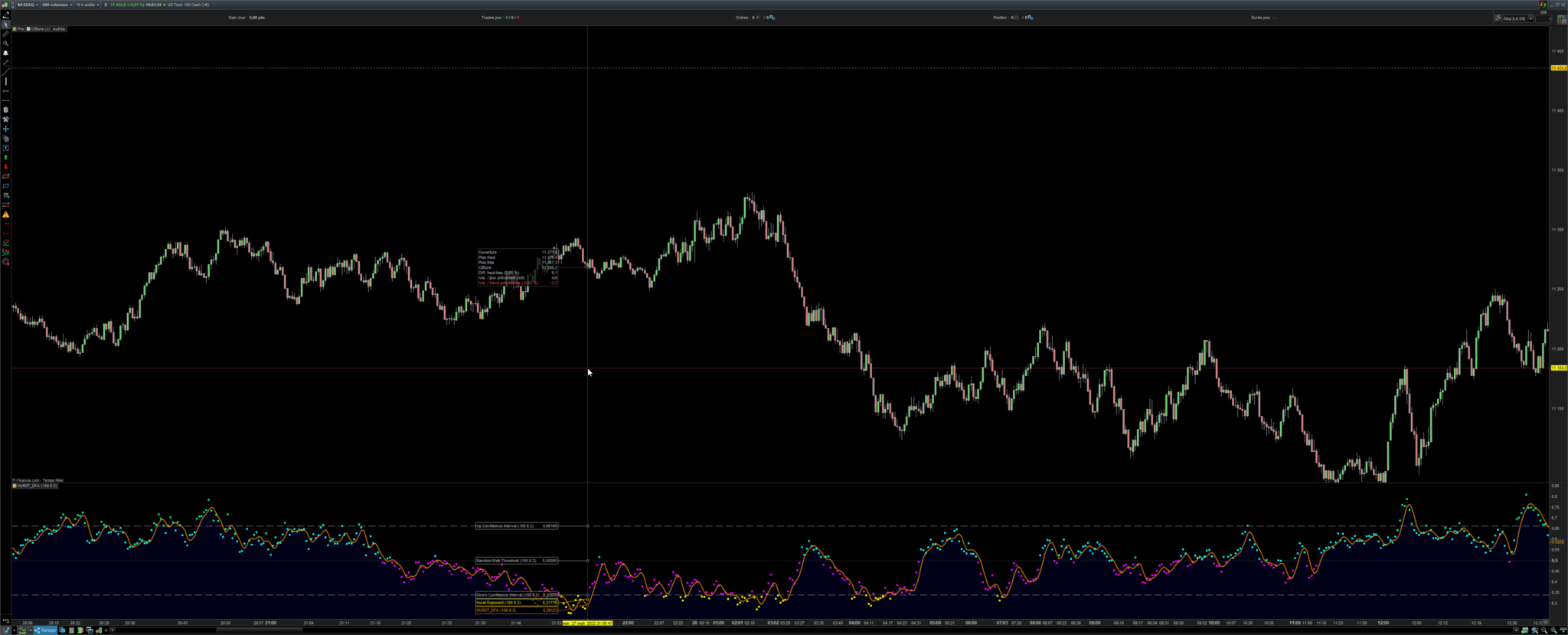

Hurst Exponent - Detrended Fluctuation Analysis

October 13, 2022, 1:17 PM

Indicators

2 Comments

{kind=link}

This is the port to PRT of the nice balipour indicator from tradingview.

In stochastic processes, chaos theory and time series analysis, detrended fluctuation analysis (DFA) is a method for determining the statistical self-affinity of a signal. It is useful for analyzing time series that appear to be long-memory processes and noise.

WARNING : this indicator will hit your CPU very hard. It was a test drive for me to test the limit of ProBuilder. I don’t recommend using it in real time.

For practical and intuitive indicators, you can have a look at my ProRealCode Market store.

