Ehlers Inverse Fisher Transform of RSI or RSX

August 20, 2018, 8:57 AM

Indicators

5 Comments

{kind=link}

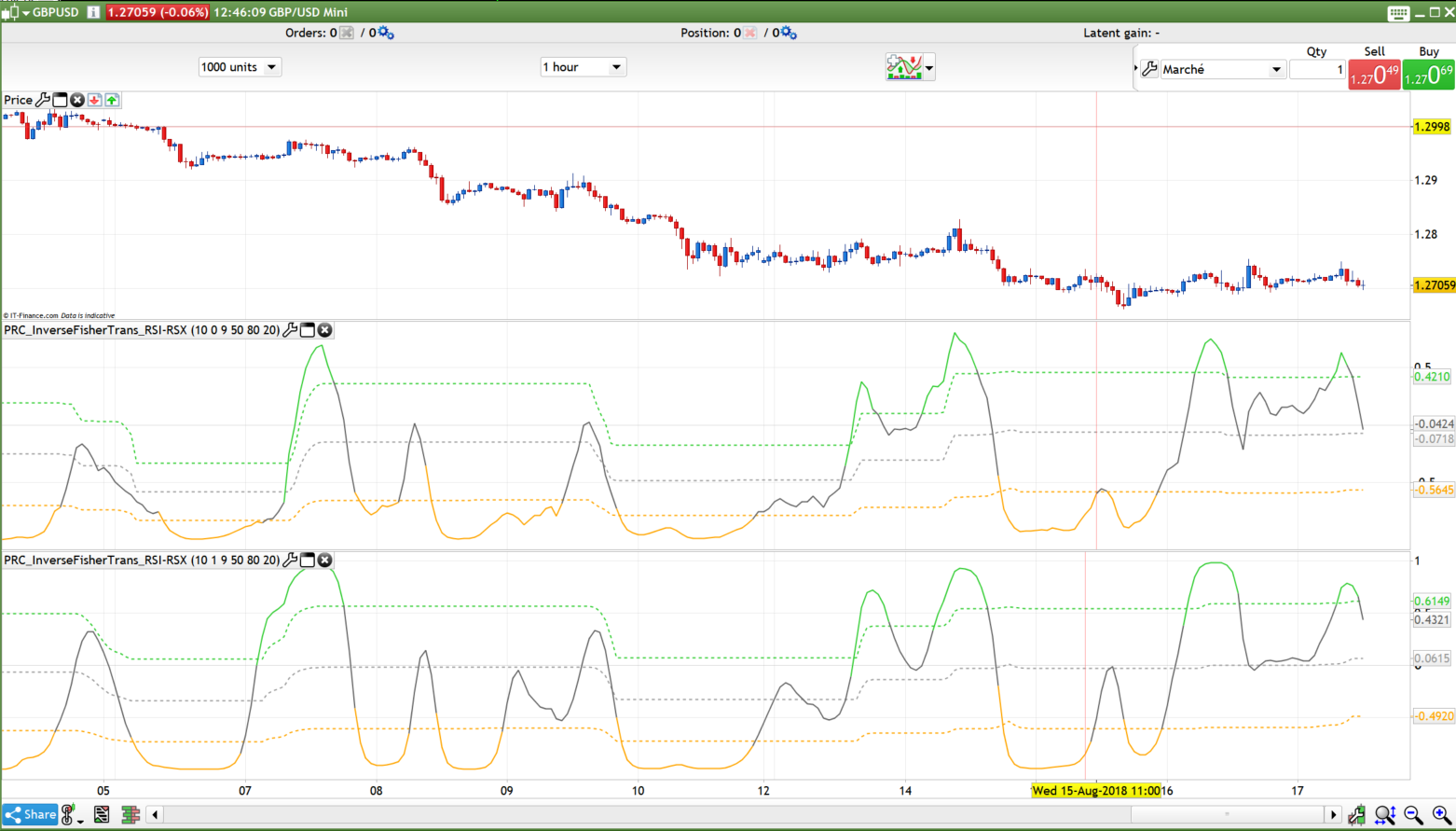

Published in the Technical Analysis of Stocks and Commodities magazine in the May 2004 issue, the inverse fisher transform is an indicator created by John Ehlers. The Inverse Fisher Transform was developed to help traders and investors with their timing decisions to buy and sell securities. It does this by altering the probability distribution function (PDF) of any indicator and makes it appear smoother.

This version include the inverse fisher transform calculation method applied on the RSI (upper oscillator in the screenshot) or the RSX (lower oscillator in the attached picture).

