====

//-------------------------------------------------------------

riskLong = close - slLong

riskShort = slShort - close

IF riskLong > 0 THEN

rrLong = (tpRef - close) / riskLong

ELSE

rrLong = 0

ENDIF

IF riskShort > 0 THEN

rrShort = (close - tpRef) / riskShort

ELSE

rrShort = 0

ENDIF

//-------------------------------------------------------------

// ===== Cooldown =====

//-------------------------------------------------------------

ONCE barssincebuy = 1000

ONCE barssincesell = 1000

barssincebuy = barssincebuy + 1

barssincesell = barssincesell + 1

//-------------------------------------------------------------

// ===== Estado de tracking (persistente) =====

//-------------------------------------------------------------

ONCE inLong = 0

ONCE inShort = 0

ONCE entryLong = 0

ONCE entryShort = 0

ONCE tpLevelLong = 0

ONCE tpLevelShort = 0

ONCE slLevelLong = 0

ONCE slLevelShort = 0

ONCE longsCount = 0

ONCE longsWins = 0

ONCE shortsCount = 0

ONCE shortsWins = 0

ONCE rSum = 0

//-------------------------------------------------------------

// ===== Gestion de LONG abierto: detectar TP o SL =====

//-------------------------------------------------------------

IF inLong = 1 THEN

// Convencion conservadora: si la vela toca SL y TP, gana el SL

IF low <= slLevelLong THEN

longsCount = longsCount + 1

rSum = rSum - 1

IF showTradeClose = 1 THEN

DRAWPOINT(barindex, slLevelLong, 2) COLOURED(200,0,0)

ENDIF

inLong = 0

ELSIF high >= tpLevelLong THEN

longsCount = longsCount + 1

longsWins = longsWins + 1

rWin = (tpLevelLong - entryLong) / (entryLong - slLevelLong)

rSum = rSum + rWin

IF showTradeClose = 1 THEN

DRAWPOINT(barindex, tpLevelLong, 2) COLOURED(0,200,0)

ENDIF

inLong = 0

ENDIF

ENDIF

//-------------------------------------------------------------

// ===== Gestion de SHORT abierto: detectar TP o SL =====

//-------------------------------------------------------------

IF inShort = 1 THEN

IF high >= slLevelShort THEN

shortsCount = shortsCount + 1

rSum = rSum - 1

IF showTradeClose = 1 THEN

DRAWPOINT(barindex, slLevelShort, 2) COLOURED(200,0,0)

ENDIF

inShort = 0

ELSIF low <= tpLevelShort THEN

shortsCount = shortsCount + 1

shortsWins = shortsWins + 1

rWin = (entryShort - tpLevelShort) / (slLevelShort - entryShort)

rSum = rSum + rWin

IF showTradeClose = 1 THEN

DRAWPOINT(barindex, tpLevelShort, 2) COLOURED(0,200,0)

ENDIF

inShort = 0

ENDIF

ENDIF

//-------------------------------------------------------------

// ===== Senales y apertura de trades =====

//-------------------------------------------------------------

buyCross = (z[1] <= -zthreshold) AND (z > -zthreshold)

sellCross = (z[1] >= zthreshold) AND (z < zthreshold)

// LONG nueva

IF inLong = 0 AND buyCross AND allowLong = 1 AND z < 0 AND rrLong >= minRR AND barssincebuy >= cooldownBars THEN

inLong = 1

entryLong = close

tpLevelLong = tpRef

slLevelLong = slLong

barssincebuy = 0

DRAWARROWUP(barindex, low - 0.35*atr) COLOURED(0,200,0)

DRAWTEXT("Z=#z#", barindex, slLong - 1.5*atr) COLOURED("darkgreen")

DRAWTEXT("Len=#len#", barindex, slLong - 0.7*atr) COLOURED("darkgreen")

DRAWTEXT("RR=#rrLong#", barindex, tpRef + 0.5*atr) COLOURED("darkgreen")

IF plottgt = 1 THEN

DRAWSEGMENT(barindex, tpRef, barindex+50, tpRef) COLOURED(0,200,0)

DRAWSEGMENT(barindex, slLong, barindex+50, slLong) COLOURED(200,0,0)

ENDIF

ENDIF

// SHORT nueva

IF inShort = 0 AND sellCross AND allowShort = 1 AND z > 0 AND rrShort >= minRR AND barssincesell >= cooldownBars THEN

inShort = 1

entryShort = close

tpLevelShort = tpRef

slLevelShort = slShort

barssincesell = 0

DRAWARROWDOWN(barindex, high + 0.35*atr) COLOURED(200,0,0)

