Deviation-Scaled Moving Average - DSMA

June 15, 2018, 1:03 PM

Indicators

9 Comments

{kind=link}

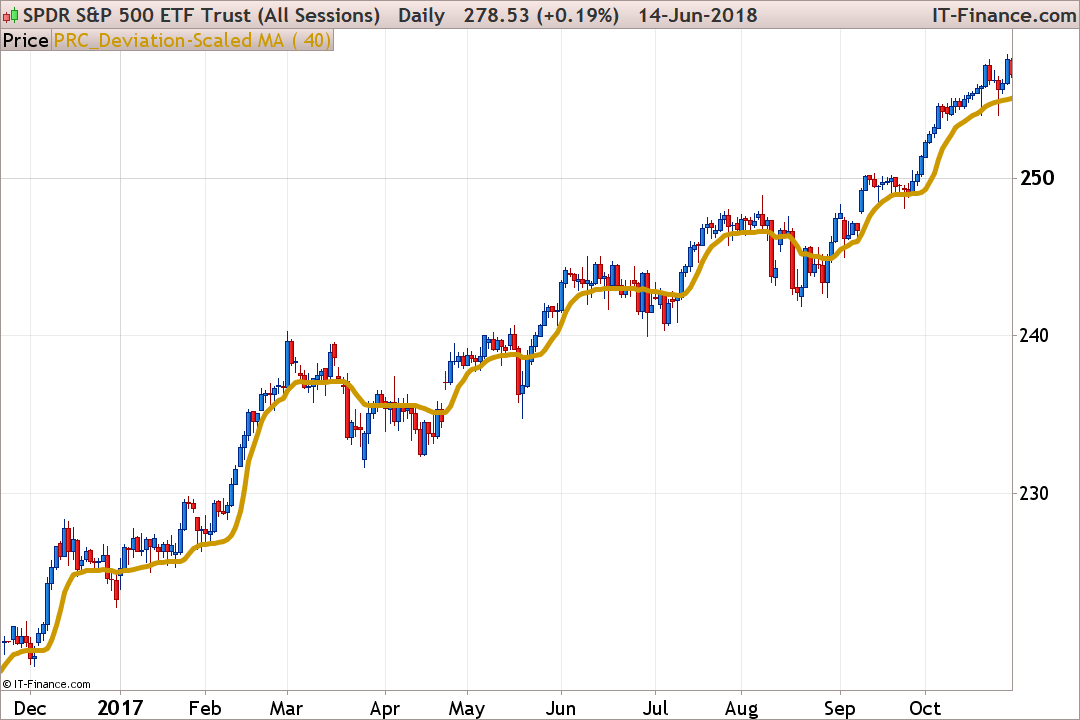

Here is the new DSMA moving average made my John Ehlers and featured in the July 2018 issue of TASC magazine.

The DSMA is an adaptive moving average that features rapid adaptation to volatility in price movement.

It accomplishes this adaptation by modifying the alpha term of an EMA byt he amplitude of an oscillator scaled in standard deviations from the mean. The DSMA’s responsiveness can be changed by using different values for the input parameter period.

John Ehlers

//PRC_Deviation Scaled Moving Average | indicator

//15.06.2018

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

// --- settings

Period = 40

// --- end of settings

If barindex>Period Then

//Smooth with a Super Smoother

a1 = exp(-1.414*3.14159 / (.5*Period))

b1 = 2*a1*Cos(1.414*180 / (.5*Period))

c2 = b1

c3 = -a1*a1

c1 = 1 - c2 - c3

//Produce Nominal zero mean with zeros in the transfer response

//at DC and Nyquist with no spectral distortion

//Nominally whitens the spectrum because of 6 dB per octave

//rolloff

Zeros = Close - Close[2]

//SuperSmoother Filter

Filt = c1*(Zeros + Zeros[1]) / 2 + c2*Filt[1] + c3*Filt[2]

//Compute Standard Deviation

RMS = 0

For count = 0 to Period - 1 do

RMS = RMS + Filt[count]*Filt[count]

next

RMS = SqRt(RMS / Period)

//Rescale Filt in terms of Standard Deviations

ScaledFilt = Filt / RMS

alpha1 = Abs(ScaledFilt)*5 / Period

DSMA = alpha1*Close + (1 - alpha1)*DSMA[1]

endif

return DSMA

Download

Filename:

PRC_Deviation-Scaled-MA.itf

Downloads:

295

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...