Edge Index

May 9, 2017, 10:01 AM

Indicators

2 Comments

{kind=link}

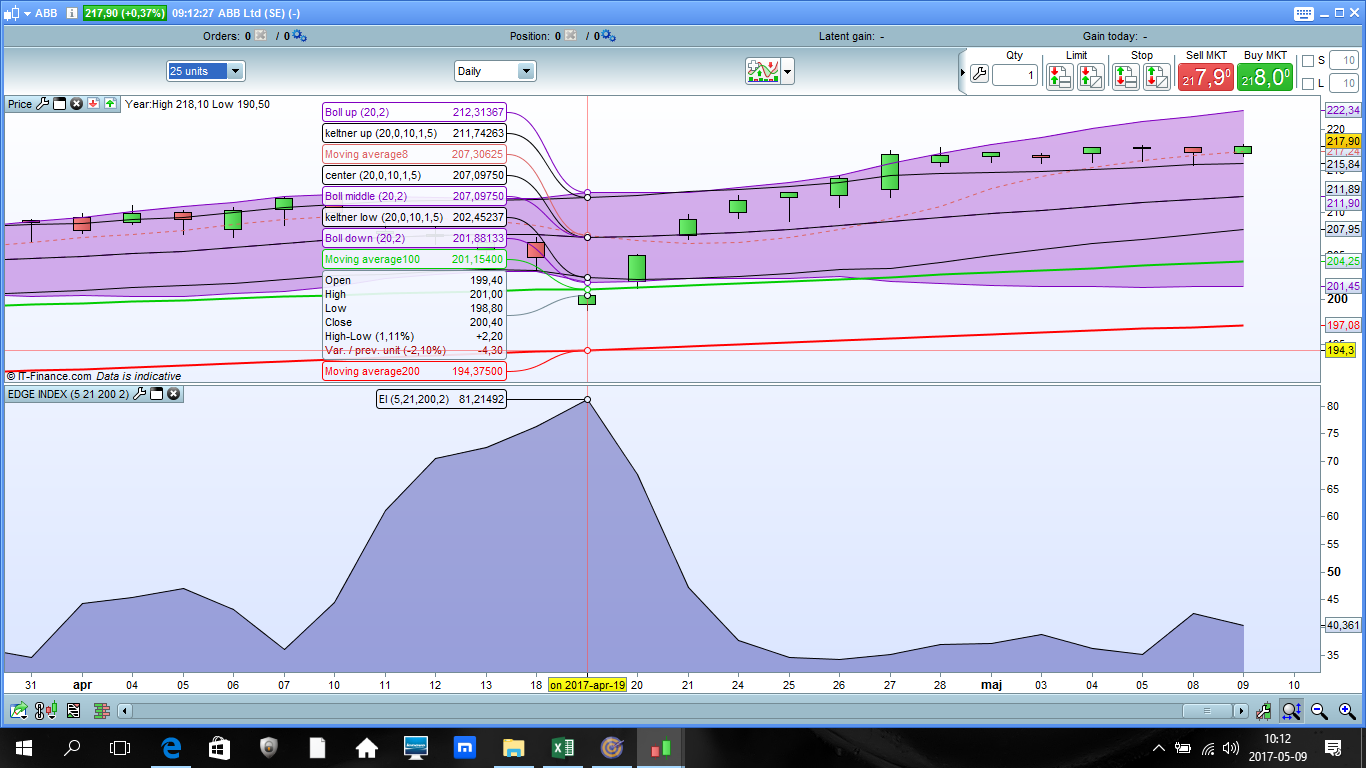

I find Edge Index to be useful in prioritizing mean reversion opportunities like for instance Rikoschett or Close below the lower Bollingerband.

Edge Index is intended for Daily time frames = does not work on intra day, not with the default parameter settings anyway.

My initial testing is showing that EDGE INDEX works better in a bull market.

REM Computes the highest and lowest prices

Shi = highest[S](high)

Slo = lowest[S](low)

Mhi = highest[M](high)

Mlo = lowest[M](low)

Lhi = highest[L](high)

Llo = lowest[L](low)

REM Building the oscillators

StochS = (close - Slo) / (Shi - Slo) * 100

StochM = (close - Mlo) / (Mhi - Mlo) * 100

StochL = (close - Llo) / (Lhi - Llo) * 100

REM We can now compute the EdgeIndex

EDGEINDEXRAW = (100 - StochS)/3 + (100-StochM)/3 + StochL/3

EDGEINDEX = EDGEINDEXRAW[0]*0.6 + EDGEINDEXRAW[1]*0.4

RETURN EDGEINDEX as "EI"

Download

Filename:

EDGE-INDEX.itf

Downloads:

101

New

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...