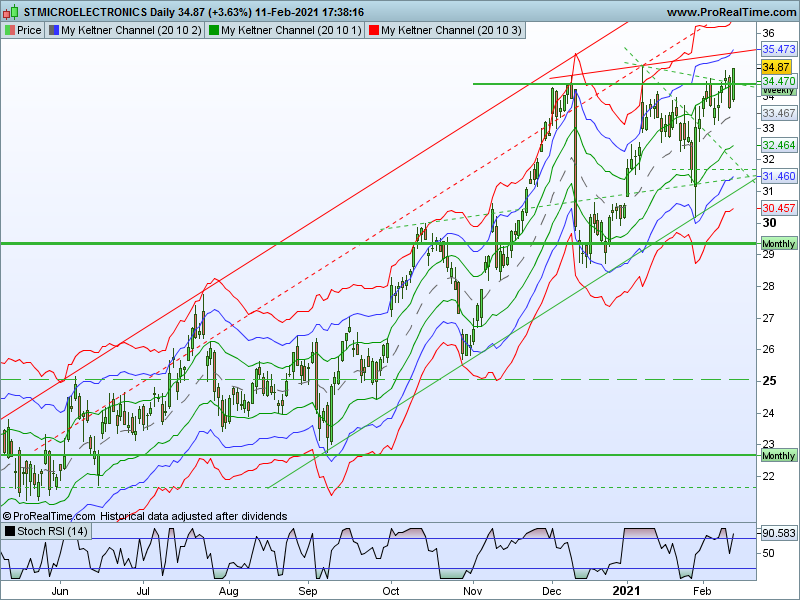

Keltner Channel (EMA, ATR)

February 16, 2021, 10:23 AM

Indicators

0 Comments

{kind=link}

In his 1960 book, How to Make Money in Commodities, Chester Keltner introduced the “Ten-Day Moving Average Trading Rule,” which is credited as the original version of Keltner Channels.

This original version started with a 10-day SMA of the typical price {(H+L+C)/3)} as the centerline. The 10-day SMA of the High-Low range was added and subtracted to set the upper and lower channel lines. Linda Bradford Raschke introduced the newer version of Keltner Channels in the 1980s. Like Bollinger Bands, this new version used a volatility based indicator, Average True Range (ATR), to set channel width.

// Keltner Channel

//periodMA=20

//periodATR=10

//k=2

MA = ExponentialAverage[periodMA](close)

// Upper Keltner Band

UpperBand = MA + k*AverageTrueRange[periodATR](close)

// Lower Keltner Band

LowerBand = MA - k*AverageTrueRange[periodATR](close)

RETURN MA AS "Keltner MA" , UpperBand AS "Keltner Upper Band" , LowerBand as "Keltner Lower Band"

Download

Filename:

KeltnerChannel-EMA-ATR.itf

Downloads:

278

Master

Operating in the shadows, I hack problems one by one. My bio is currently encrypted by a complex algorithm. Decryption underway...

Author’s Profile

Loading...