Intraday flexible camarilla pivot points

October 12, 2020, 3:15 PM

Indicators

4 Comments

{kind=link}

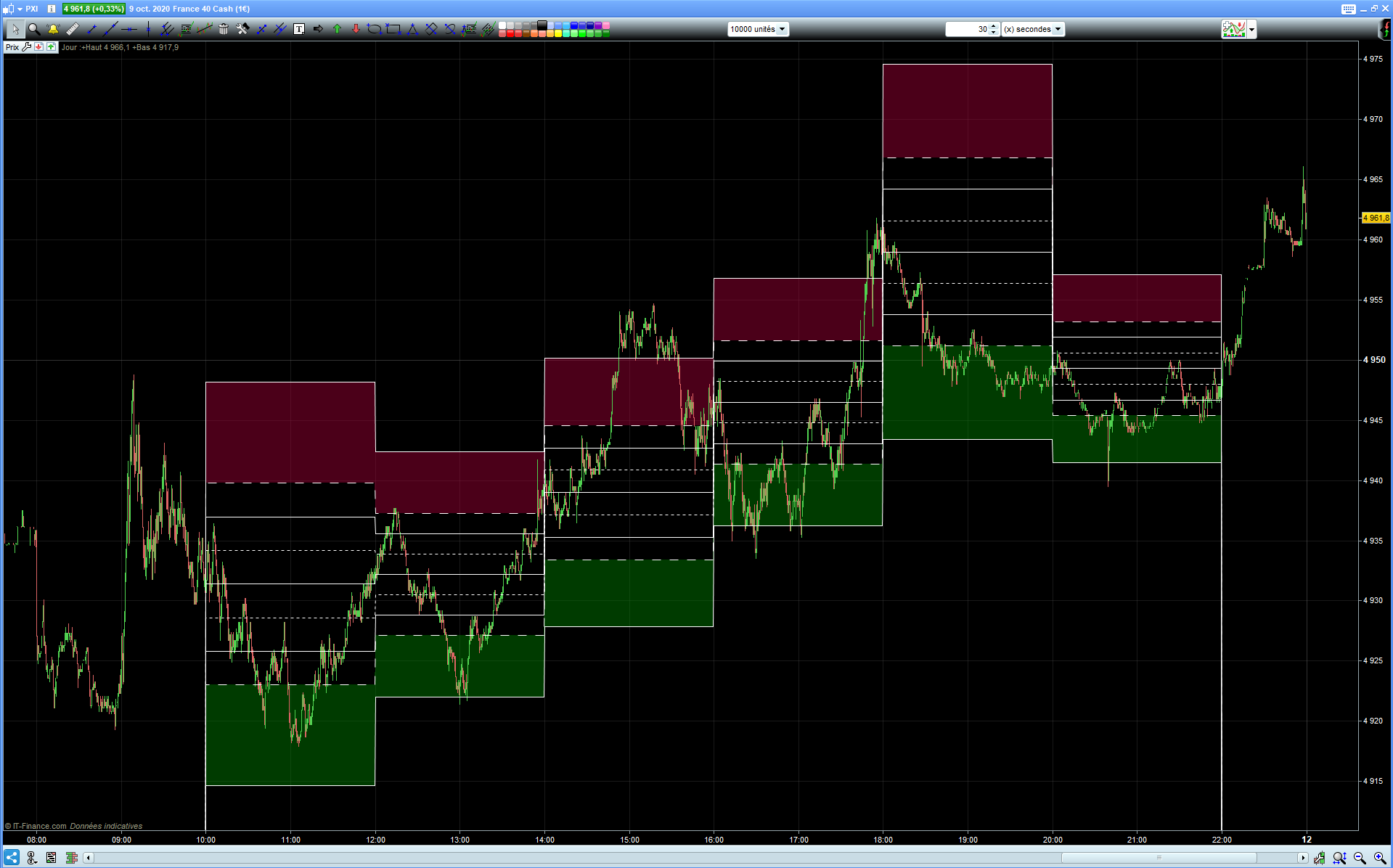

A flexible intraday camarilla pivot points indicator was requested on the probuilder french forum, working for no matter how small the timeframe, robust enough to function in case of empty bars :

http://www.prorealcode.com/topic/point-pivot-camarilla-hourly/

Change integer n among values 15, 30, 60, 120, 180, 240 in minutes as the period for calculation of the camarilla pivot points.

