Laguerre Filter on price

March 24, 2016, 3:47 PM

Indicators

3 Comments

{kind=link}

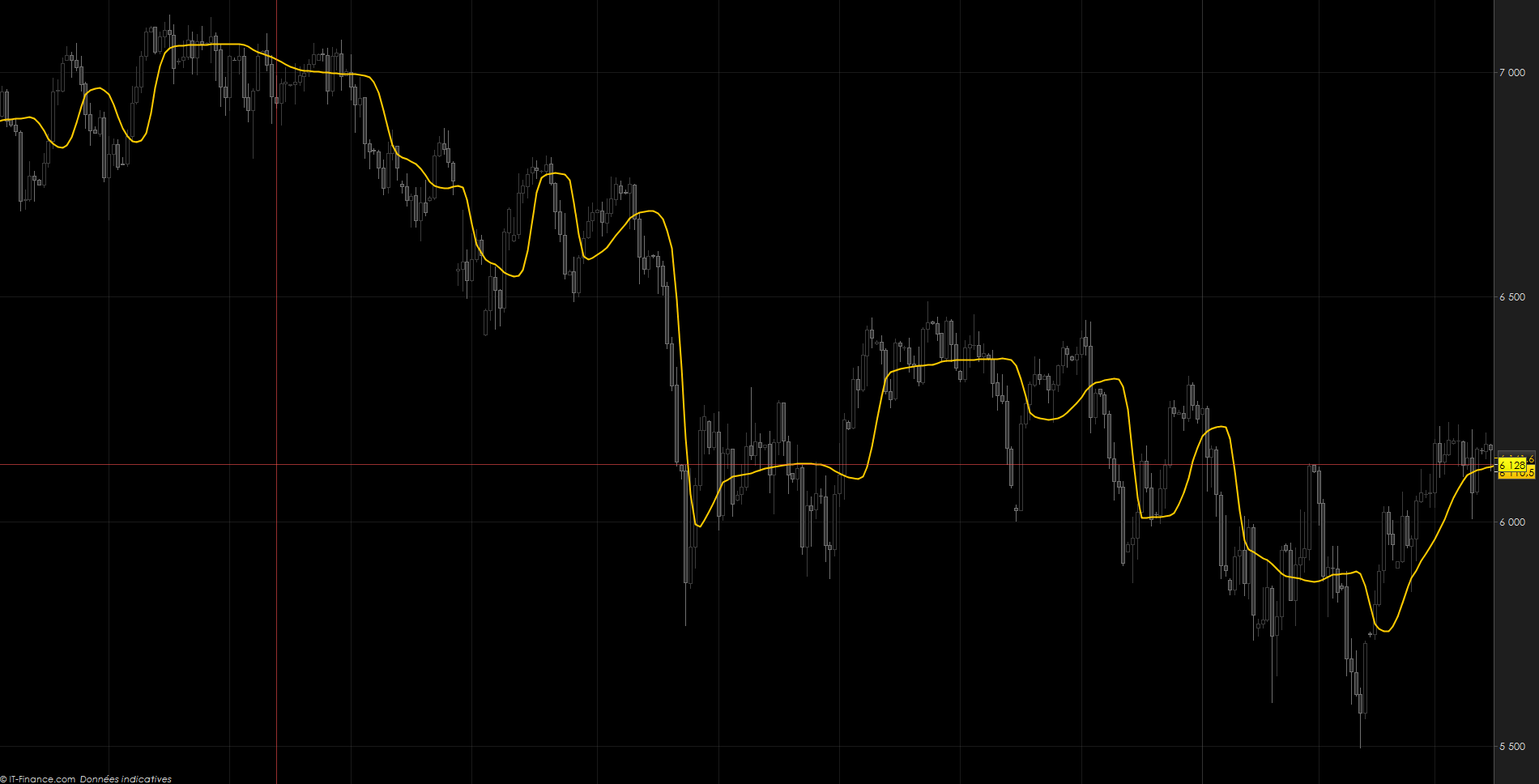

The Laguerre filter is a mathematical filter used to have a better idea of price direction while denoising it. It were made by John Ehlers. Everything can be denoised by applying this filter, from oscillator like RSI to any others trend indicators. This one is only for price purpose, so I think that someone can adapt it for other things of interest of the community.

//parameters :

//length = 20

//Elements = 5

Price = (High+Low+Open+Close)/4

Diff = ABS(Price - Filt[1])

HH = Diff

LL = Diff

FOR count = 0 TO Length - 1

IF Diff[count] > HH THEN

HH = Diff[count]

ENDIF

IF Diff[count] < LL THEN

LL = Diff[count]

ENDIF

NEXT

If Barindex > Length AND HH - LL <> 0 THEN

Calcul = (Diff - LL) / (HH - LL)

// Calculate MEDIAN with 5 Elements. Vary at will

Data = Calcul

NrElements = Elements

FOR X = 0 TO NrElements-1

M = Data[X]

SmallPart = 0

LargePart = 0

FOR Y = 0 TO NrElements-1

IF Data[Y] < M THEN

SmallPart = SmallPart + 1

ELSIF Data[Y] > M THEN

LargePart = LargePart + 1

ENDIF

IF LargePart = SmallPart AND Y = NrElements-1 THEN

Median = M

BREAK

ENDIF

NEXT

NEXT

alpha = Median

L0 = alpha*Price + (1 - alpha)*L0[1]

L1 = -(1 - alpha)*L0 + L0[1] + (1 - alpha)*L1[1]

L2 = -(1 - alpha)*L1 + L1[1] + (1 - alpha)*L2[1]

L3 = -(1 - alpha)*L2 + L2[1] + (1 - alpha)*L3[1]

FILT = (L0 + 2*L1 + 2*L2 + L3) / 6

ENDIF

IF Barindex < 1 THEN

FILT = Price

ENDIF

RETURN Filt AS "Laguerre1"

Download

Filename:

Laguerre-Filter.itf

Downloads:

372

Junior

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...