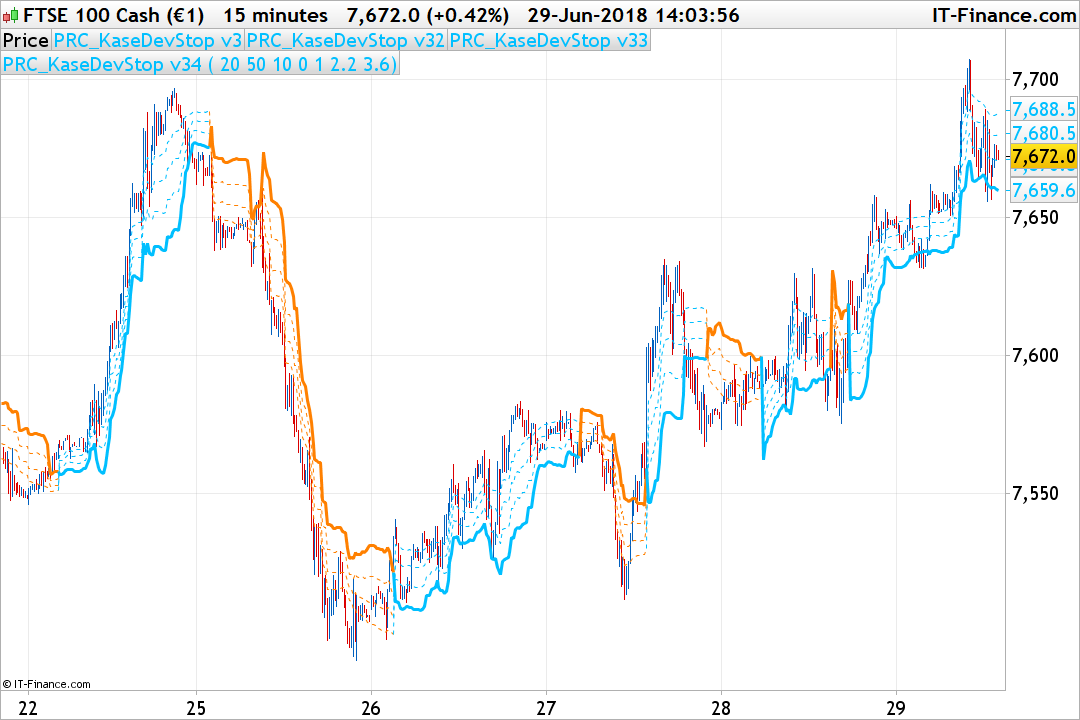

Kase Dev Stop v3

June 29, 2018, 1:07 PM

Indicators

8 Comments

{kind=link}

As requested in the forum, here is a new version of the Cynthia Kase Dev Stop indicator.

Originally developed bu Cynthia Kase (in her book “Trading With the Odds”). This version is calculating the DevStops exactly as described in the book.

Engineering a Better Stop: The Kase DevStops

What all of this boils down to is that we need to take variance and skew into consideration when we are establishing a system for setting stops. Three steps that we can take in order to both better define and to minimize the threshold of uncertainty in setting stops are:

- Consideration of the variance or the standard deviation of range.

- Consideration of the skew, or more simply, the amount at which range can spike in the opposite direction of the trend.

- Reformation of our data to be more consistent (this step is examined in detail in Chapter 81, while minimizing the degree of uncertainty as much as possible).

//PRC_KaseDevStop v3 | indicator

//29.06.2018

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

//translated from MT5 code version

//--- settings

inpDesPeriod = 20 // Dev-stop period

inpSlowPeriod = 21 // Dev-stop slow period

inpFastPeriod = 10 // Dev-stop fast period

inpStdDev1 = 0.0 // Deviation 1

inpStdDev2 = 1.0 // Deviation 2

inpStdDev3 = 2.2 // Deviation 3

inpStdDev4 = 3.6 // Deviation 4

//--- end of settings

pricc=customclose

once price=close*100

average1 = average[inpFastPeriod](pricc)

average2 = average[inpSlowPeriod](pricc)

if average1>average2 then

trend=1

r=0

g=191

b=255

else

trend=-1

r=255

g=128

b=0

endif

if trend<>trend[1] then

if trend=1 then

price=high

else

price=low

endif

endif

if trend>0 then

price=max(price,high)

endif

if trend<0 then

price=min(price,low)

endif

mmax=max(max(high,high[1]),pricc[2])

mmin=min(min(low,low[1]),pricc[2])

rrange=mmax-mmin

avg=rrange

for n=1 to inpDesPeriod-1 do

avg=(avg+rrange[n])

next

avg=avg/n

dev = square(rrange-avg)

for n=1 to inpDesPeriod-1 do

dev=dev+(rrange[n]-avg)*(rrange[n]-avg)

next

dev=sqrt(dev/n)

val = price+(-1)*trend*(avg+(inpStdDev1*dev))

val1 = price+(-1)*trend*(avg+(inpStdDev2*dev))

val2 = price+(-1)*trend*(avg+(inpStdDev3*dev))

val3 = price+(-1)*trend*(avg+(inpStdDev4*dev))

return val coloured(r,g,b) style(dottedline,1) ,val1 coloured(r,g,b) style(dottedline,1) ,val2 coloured(r,g,b) style(dottedline,1),val3 coloured(r,g,b) style(line,3)

Download

Filename:

PRC_KaseDevStop-v3.itf

Downloads:

279

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...