Settings explained:

- RsiPeriod: Period of RSI or RSX oscillator

- RsiMethod: 0=RSI 1=RSX

- SmoothPeriod: Smoothing period applied on the oscillator with a linear weighted average

- MinMaxPeriod: period of highest high / lowest low to calculate the dynamic overbough/oversold levels

- LevelUp: percentage of the overbought upper level

- LevelDown: percentage of the oversold lower level

//PRC_InverseFisherTrans_RSI-RSX | indicator

//17.08.2018

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

// --- settings

RsiPeriod = 10 // RSI period

RsiMethod = 1 // Rsi method (0=RSI, 1=RSX)

SmoothPeriod = 9 // Smoothing period

MinMaxPeriod = 50 // Floating levels period (<= 1 for fixed levels)

LevelUp = 80.0 // Up level %

LevelDown = 20.0 // Down level %

// --- end of settings

RsiPrice = customclose // Price

if barindex>RsiPeriod then

smallRsiValue = 0.0000000000000001

if RsiMethod=0 then

//RSI

alpha = 1.0/Max(RsiPeriod,1)

change = RsiPrice-RsiPrice[1]

workRsichange = workRsichange[1] + alpha*( change - workRsichange[1])

workRsichanga = workRsichanga[1] + alpha*(Abs(change) - workRsichanga[1])

iRsi = (50.0*(workRsichange/Max(workRsichanga,smallRsiValue)+1))

else

//RSX

Len=rsiperiod

if (f90 = 0.0) then

f90 = 1.0

f0 = 0.0

if (Len-1 >= 5) then

f88 = Len-1.0

else

f88 = 5.0

endif

f8 = 100.0*(rsiprice)

f18 = 3.0 / (Len + 2.0)

f20 = 1.0 - f18

else

if (f88 <= f90) then

f90 = f88 + 1

else

f90 = f90 + 1

endif

f10 = f8

f8 = 100*Close

v8 = f8 - f10

f28 = f20 * f28 + f18 * v8

f30 = f18 * f28 + f20 * f30

vC = f28 * 1.5 - f30 * 0.5

f38 = f20 * f38 + f18 * vC

f40 = f18 * f38 + f20 * f40

v10 = f38 * 1.5 - f40 * 0.5

f48 = f20 * f48 + f18 * v10

f50 = f18 * f48 + f20 * f50

v14 = f48 * 1.5 - f50 * 0.5

f58 = f20 * f58 + f18 * Abs(v8)

f60 = f18 * f58 + f20 * f60

v18 = f58 * 1.5 - f60 * 0.5

f68 = f20 * f68 + f18 * v18

f70 = f18 * f68 + f20 * f70

v1C = f68 * 1.5 - f70 * 0.5

f78 = f20 * f78 + f18 * v1C

f80 = f18 * f78 + f20 * f80

v20 = f78 * 1.5 - f80 * 0.5

if ((f88 >= f90) and (f8 <> f10)) then

f0 = 1.0

endif

if ((f88 = f90) and (f0 = 0.0)) then

f90 = 0.0

endif

endif

if ((f88 < f90) and (v20 > smallRsiValue)) then

v4 = (v14 / v20 + 1.0) * 50.0

if (v4 > 100.0) then

v4 = 100.0

endif

if (v4 < 0.0) then

v4 = 0.0

endif

else

v4 = 50.0

endif

irsi=v4

endif

//linear weighted moving average

sumw = smoothperiod

sum = smoothperiod*(0.1*(iRsi-50))

workLwma = (0.1*(iRsi-50))

for k=1 to smoothperiod-1 do

weight = smoothperiod-k

sumw = sumw + weight

sum = sum+(weight*workLwma[k])

next

trss = (sum/sumw)

//oscillator final cut

e = 2.7182818284590452353602874713527

y = exp((2.0*trss)*log(e))

rsii=(y-1.0)/(y+1.0)

//levels

mmin = rsii

mmax = rsii

for k=1 to MinMaxPeriod-1 do

mmin=min(rsii[k],mmin)

mmax=max(rsii[k],mmax)

next

rrange = mmax-mmin

levelupz = mmin+LevelUp * rrange/100

leveldnz = mmin+LevelDown * rrange/100

levelmi = mmin+0.5*rrange

//Color

r=100

g=100

b=100

if rsii>levelupz then

r=50

g=205

b=50

elsif rsii<leveldnz then

r=255

g=165

b=0

endif

endif

return levelupz coloured(50,205,50) style(dottedline,2) as "Level Up", leveldnz coloured(255,165,0) style(dottedline,2) as "Level Down", levelmi coloured(155,155,155) style(dottedline,2) as "mid level", rsii coloured(r,g,b) style(line,2) as "RSI"

Download

Filename:

PRC_InverseFisherTrans_RSI-RSX.itf

Downloads:

248

Legend

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...