DRAWTEXT("Z=#z#", barindex, slShort + 1.5*atr) COLOURED("darkred")

DRAWTEXT("Len=#len#", barindex, slShort + 0.7*atr) COLOURED("darkred")

DRAWTEXT("RR=#rrShort#", barindex, tpRef - 0.5*atr) COLOURED("darkred")

IF plottgt = 1 THEN

DRAWSEGMENT(barindex, tpRef, barindex+50, tpRef) COLOURED(0,200,0)

DRAWSEGMENT(barindex, slShort, barindex+50, slShort) COLOURED(200,0,0)

ENDIF

ENDIF

//-------------------------------------------------------------

// ===== Coloreado de velas en extremos =====

//-------------------------------------------------------------

IF barcolor = 1 THEN

IF z >= zthreshold THEN

DRAWCANDLE(open, high, low, close) COLOURED("fuchsia")

ELSIF z <= -zthreshold THEN

DRAWCANDLE(open, high, low, close) COLOURED("black")

ENDIF

ENDIF

//-------------------------------------------------------------

// ===== Cuadro de stats en la ultima barra =====

//-------------------------------------------------------------

IF showStats = 1 AND IsLastBarUpdate THEN

totalTrades = longsCount + shortsCount

totalWins = longsWins + shortsWins

totalLosses = totalTrades - totalWins

IF totalTrades > 0 THEN

winrate = ROUND(1000 * totalWins / totalTrades) / 10

avgR = ROUND(100 * rSum / totalTrades) / 100

ELSE

winrate = 0

avgR = 0

ENDIF

IF longsCount > 0 THEN

wrLong = ROUND(1000 * longsWins / longsCount) / 10

ELSE

wrLong = 0

ENDIF

IF shortsCount > 0 THEN

wrShort = ROUND(1000 * shortsWins / shortsCount) / 10

ELSE

wrShort = 0

ENDIF

// Panel anclado a la esquina superior derecha (no se mueve con scroll/zoom)

panelX = -200 // 200 px a la izquierda del borde derecho

topY = -100 // 100 px hacia abajo del borde superior

DRAWTEXT("== STATS ==", panelX, topY) COLOURED(0,80,200) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("Trades: #totalTrades#", panelX, topY - 25) COLOURED(0,80,200) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("W/L: #totalWins# / #totalLosses#", panelX, topY - 50) COLOURED(0,80,200) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("Winrate: #winrate# %", panelX, topY - 75) COLOURED(0,80,200) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("Avg R: #avgR#", panelX, topY - 100) COLOURED(0,80,200) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("Long #longsCount# (WR #wrLong# %)", panelX, topY - 125) COLOURED(0,150,0) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

DRAWTEXT("Short #shortsCount# (WR #wrShort# %)", panelX, topY - 150) COLOURED(200,0,0) ANCHOR(TOPRIGHT, XSHIFT, YSHIFT)

ENDIF

//-------------------------------------------------------------

RETURN

Honest Results

The corrected v2 was tested on a few instruments and timeframes.

The expectancy is mildly positive on some markets, but the indicator is not robust across instruments and timeframes. It is more useful as a study tool than as a stand-alone signal generator. Adding extra filters (volatility regimes, time-of-day, support/resistance proximity, etc.) would likely push results into overfit territory without a real out-of-sample validation. We deliberately stop here.

The Real Lesson

When an indicator’s title contains “Machine Learning”, “AI”, “Neural Network” or similar buzzwords, read the source carefully. In the case of this Z-Score:

- The “Machine Learning” step turned out to be a fixed table of ten candidate lookbacks and an argmax. There is no learning, no optimization loop, no out-of-sample evaluation. The label is marketing.

- Even if we accept the framing as auto-selection, the criterion (maximum R²) is the opposite of what mean-reversion needs. The two halves of the indicator work against each other.

- The signal logic has a self-fulfilling condition (c <= Lowest[len](c)) and a counter bug (buywait is never reset on the failing branch). Either of these would have been caught by anyone tracing the indicator with print statements.

The mistake is not Steversteves’s alone. Indicator marketplaces reward complex-looking ideas, not validated ones. The defense is always the same: understand every line of code in any indicator you intend to use, demand a proper backtest with realistic costs, and treat brand-name labels (“AI”, “ML”, “smart”) as a marketing input, not a quality signal. This article is a small contribution to that habit.