Use start and finish variables in HHMMSS format for intraday start and finish times. First calculation is made one « n » period after the start.

// PRC Camarilla Pivot Points intra day

// 04.10.2020 mod 09.10.2020

// Noobywan @ www.prorealcode.com

// Sharing ProRealTime Knowledge

// Forum ProBuilder user Choliver request

// --- Settings

n=120 // time span in minutes, choose parameter n equal to 15, 30, 60, 120, 180 or 240

start=080000 // time start in HHMMSS format

finish=220000 // time end in HHMMSS format

// --- End of settings

//

if n=15 then

changebarre= openminute[1]>openminute or (openminute[1]<15 and openminute>=15) or (openminute[1]<30 and openminute>=30) or (openminute[1]<45 and openminute>=45)

deltamin=1500

elsif n=30 then

changebarre= openminute[1]>openminute or (openminute[1]<30 and openminute>=30)

deltamin=3000

elsif n=60 then

changebarre= openminute[1]>openminute

deltamin=10000

elsif n=120 then

deltamin=20000

hrs=(opentime-start)/deltamin

changebarre= (hrs[1]<1 and hrs>=1) or (hrs[1]<2 and hrs>=2) or (hrs[1]<3 and hrs>=3) or (hrs[1]<4 and hrs>=4) or (hrs[1]<5 and hrs>=5) or (hrs[1]<6 and hrs>=6) or (hrs[1]<7 and hrs>=7) or (hrs[1]<8 and hrs>=8) or (hrs[1]<9 and hrs>=9) or (hrs[1]<10 and hrs>=10) or (hrs[1]<11 and hrs>=11)

elsif n=180 then

deltamin=30000

hrs=(opentime-start)/deltamin

changebarre= (hrs[1]<1 and hrs>=1) or (hrs[1]<2 and hrs>=2) or (hrs[1]<3 and hrs>=3) or (hrs[1]<4 and hrs>=4) or (hrs[1]<5 and hrs>=5) or (hrs[1]<6 and hrs>=6) or (hrs[1]<7 and hrs>=7)

elsif n=240 then

deltamin=40000

hrs=(opentime-start)/deltamin

changebarre= (hrs[1]<1 and hrs>=1) or (hrs[1]<2 and hrs>=2) or (hrs[1]<3 and hrs>=3) or (hrs[1]<4 and hrs>=4) or (hrs[1]<5 and hrs>=5)

else

DRAWTEXT("n must be 15, 30, 60, 120, 180 or 240", barindex, close)

endif

//

if changebarre then

stoque=barchange

barchange=barindex

myhigh=highest[barchange-stoque](high)[1]

mylow=lowest[barchange-stoque](low)[1]

myclose=close[1]

endif

//

if opentime>=start+deltamin and opentime<finish then

PPcama=myclose

R1cama=myclose+(myhigh-mylow)*1.1/12

R2cama=myclose+(myhigh-mylow)*1.1/6

R3cama=myclose+(myhigh-mylow)*1.1/4

R4cama=myclose+(myhigh-mylow)*1.1/2

S1cama=myclose-(myhigh-mylow)*1.1/12

S2cama=myclose-(myhigh-mylow)*1.1/6

S3cama=myclose-(myhigh-mylow)*1.1/4

S4cama=myclose-(myhigh-mylow)*1.1/2

else

PPcama=0

R1cama=0

R2cama=0

R3cama=0

R4cama=0

S1cama=0

S2cama=0

S3cama=0

S4cama=0

endif

RETURN PPcama AS "PP Camarilla", R1cama AS "R1 Camarilla", R2cama AS "R2 Camarilla", R3cama AS "R3 Camarilla", R4cama AS "R4 Camarilla", S1cama AS "S1 Camarilla", S2cama AS "S2 Camarilla", S3cama AS "S3 Camarilla", S4cama AS "S4 Camarilla"

Download

Filename:

PRC_export_camarilla_intraday.itf

Downloads:

380

Master

https://market.prorealcode.com/store/volume-profile-solutions/ - Trading since 2008, using PRT since 2009, PRC forums moderator since 2016, helping out when I can. Using personal algorithmic universal market model (any market, any timeframe, self-adaptating no optimisation required), and volume profile and tape personal tools. Scientific coding skills from past life in aerospace sector, in Computational Fluid Dynamics.

Author’s Profile

Loading...