//defparam calculateonlastbars = 2000

// Params

len: 100

bsc: 8

msc: 2

//Log Return

r = log(close / close[1])

//Mean of Log Return

mean = average[len](r)

//Cumulative Sum

sum = 0

for i = 0 to len - 1 do

sum = (r[i] - mean) + sum

$csum[i] = sum

next

// Approximating log scale function (save sample size)

for i = 0 to 9 do

$fs[i] = round(bsc*pow(pow(len/(msc*bsc),0.1111111111),i))

next

for i = 0 to 9 do

//Average of Root Mean Sum Measured each block (Log Scale) ARMS

bar = $fs[i]

num = floor(len / bar)

sumr = 0

for j = 0 to num - 1 do

//Root Mean Sum (FLuctuation) function linear trend to calculate error between linear trend and cumulative sum

rms = 0

count = 0

N1 = j * bar

N = bar

//Slicing the array into different segments

for k = 0 to N - 1 do

count = count + 1

$seq[k] = count

next

for k = N1 to N1 + N - 1 do

$y[k - N1] = $csum[k]

next

//Linear regression measuing trend (N/(N-1) for sample unbiased adjustedment)

ec = 0

for k = 0 to N - 1 do

ec = ec + $seq[k]

next

mc = ec / N

varx = 0

for k = 0 to N - 1 do

varx = varx + square($seq[k] - mc)

next

sdx = sqrt(varx/N) * sqrt(N/(N-1))

ey = 0

for k = 0 to N - 1 do

ey = ey + $y[k]

next

my = ey / N

vary = 0

for k = 0 to N - 1 do

vary = vary + square($y[k] - my)

next

sdy = sqrt(vary/N) * sqrt(N/(N-1))

esy = 0

for k = 0 to N - 1 do

esy = esy + $seq[k] * $y[k]

next

msy = esy / N

cov = (msy - mc * my) * (N/(N-1))

rr2 = pow(cov/(sdx*sdy), 2)

rms = sqrt(1 - rr2) * sdy

sumr = sumr + rms

next

$fluc[i] = log(sumr / num) / log(10)

next

//Set Ten Points of data scale along the X log axis

for i = 0 to 9 do

$scl[i] = log($fs[i]) / log(10)

next

// Slope Measured from RMS and scale on log log plot using linear regression

ssc = 0

for i = 0 to 9 do

ssc = ssc + $scl[i]

next

esc = ssc / 10

sfl = 0

for i = 0 to 9 do

sfl = sfl + $fluc[i]

next

efl = sfl / 10

sf = 0

for i = 0 to 9 do

sf = sf + ($scl[i] - esc) * ($fluc[i] - efl)

next

cov = sf / 10

ssq = 0

for i = 0 to 9 do

ssq = ssq + square($scl[i] - esc)

next

var = ssq / 10

hurst = cov / var

//Critical Value based on Confidence Interval (95% Confidence)

ci = 1.645 * (0.3912 / pow(len,0.3))

//Expected Value plus Crtical Value

cu = 0.5 + ci

cd = 0.5 - ci

if hurst > cu then

hr = 0

hg = 255

hb = 128

elsif hurst >= 0.5 then

hr = 0

hg = 255

hb = 255

elsif hurst < cd then

hr = 255

hg = 255

hb = 0

elsif hurst < 0.5 then

hr = 255

hg = 0

hb = 255

endif

smooth = (hurst + 2 * hurst[1] + 2 * hurst[2] + hurst[3]) / 6

return hurst coloured(hr, hg, hb) style(point, 3) as "Hurst Exponent", cu as "Up Confidence Interval", cd as "Down Confidence Interval", 0.5 as "Random Walk Threshold", smooth

Download

Filename:

HurstExp–DetrendedFluctAnalys.itf

Downloads:

100

Senior

https://market.prorealcode.com/store/digital-filters-workshop/

Author’s Profile

Loading...